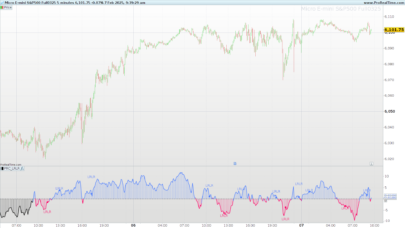

In his article in this issue, “An Elegant Oscillator: Inverse Fisher Transform Redux,” author John Ehlers explains how he uses the inverse Fisher transform to create an indicator he calls the elegant oscillator. First, he describes the Fisher transform before explaining the inverse Fisher transform, which provides normalization by dividing the root mean square (RMS) value into the waveform. The elegant oscillator can be used to spot reversion-to-the-mean opportunities with improved timing capabilities.

|

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 |

//Indicator: TASC FEB 2022 Elegant Oscillator //{ //TASC FEB 2022 //The Elegant Oscillator //(c) 2021 John F. Ehlers //} // Parameters: BandEdge: 20 //Take the derivative of prices Deriv = Close - Close[2] //Normalize to standard deviation RMS = 0 for count = 0 to 49 do RMS = RMS + Deriv[count]*Deriv[count] next if RMS <> 0 then RMS = sqrt(RMS / 50) endif NDeriv = Deriv / RMS //Compute the Inverse Fisher Transform IFish = (exp(2*NDeriv) - 1) / (exp(2*NDeriv) + 1) //Integrate with SuperSmoother once a1 = exp(-1.414*3.14159 / BandEdge) once b1 = 2*a1*cos(1.414*180 / BandEdge) once c2 = b1 once c3 = -a1*a1 once c1 = 1 - c2 - c3 if barindex < 50 + BandEdge then SS = 0 else SS = c1*(IFish + IFish[1]) / 2 + c2*SS[1] + c3*SS[2] endif return SS, 0 |

Share this

No information on this site is investment advice or a solicitation to buy or sell any financial instrument. Past performance is not indicative of future results. Trading may expose you to risk of loss greater than your deposits and is only suitable for experienced investors who have sufficient financial means to bear such risk.

ProRealTime ITF files and other attachments :

Find other exclusive trading pro-tools on ![]()

PRC is also on YouTube, subscribe to our channel for exclusive content and tutorials