Dax adaptable strategy Breakout/Mean reversion

{kind=link}

Dear all

I have elaborated a little over an idea originally posted in the forum by Bjoern posted as True Range Breakout EUR/USD.

I applied to the Dax with the additional feature of switching from a breakout to a mean reversion strategy depending on some optimized value of the ADX indicator.

The strategy is a breakout strategy when the adx is above a certain value and a mean reverting strategy when ADX value is below that same value.

I have optimized it on several time frame and the results look quite promising, it would be great if someone think of a better way of discriminate between range trading vs trending phases. I have used the popular ADX indicator, but I am sure there are more efficient way to look at phase transitions in market.

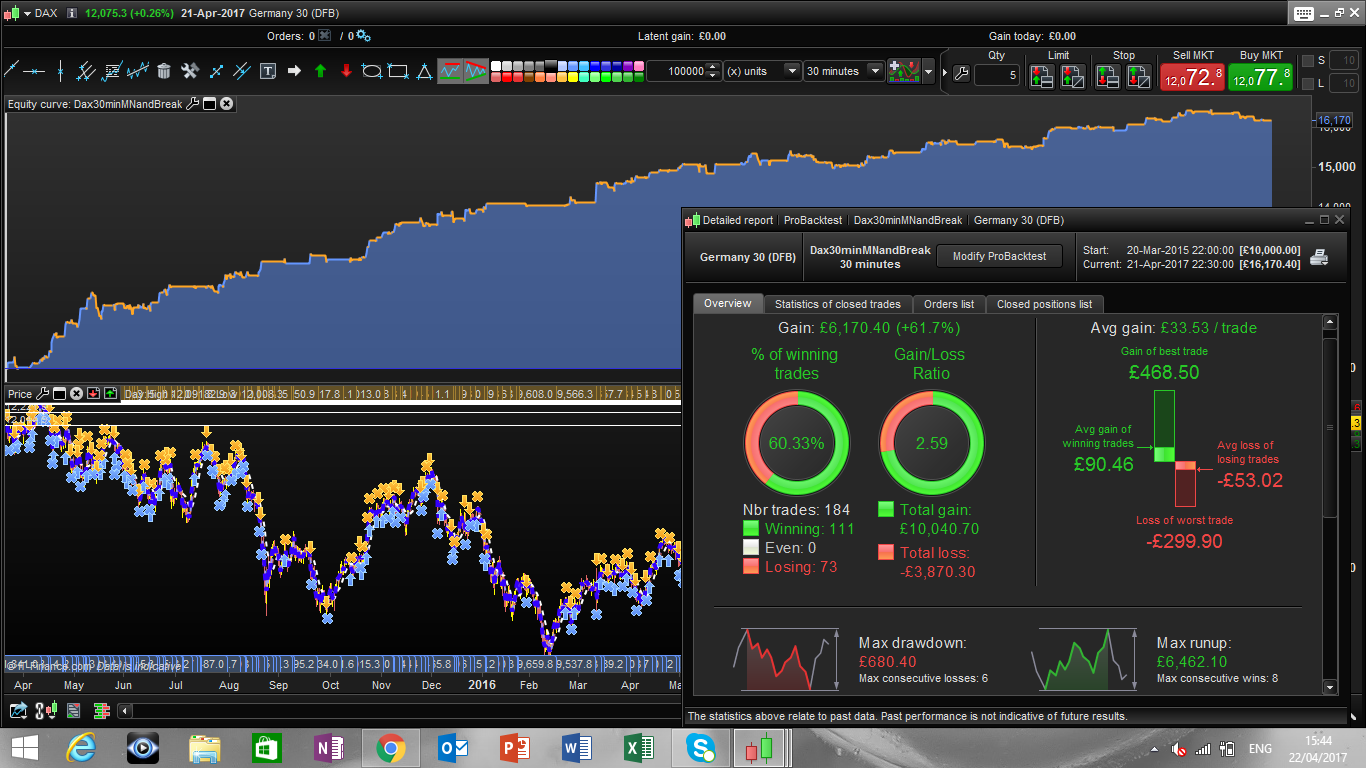

