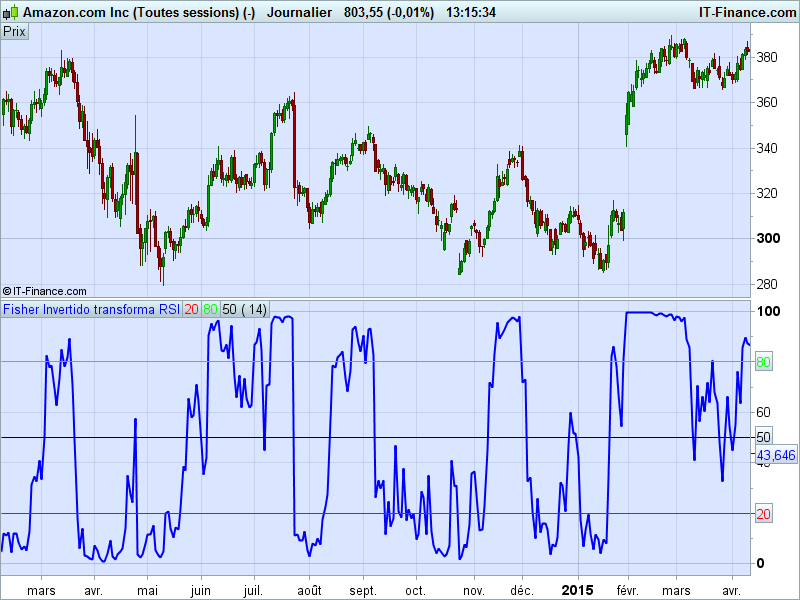

Inverse Fisher transform on RSI

February 3, 2017, 2:21 PM

Indicators

0 Comments

{kind=link}

Developed by John Ehlers, the RSI-based inverse Fisher Transform is used to help clearly define trigger points.

The normal RSI indicator is calculated and adjusted so that the values are centered around zero. The inverse transform is then applied to these values.

John Ehlers recommend to smooth the result of the calculation with a weighted average, but that’s not the case into this one.

The default RSI period is set to 14.

/// Variable N = Núm. de velas para calcular el RSI = 14

/// Fisher invertido en histograma

/// variable N puede modificarse a gusto de cada uno.

ind=RSI[N](close)

x=0.1*(ind-50)

y=(EXP(2*x)-1)/(EXP(2*x)+1)

ynorma=50*(y+1)

RETURN ynorma COLOURED (0, 0, 255) AS"Fisher Invertido transforma RSI", 20 COLOURED (255, 0, 0) AS"20", 80 COLOURED (0, 255, 0) AS"80", 50 COLOURED (0,0,0)AS"50"

Download

Filename:

Inverse-Fisher-transform-RSI.itf

Downloads:

179

Download

{kind=link}

Filename:

fisher-1486057680lc48p.jpg

Downloads:

50

Average

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...