The "DAX Donchian Breakout" strategy

March 18, 2018, 6:01 PM

Strategies

8 Comments

{kind=link}

Hi all,

Here is one of my simple strategies. With a little help from someone, here is the code with optimization.

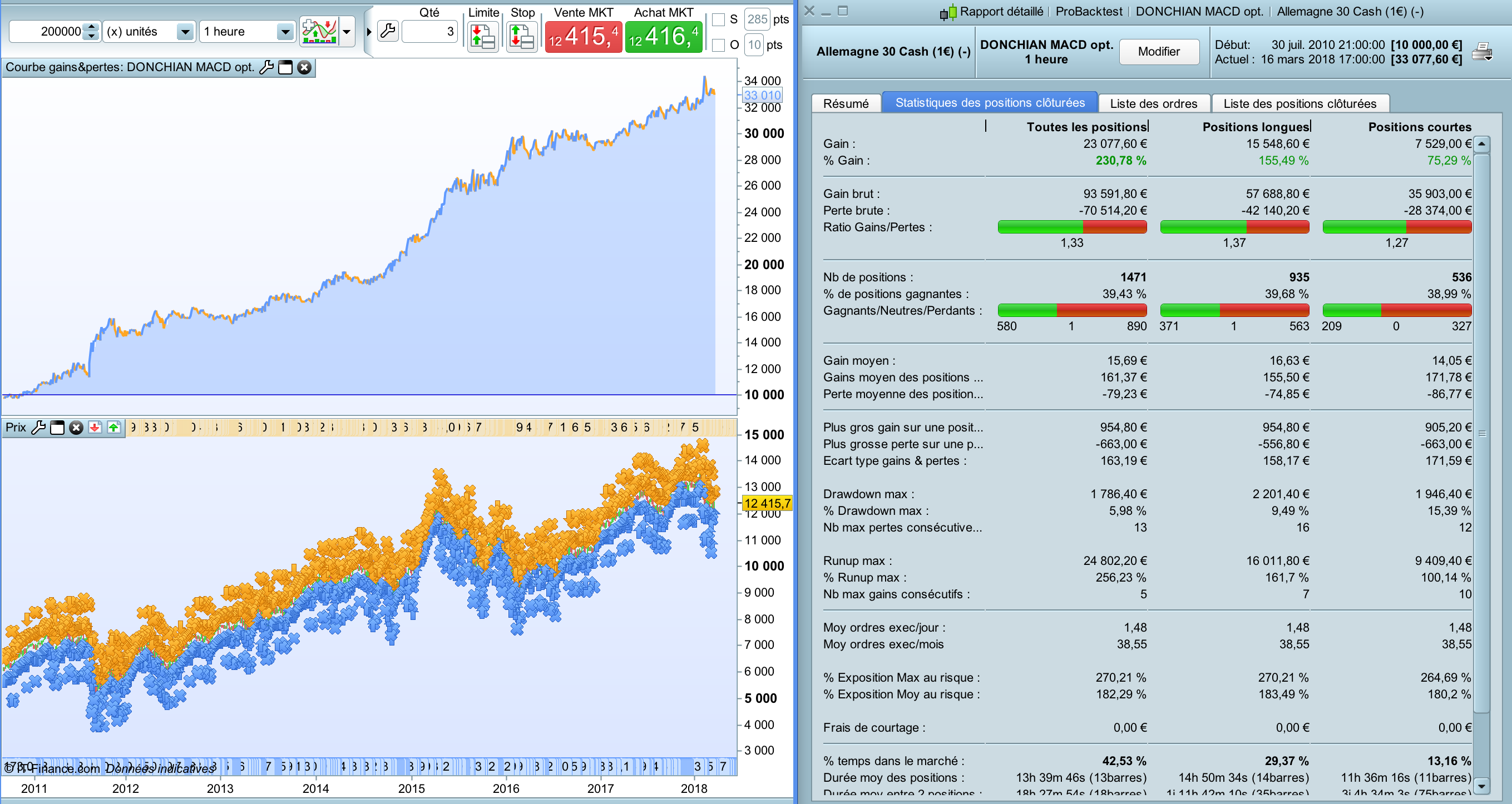

The strategy is using Donchian breakout, with MACD, RSI and moving average as trending indicators.

The code is so simple that I won’t write a long description.

Seems to be effective !

Best regards,

This strategy is suitable for : DAX, H1 (1 point spread, tick by tick)

// ALLEMAGNE 30

// H1

DEFPARAM CumulateOrders = False

// TAILLE DES POSITIONS

N = 2

// MACD histogramme

iMACD = MACD[12,26,9](close)

// Donchian

// Pour le DAX : A = 9 et V = 7

A= 9

V = 7

DonchianSupA = highest[A](high)

DonchianInfA = lowest[A](low)

DonchianSupV = highest[V](high)

DonchianInfV = lowest[V](low)

iRSI= RSI[4](close)

// ACHAT

ca1 = iMACD > iMACD[1]

ca2 = iMACD >= 0

ca3 = close crosses over DonchianSupA[1]

ca4 = iRSI > 63

ca5 = close >= average[50]

IF ca1 AND ca2 AND ca3 and ca4 and ca5 THEN

buy N shares at market

ENDIF

sell at DonchianInfA stop

// VENTE

cv1 = iMACD < iMACD[1]

cv2 = iMACD <= 0

cv3 = close crosses under DonchianInfV[1]

cv4 = iRSI < 31

cv5 = close <= average[500]

IF cv1 AND cv2 AND cv3 and cv4 and cv5 THEN

sellshort N shares at market

ENDIF

exitshort at DonchianSupV stop

Download

Filename:

DAX-Donchian-Breakout-strategy.itf

Downloads:

1242

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...