Breakout Failures DAX 5m

October 30, 2017, 8:50 AM

Strategies

7 Comments

{kind=link}

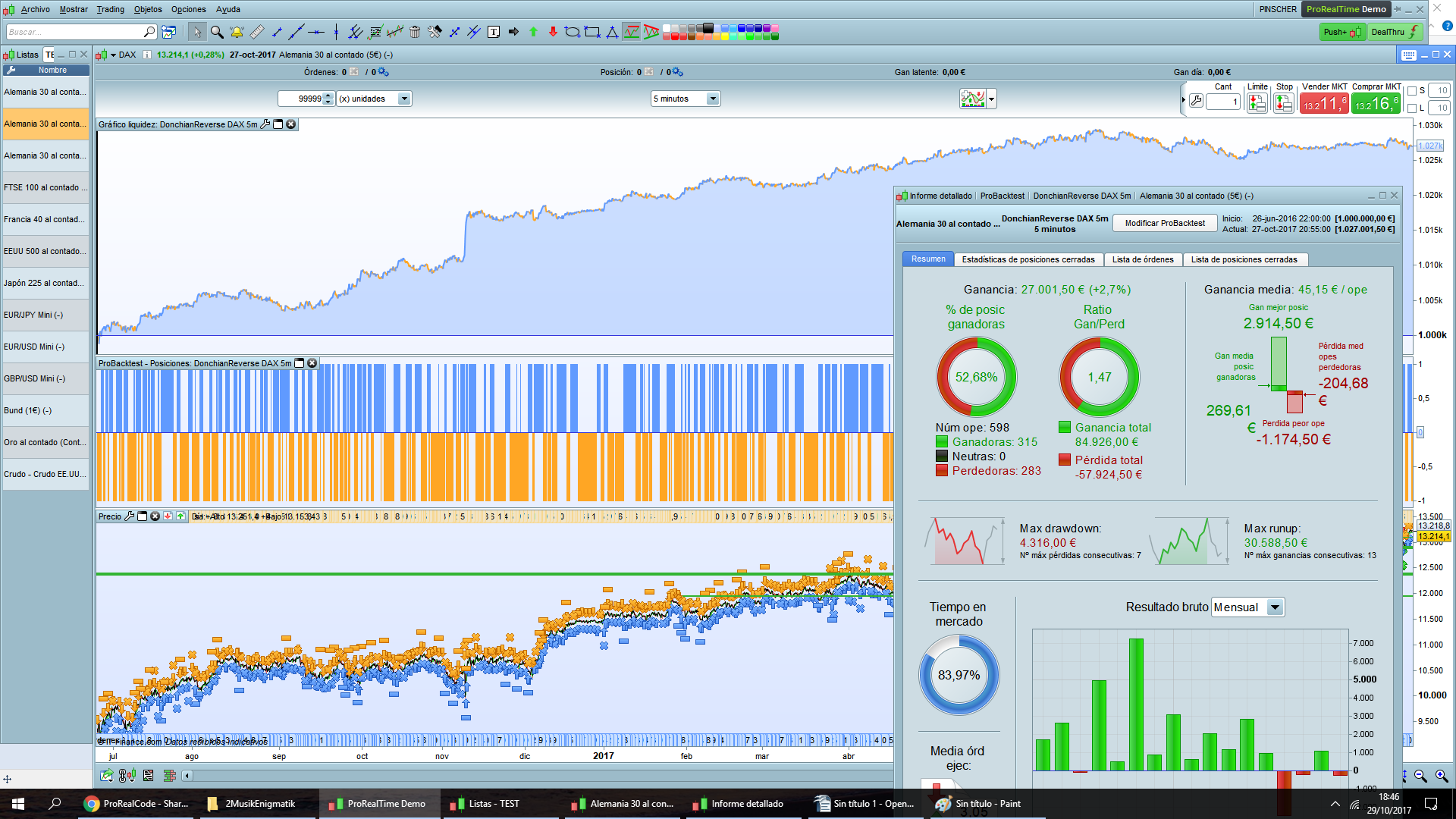

This is a simple strategy, just an idea that seems to work. No MoneyManagement or Position Size. Optimized for DAX 5 minutes.

It looks for breakouts in Donchian Channel for going in the opposite direction, trying to catch breaout failures so kind of mean reversion system. There is no Stop, when the losses reach 10xATR it changes (“flip”) direction to catch the trend that seems to be forming. Also finish tradings at 20:30, kind of time stop with no overnight.

// System parameters

DEFPARAM CumulateOrders = False

DEFPARAM PRELOADBARS = 20

//DEFPARAM FLATBEFORE = 000000

DEFPARAM FLATAFTER = 203000

// Condiciones de entrada

myUpperband, myLowerband, ignored = CALL "Donchian (canal)"[8]

c1 = close < myLowerband

c2 = close > myUpperband

// Conditions for Entry of Long Positions

IF c1 AND NOT ONMARKET THEN

BUY 1 CONTRACTS AT MARKET

ELSIF SHORTONMARKET AND (CLOSE-TRADEPRICE) > FlipPosition THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

// Conditions for Entry of Short Positions

IF c2 AND NOT ONMARKET THEN

SELLSHORT 1 CONTRACTS AT MARKET

ELSIF LONGONMARKET AND (CLOSE-TRADEPRICE) < -FlipPosition THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

// Loss, Profit

//SET STOP LOSS 15*AverageTrueRange[10](close)

SET TARGET PROFIT 15*AverageTrueRange[12](close)

FlipPosition = 10*AverageTrueRange[12](close)

// ENDDonchian channel indicator (should be set as a new indicator)

//N=10 //variable to add as an external one

IF BarIndex > N THEN

upperBand = Highest[N](High)

lowerBand = Lowest[N](Low)

middleBand = (upperBand + lowerBand)/2

ELSE

upperBand = Undefined

lowerBand = Undefined

middleBand = Undefined

ENDIF

RETURN upperBand[1] AS "Upper band" , lowerBand[1] AS "Lower band" , middleBand[1] COLOURED(0,255,0) AS "Middle band"

Download

Filename:

Donchian-canal.itf

Downloads:

436

Download

Filename:

DonchianReverse-DAX-5m.itf

Downloads:

544

Veteran

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...