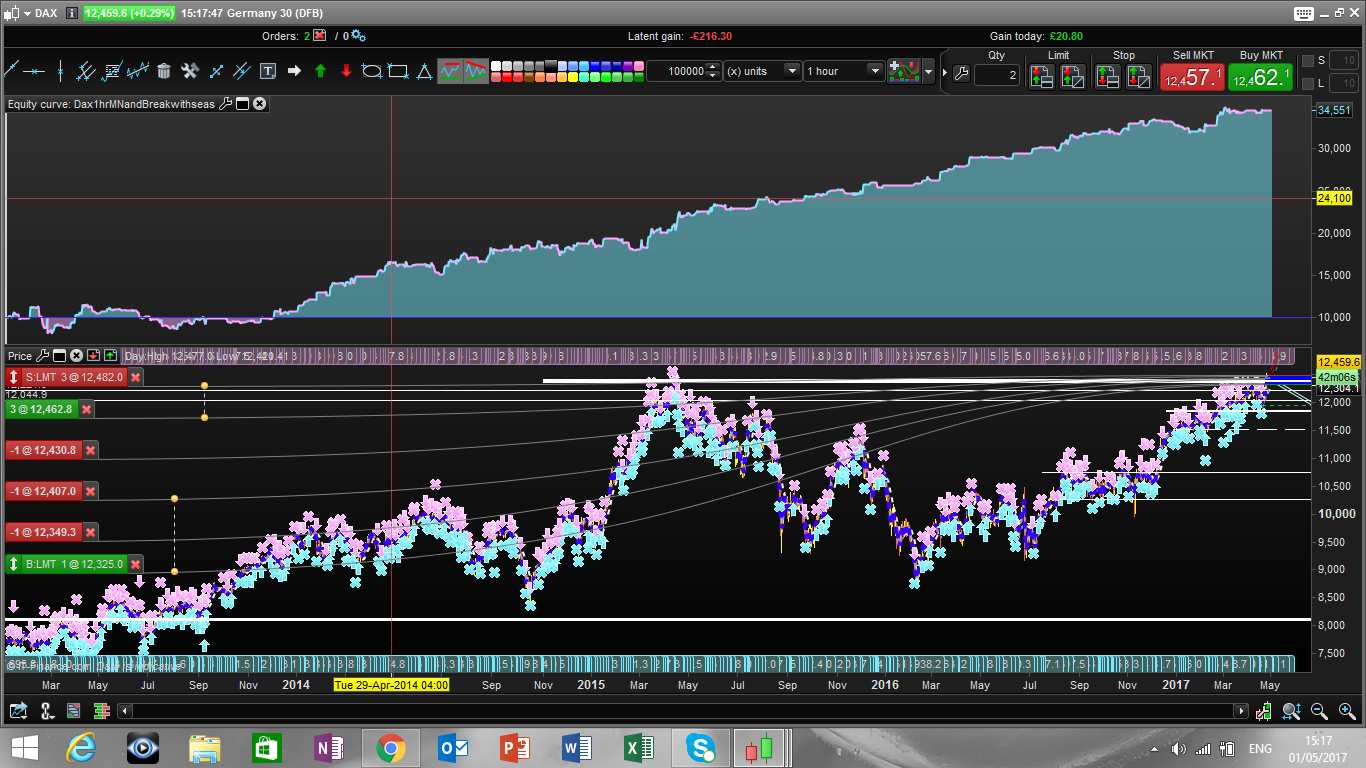

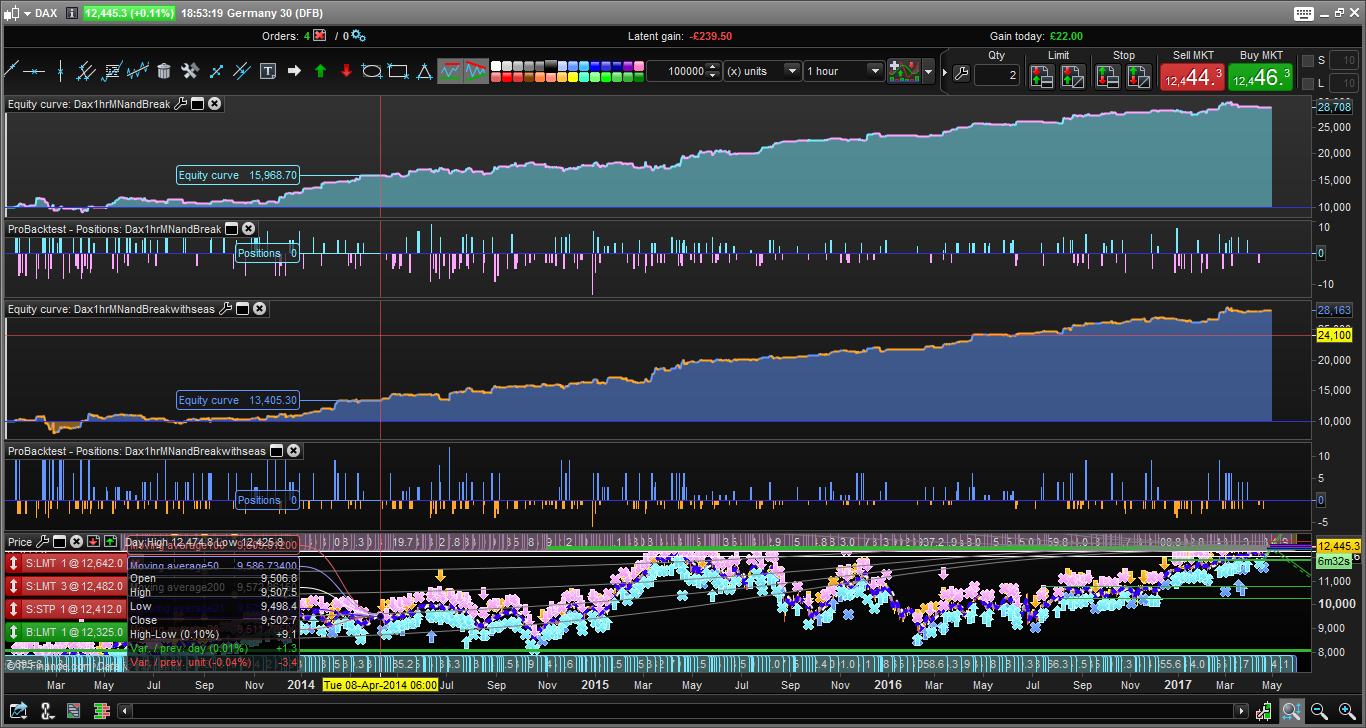

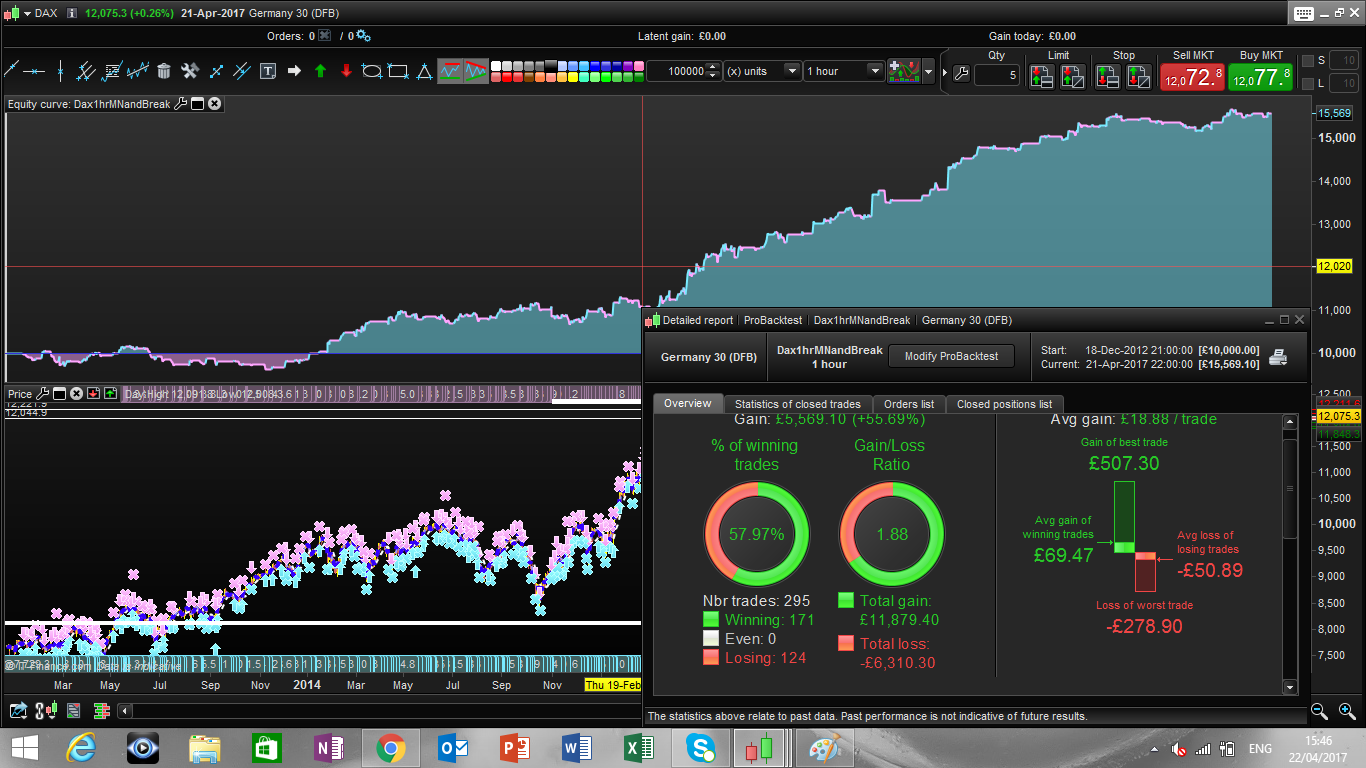

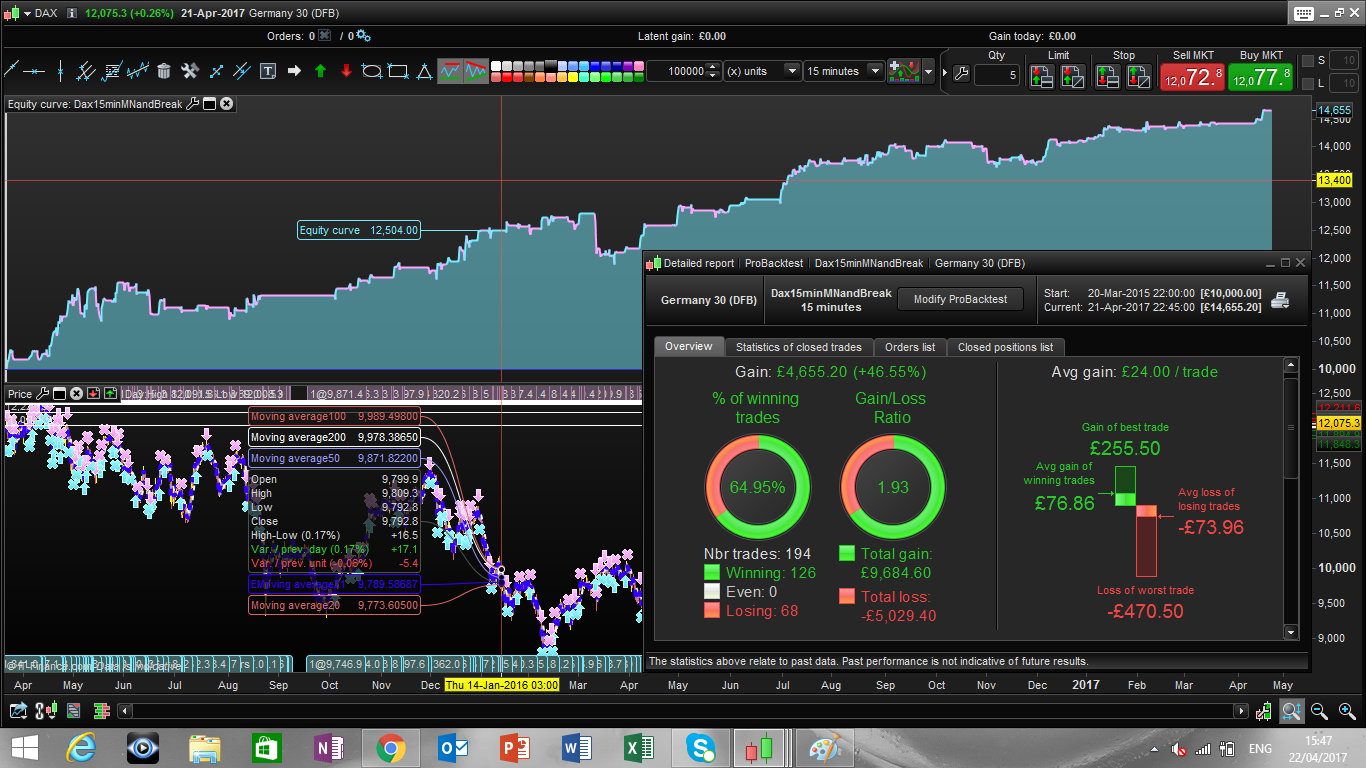

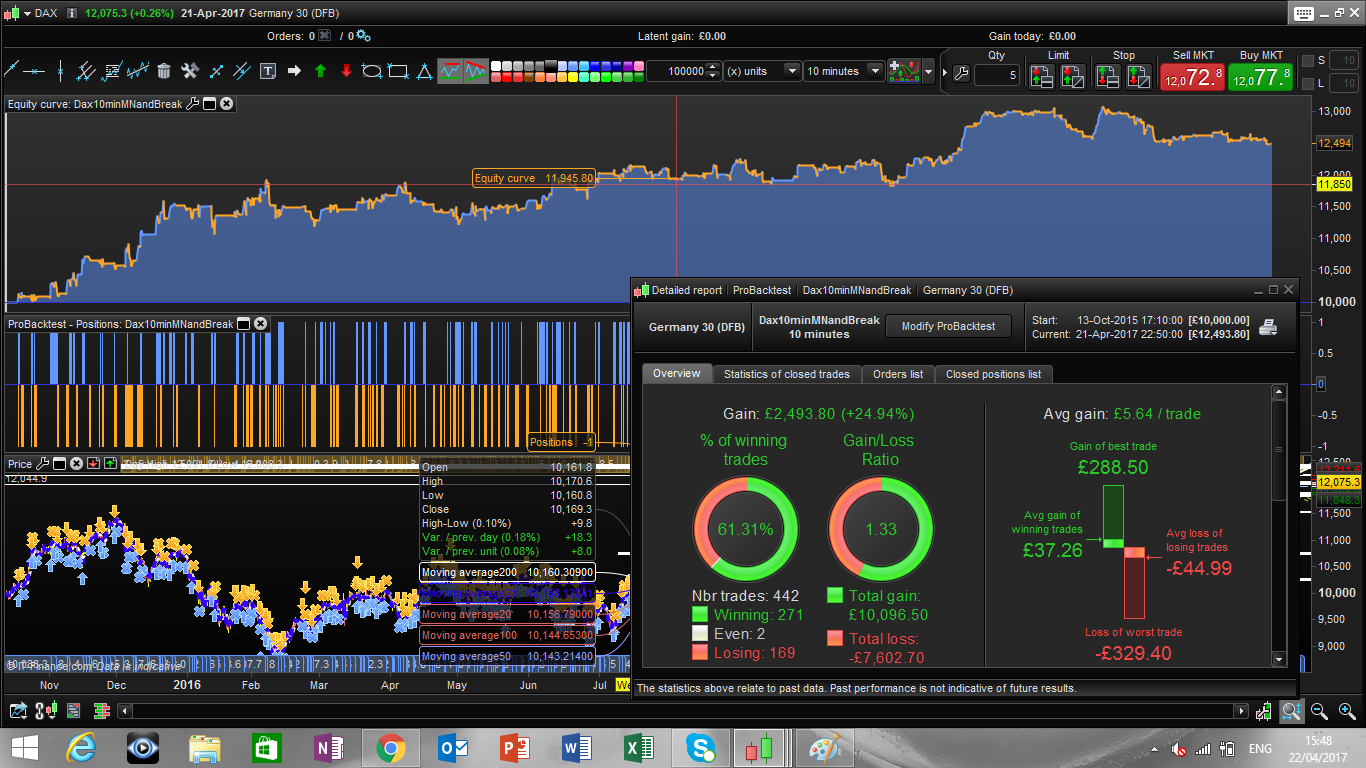

The results for different time frames are attached, together with the 30minutes code.

Best Regards

Francesco

DEFPARAM CumulateOrders = False

DEFPARAM FLATBEFORE =080000

DEFPARAM FLATAFTER =210000

adxval = 20

ATRperiod = 12

adxperiod = 15

indicator1 = adx[adxperiod]

atr = AverageTrueRange[ATRperiod]

m = 3

n = 2

c1 = indicator1 <adxval

c2 = indicator1 >adxval

if c1 then

// short

IF (abs(open-close) > (atr*m) and close > open) THEN

sellshort 1 CONTRACTS AT MARKET

//SET STOP pLOSS losses

//SET TARGET pPROFIT profits

ENDIF

//long

IF (abs(open-close) > (atr*m) and close < open) THEN

buy 1 CONTRACTS AT MARKET

//SET STOP pLOSS losses

//SET TARGET pPROFIT profits

ENDIF

endif

if c2 then

// long

IF (abs(open-close) > (atr*n) and close > open and close> Dhigh(1)) THEN

buy 1 CONTRACTS AT MARKET

//SET STOP pLOSS losses

//SET TARGET pPROFIT profits

ENDIF

//short

IF (abs(open-close) > (atr*n) and close < open and close< Dlow(1)) THEN

sellshort 1 CONTRACTS AT MARKET

//SET STOP pLOSS losses

//SET TARGET pPROFIT profits

ENDIF

endif

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}