Cumulative RSI 2 periods strategy

{kind=link}

Long only strategy that performs extremely well on any world indices and beyond on a daily timeframe. I will certainly do much exploration of this very short term mean reversion strategy, as it seems very powerful without doing any change on triggers.

The main trigger is based of a “cumulated RSI” over the 2 recent periods while trade are launch only if the price Close is above a 200 period moving average.

When the cumulated RSI enter in oversold territory, we expect the price to return to its mean, on the bullish trend. We exit the market when the CRSI gain overbought area above the 65 level.

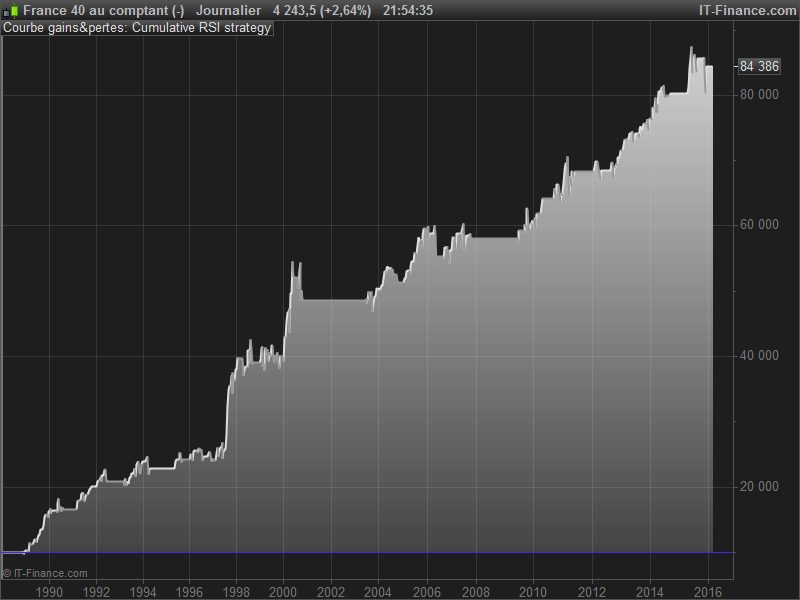

As for my current test : (with exactly the same code on CFDs)

CAC40 : (featuring picture) : 10€ /contracts, 1 contract per trade since 1988 = +370% / % Drawdown max = 12.7%

IBEX35 : 2€ / contract, 1 contract per trade since 1994 = +134.33% / % Drawdown max = 25.6%

SP500 : 1€ / contract, 10 contract per trade since 1984 = +95.33% / % Drawdown max = 8.08%

//indicator

Period = 2

CUMRSI = SUMMATION[Period](RSI[Period](close))

AVG = average[200](close)

//initial lot

initLOT = 10

IF NOT LongOnMarket AND Close>AVG AND CUMRSI<35 THEN

BUY initLOT CONTRACTS AT MARKET

ENDIF

If LongOnMarket AND CUMRSI>65 THEN

SELL AT MARKET

ENDIF