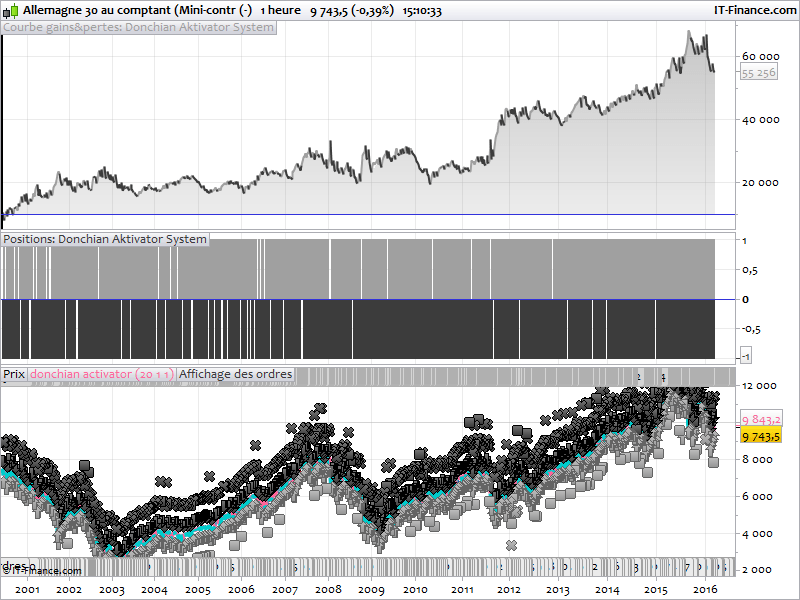

DAX Donchian breakout Aktivator 1 hour

March 8, 2016, 3:22 PM

Strategies

4 Comments

{kind=link}

This automatic trading strategy on DAX GER30 is made of the indicator “Donchian Channel Activator Factor” available in the Library here : http://www.prorealcode.com/prorealtime-indicators/donchian-channel-activator-factor/

This system is a simple one, based on breakout of the recent highest or lowest on a 1 hour timeframe. Each trade has a stoploss made of the difference from the current close to last indicator value (upper or lower channel).

Test were made with 1 point spread, on mini-DAX CFD from ProRealTime-Trading.

//parameters

pd = 20

Factor = 1

ot = 1

//indicators

hi = HIGHEST[pd](high)[ot]

lo = LOWEST[pd](low)[ot]

DUpper=hi+Factor*AverageTrueRange[pd](close)

DLower=lo-Factor*AverageTrueRange[pd](close)

// case BUY

IF NOT LongOnMarket AND Close>hi AND Close[1]<hi THEN

BUY 1 CONTRACTS AT MARKET

stoploss = close-DLower

ENDIF

// exit BUY position

If LongOnMarket AND Close<lo THEN

SELL AT MARKET

ENDIF

//case SELL

IF NOT ShortOnMarket AND Close<lo AND Close[1]>lo THEN

SELLSHORT 1 CONTRACTS AT MARKET

stoploss = DUpper-close

ENDIF

// exit SELL position

IF ShortOnMarket AND Close>hi THEN

EXITSHORT AT MARKET

ENDIF

SET STOP LOSS stoploss

Download

Filename:

Donchian-Aktivator-System.itf

Downloads:

261

Legend

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...