BreakOut - SAR - Index - 15m - (DJIA-DAX-PXI)

April 25, 2016, 10:10 PM

Strategies

15 Comments

{kind=link}

Hi everyone!

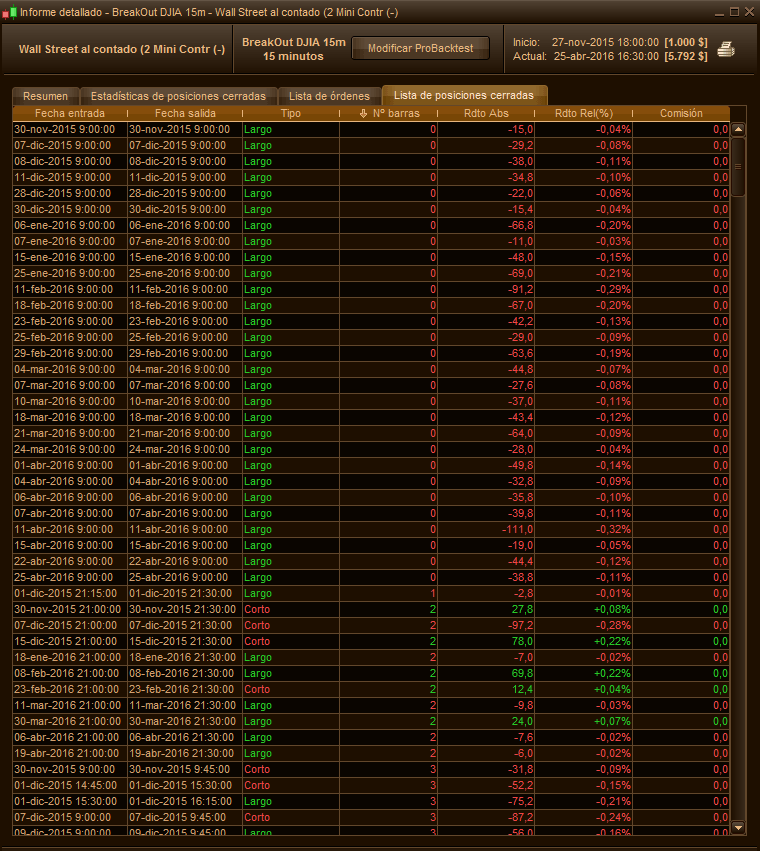

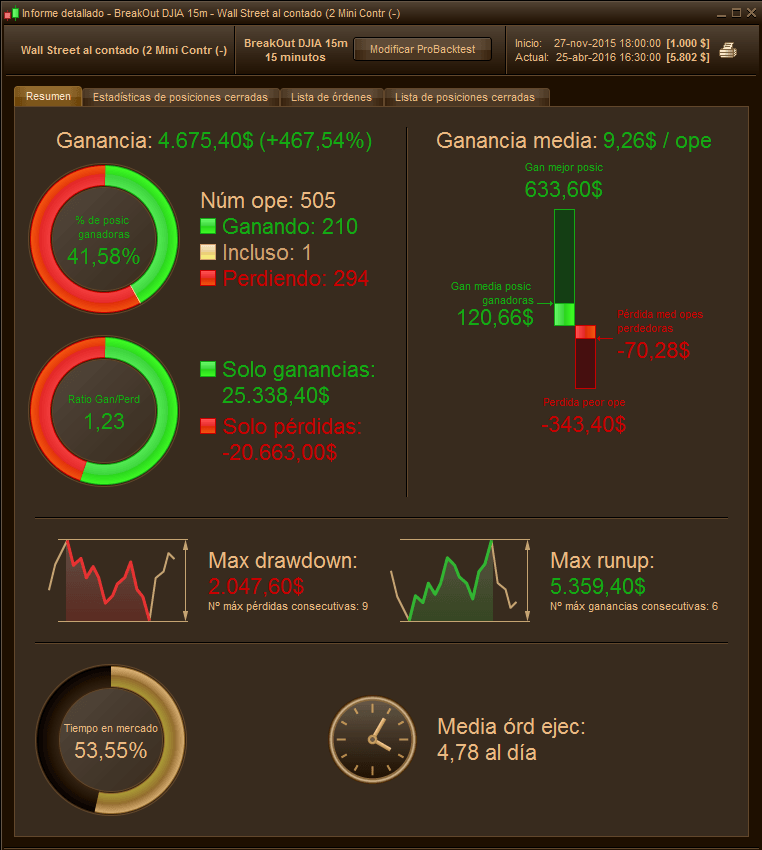

This strategy buy or sell if price breaks max or min night range with an “spread” difference (optimized by variable “s”), and then is stopped at SAR crosses.

It has money-management included, system will calculate risk before setting up orders and join with the contracts updated with “STRATEGYPROFIT” var.

I’m thinking to trade it real mode and maybe you could help me to improve it, is my really first one you know…

Best wishes!

REM Cumulate orders

DEFPARAM CumulateOrders=true

REM Operative time

DEFPARAM FlatBefore = 090000

DEFPARAM FlatAfter = 212900

REM Indicadores

parabolic = SAR[0.02,0.02,0.2]

REM Variables

maximo = Highest[4](high)

minimo = Lowest[4](low)

ultimotrade = BARINDEX-TRADEINDEX

REM Condiciones

C1 = PARABOLIC>HIGH

C2 = PARABOLIC<LOW

C3 = uLtimotrade>1

if time=080000 then

maximoN=dhigh(0)

minimoN=dlow(0)

endif

REM CONFIGURACION DE ESTRATEGIA

REM GESTION MONETARIA

REM Cálculo de contratos a operar

capitalinicial = c //Capital

riesgo = r // riesgo por operación

spread = s

equity = capitalinicial+strategyprofit

maxriesgo = round(equity*riesgo)

pipstop = abs(round(maximo-minimo))

myLOT = abs(round(((maxriesgo/pipstop)/PointValue)*pipsize))

if mylot<1 then

mylot=1

else

myLOT = abs(round(((maxriesgo/pipstop)/PointValue)*pipsize))

