Bollinger Bands + RSI + TDI (EURUSD 30M)

July 21, 2020, 5:34 PM

Strategies

2 Comments

{kind=link}

Hello,

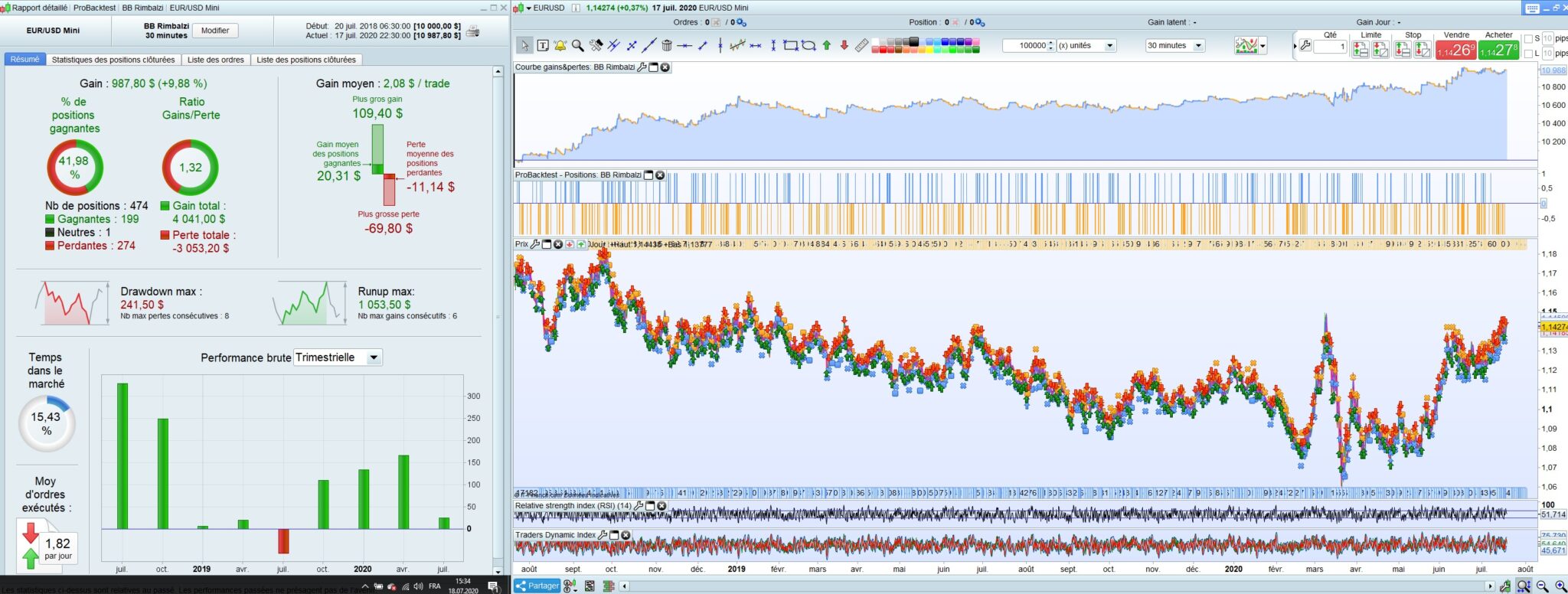

I would like to share with you this first strategy that I have just developed. It is based on the Bollinger, RSI and TDI bands largely inspired by Marc website Doctrading (https://www.youtube.com/watch?v=KxTrCc3GmaY) . The results on the EUR/USD pair in 30 minutes look promising.

But it still needs a lot of optimization and hopefully help from you to get it optimized.

See you soon

Michel

// Definizione dei parametri

DEFPARAM FlatBefore = 070000

DEFPARAM FlatAfter = 230000

DEFPARAM preloadbars = 500

// Numero di contratti

Once nlot = 1

// Variabili indicatori

Once perBB = 20

Once perRSI = 9

Once RSIUp = 62

Once RSIDn = 28

Once DMTSLm = 14 // DMT StopLine -> average ATR

Once DMTSLn = 10 // DMT StopLine -> average price

Once lengthRSI = 13 //TDI

Once lengthband = 34 //TDI

Once lengthrsipl = 2 //TDI

Once lengthtradesl = 7 //TDI

// Caricare indicatori

BBup = BollingerUp[perBB](close)

BBDn = BollingerDown[perBB](close)

RSI1 = RSI[perRSI](close)

// -------- Indicatore DMT StopLine --------------

ATR = AverageTrueRange[DMTSLm](close)

avgATR1 = average[DMTSLm](High+ATR)

avgATR2 = average[DMTSLm](Low-ATR)

AVG1 = average[DMTSLn](High)

AVG2 = average[DMTSLn](low)

IF close > AVG1 THEN

BREAKOUT = 1

ELSIF close < AVG2 THEN

BREAKOUT = -1

ENDIF

IF BREAKOUT = -1 AND avgATR1 > avgATR1[1] THEN

avgATR1 = avgATR1[1]

ELSIF BREAKOUT = 1 AND avgATR2 < avgATR2[1] THEN

avgATR2 = avgATR2[1]

ENDIF

IF BREAKOUT = 1 THEN

StopLINE = avgATR2

ELSE

StopLine = avgATR1

ENDIF

// ------- Indicatore TDI ---------

r = rsi[lengthrsi](close)

ma = average[lengthband](r)

offs = (1.6185 * std[lengthband](r))

up = ma+offs

dn = ma-offs

TDI = average[lengthrsipl](r)

TDI2 = average[lengthtradesl](r)

// Variabili di lavoro

Once cdLong1 = 0

Once cdLong2 = 0

Once cdShort1 = 0

Once cdShort2 = 0

//=============== RICERCA ENTRTY ===============

// Long

IF NOT LongOnMarket THEN

IF not cdLong1 AND close < BBdn AND RSI1 < RSIDn AND TDI < dn THEN

cdlong1 = 1

ENDIF

IF not cdlong2 THEN

cdLong2 = TDI > TDI2

ENDIF

IF cdLong1 AND cdLong2 AND StopLine < close THEN

BUY nlot CONTRACTS AT MARKET

SET STOP LOSS (close - StopLine)

cdLong1 = 0

cdLong2 = 0

ENDIF

ENDIF

//Short

IF not ShortOnMarket THEN

IF not cdShort1 AND close > BBUp AND RSI1 > RSIUp AND TDI > up THEN

cdShort1 = 1

ENDIF

IF not cdShort2 THEN

cdShort2 = TDI < TDI2

ENDIF

IF cdShort1 AND cdShort2 AND StopLine > close THEN

SELLSHORT nlot CONTRACTS AT MARKET

SET STOP LOSS (StopLine - close)

cdShort1 = 0

cdShort2 = 0

ENDIF

ENDIF

// =============== USCITA TRAD ===============

//Long

IF LongOnMarket AND close < StopLine THEN

SELL AT MARKET

ENDIF

// Short

IF ShortOnMarket AND close > StopLine THEN

EXITSHORT AT MARKET

ENDIF

Download

Filename:

BB-Rimbalzi.itf

Downloads:

723

Junior

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...