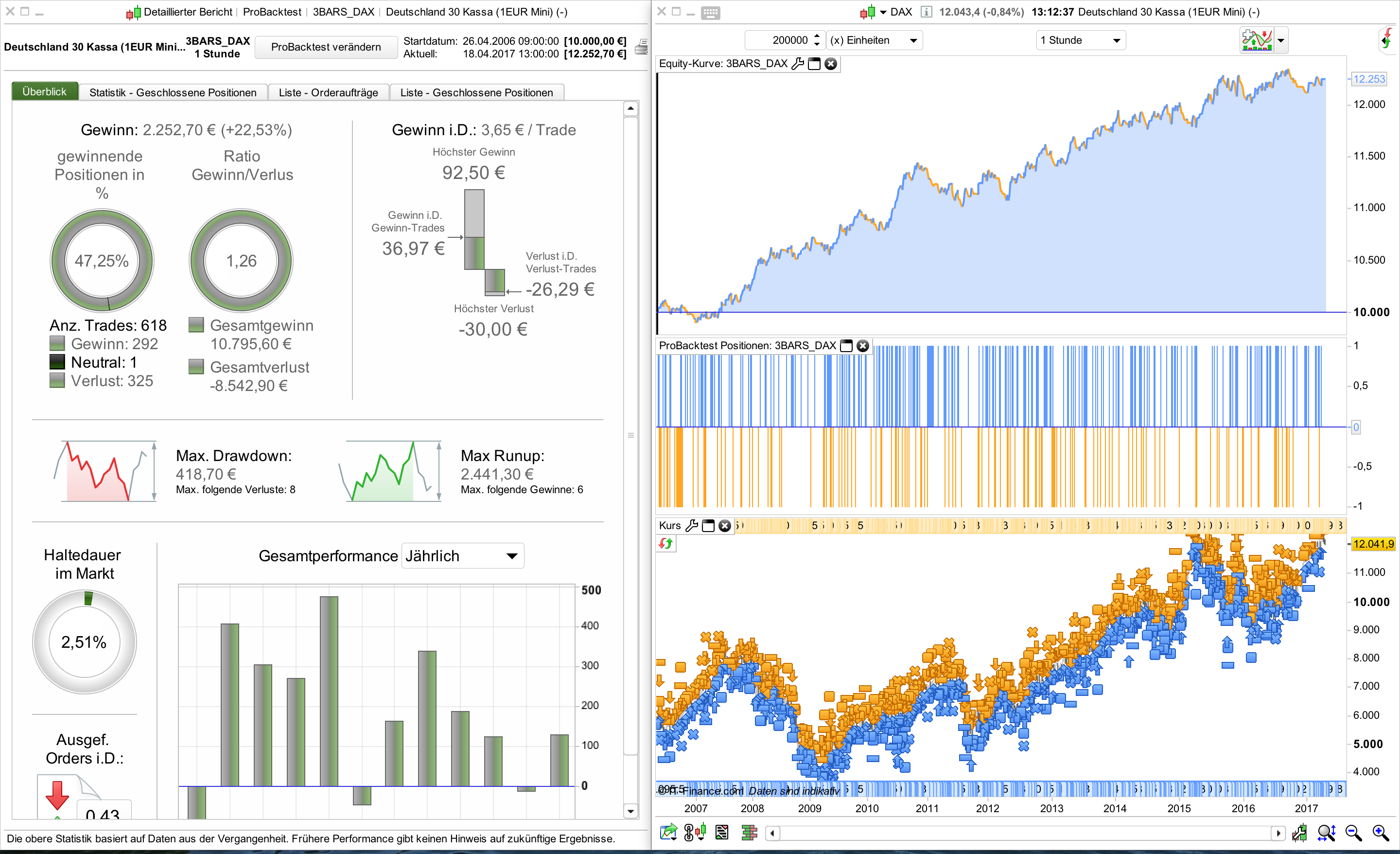

3 bars patterns - DAX intraday trading 1 hour

April 18, 2017, 1:33 PM

Strategies

12 Comments

{kind=link}

Simple 1H strategy on DAX (1EUR)

The aim of this strategy is to take a position after a succession of 3 consecutive candles of the same color. Strict hourly conditions allow the strategy to enter into position only at predetermined fixed times:

- buy orders only at 12:00

- sell orders only at 16:00

Trades are automatically closed at the end of the day.

// DAX (1E) - IG MARKETS

// TIME FRAME 1H

// SPREAD 2.0 PIPS

DEFPARAM CumulateOrders = False

DEFPARAM FLATBEFORE = 100000

DEFPARAM FLATAFTER = 210000

// LONG

IF (time = 120000 and close > open and close[1] > open[1] and close[2] > open[2]) THEN

BUY 1 CONTRACTS AT MARKET

SET STOP pLoss 30

SET TARGET pPROFIT 45

ENDIF

// SHORT

IF (time = 160000 and close < open and close[1] < open[1] and close[2] < open[2]) THEN

SELLSHORT 1 CONTRACTS AT MARKET

SET STOP pLoss 30

SET TARGET pPROFIT 45

ENDIF

Download

Filename:

3-bars-patterns-DAX.itf

Downloads:

494

New

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...