Smoothed Rate Of Change (S-ROC)

{kind=link}

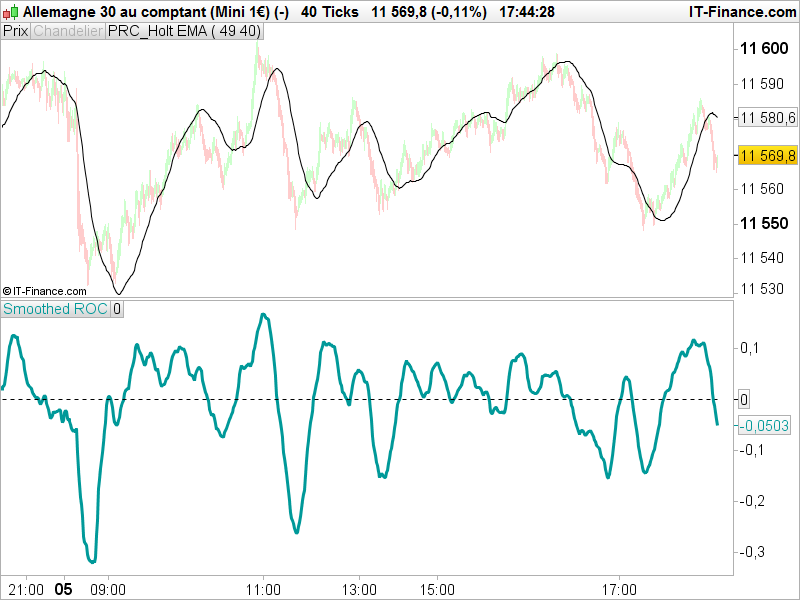

Smoothed Rate of Change (S-RoC) is a refinement of Rate of Change (RoC) that was developed by Fred G Schutzman. It differs from the RoC in that it based on exponential moving averages (EMAs) rather than on price closes. Like the RoC, Smoothed RoC is a leading momentum indicator that can be used to determine the strength of a trend by determining if the trend is accelerating or decelerating. The S-RoC does this by comparing the current EMA to value that the EMA was a specified periods ago. Thus, a 7-day S-RoC compares the current EMA to the value that the EMA was seven days ago. The use of EMAs rather than the price close illuminates the erratic tendencies of the RoC.

RoC is calculated in three steps. First, the EMA is calculated. Then the momentum of the change in the EMA is calculated by subtracting the previous value of the EMA from the current EMA. Finally, the result is divided by the previous value of the EMA and multiplied by 100 to give a percentage. As the S-RoC is a RoC of EMA, it takes two periods: the period of the EMA, with the default being 13; and the period of the RoC, with the default being 21. The formula is: S-RoC = ( Current EMA – Previous EMA ) / ( Previous EMA ) x 100 where the previous EMA is the value that the EMA was at specified period ago. The result is a percentage that is plotted as an oscillator that oscillates between 100% and -100%.

Coded by request on English forum.

//PRC_Smoothed ROC (S-ROC) | indicator

//06.01.2017

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

// --- parameters

//EMAperiod = 13

//ROCperiod = 21

// ---

EMA = exponentialaverage[EMAperiod](close)

SRoC = ( EMA - EMA[ROCperiod] ) / ( EMA[ROCperiod] ) * 100

RETURN SRoC as "Smoothed ROC", 0 as "0"