Buy if the price has fallen

February 15, 2022, 9:36 AM

Strategies

10 Comments

{kind=link}

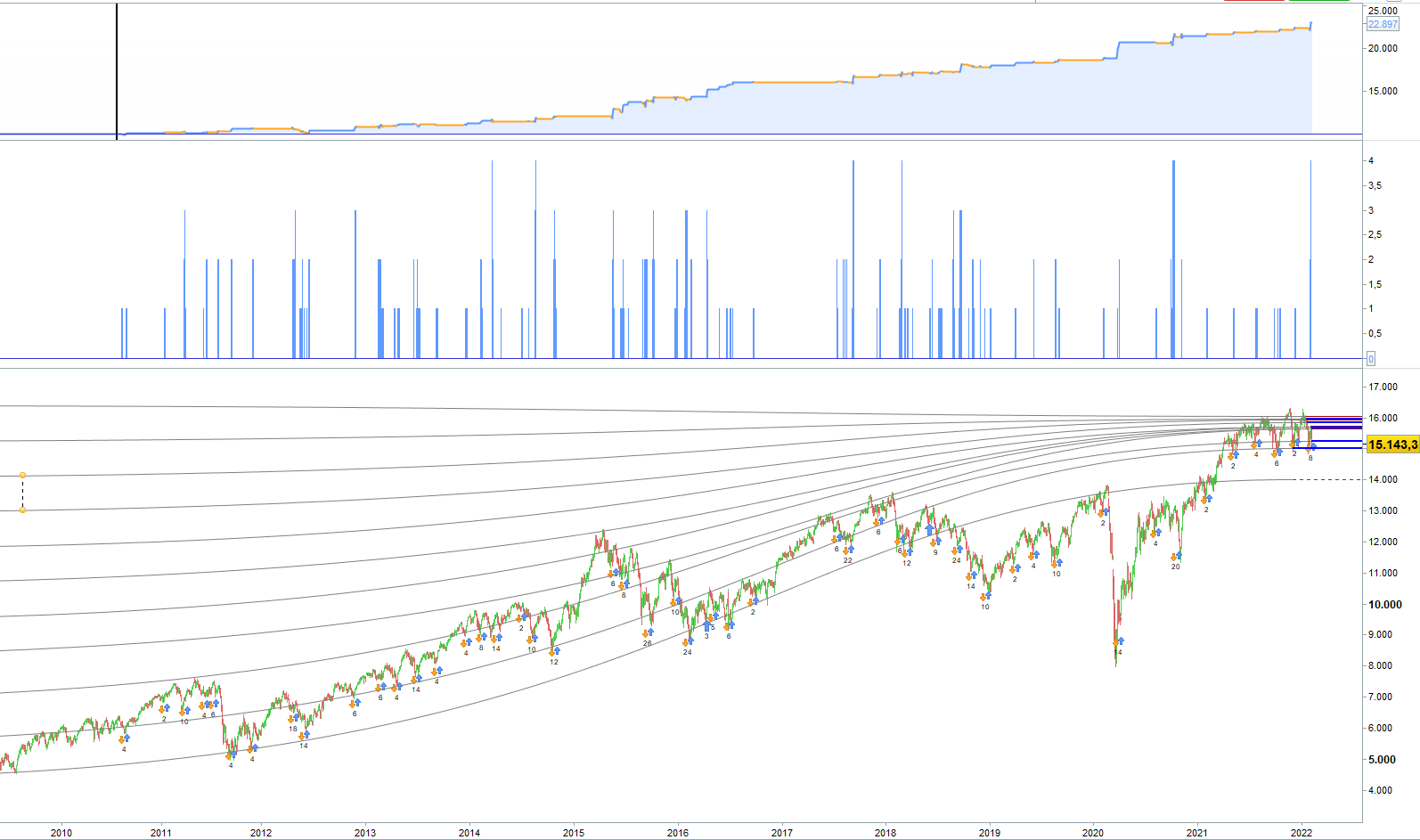

We buy when the price is below the EMA200 and above the EMA50 (sik!).

As a filter we use a simple linear regression slope.

We sell when the price is above the EMA28 and below the EMA7.

It really couldn’t be easier

thats all for today

until then

//-------------------------------------------------------------------------

// maincode : everytimelong g50 k100 lrs

//-------------------------------------------------------------------------

// ger40 longonly strategie

// timezone europe, berlin

// timeframe 4h

// created and coded by johnscher

defparam cumulateorders = true // false is working well

once ordersize = 1

TradingDay = Opendayofweek = 1 or Opendayofweek = 2 or Opendayofweek = 3 or Opendayofweek = 4 or Opendayofweek = 5

TradingTime = time >= 090000 and time <= 170000

c1 = close > Exponentialaverage [50] (close)

c2 = close < Exponentialaverage [100] (close)

c3 = close > close [1]

c4 = LinearRegressionSlope[100] (close) < 0

IF TradingDay and TradingTime then

If c1 and c2 and c3 and c4 then

buy ordersize contract at market

Endif

ENDIF

c5 = close < Exponentialaverage [7] (close)

c6 = close > Exponentialaverage [28] (close)

IF longonmarket then

If c5 and c6 then

sell at market

Endif

Endif

Set Stop %Loss 10 //as insurance

Set Target %profit 2.75

Download

Filename:

Buy-if-the-price-has-fallen.itf

Downloads:

650

Veteran

Code artist, my biography is a blank page waiting to be scripted. Imagine a bio so awesome it hasn't been coded yet.

Author’s Profile

Loading...