endif

REM PRIMERA COMPRA

IF TIME>=090000 AND TIME<=094500 AND NOT ONMARKET AND C3 THEN

REM ENTRAR AL MERCADO DENTRO DEL RANGO

IF CLOSE<maximoN and CLOSE>minimoN and c1 then

sellshort myLOT contract at minimoN-spread*pipsize stop

buy myLOT contract at parabolic+spread*pipsize limit

ENDIF

IF CLOSE<maximoN and CLOSE>minimoN and c2 AND C3 then

sellshort myLOT contract at parabolic-spread*pipsize stop

buy myLOT contract at maximoN+spread*pipsize limit

ENDIF

REM ENTRAR AL MERCADO POR ENCIMA DEL RANGO

IF CLOSE>maximoN and c2 AND C3 then

buy myLOT contract at market

endif

REM ENTRAR AL MERCADO POR DEBAJO DEL RANGO

IF CLOSE<minimoN and c1 AND C3 then

sellshort myLOT contract at MARKET

endif

ENDIF

rem si estoy largo

if longonmarket and c1 AND C3 then

breakeven = minimo

SELLSHORT AT minimo STOP

endif

if longonmarket and c2 AND C3 then

breakeven = parabolic

sellSHORT at breakeven-spread*pipsize stop

endif

rem si estoy corto

if shortonmarket and c1 AND C3 then

breakeven = parabolic

BUY at breakeven+spread*pipsize stop

endif

if shortonmarket and c2 AND C3 then

breakeven = maximo

BUY at breakeven+spread*pipsize stop

endif

No confusing closes at bar 0. +info

{kind=link}

Download

Filename:

BREAKOUT-SAR-INDEX.itf

Downloads:

277

Download

{kind=link}

Filename:

Informe-detallado-1-Breakout-djia-15m.png

Downloads:

112

Senior

A ProRealTrader.

I'm here to learn as much as I can, and improve my skills every single day!

Author’s Profile

Loading...