DI TEMA Trendfollowing strategy on DAX 5 min

{kind=link}

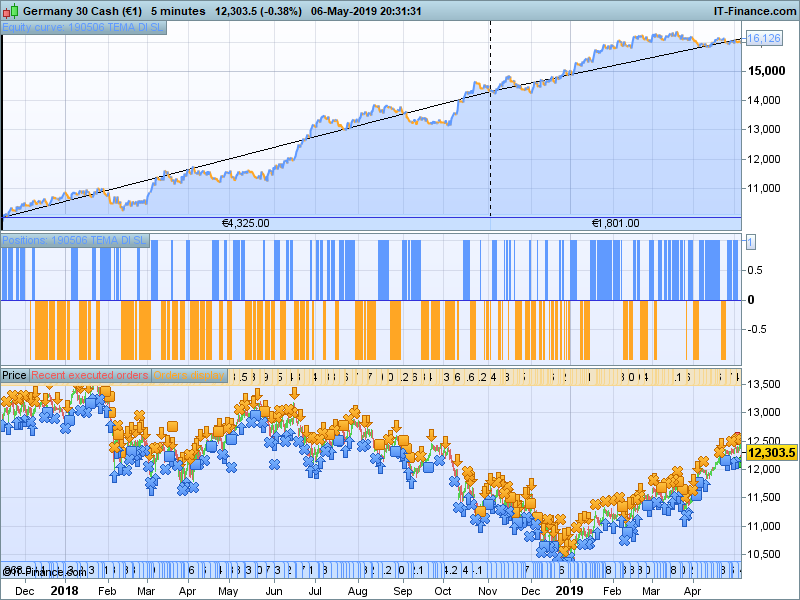

Please find below a simple strategy based on a combination of the DI and TEMA indicators.

It performs quite well on the DAX 5 minutes (7:00-22:00 trading), for 100.000 bars, spread 5 pips.

Conditions to OPEN positions (see settings in the code)

1 TEMA trend turn into positive (for long) or turns into negative (for short)

2 the DI increases, but starts from below zero (Long) or decreases, but starts from above zero (short)

The only CLOSE conditions are a Trailing stop loss, whereby the Trailing stop is reduced after 12 trading bars.

I tried it on several indices in different timeframes, I only got good results for the DAX, 5 minutes bar.

Disadvantage of this strategy is the long TTM, Time in the Market, of at least 65 %, obviously also overnight.

As a spread I have taken into account 5 pips, which should include 3 pips for interest to be paid (estimation 4% x exposure 12.000 Euro for 1 contract x 65% in the market / 120 trades per year)

This strategy requires a bit different settings for 2019 alone (for better results) compared to the settings set in the code for the whole period of 100.000 bars. I am (obviously!) looking for automated setting adjustments during different structures of market movements, any suggestions are more then welcome.

Any suggestions for improvement welcome !

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

//VARIABLES

once SLperc = 105 // Stoploss percentage 105/10000 * Close

once TrailSLPerc = 85 // Trailng Stoploss percentage 85/10000 * Close

once Tema2 = 30 // Tema setting for opening long/short positions

once DI2 = 7 //DI setting for opening long/short positions

once Duration = 12 // number of bars in trade before reducing the trailing stop

once Factor = 7/10//factor to reduce trailing stoploss after some time in the trade

once StartE = 74500 //start time for opening positions

once StartL = 103000 //ending time for opening positions (only trading in the morning)

once N = 1 // initieel aantal contracten

OTD = Barindex - TradeIndex(1) > IntradayBarIndex // limits the (opening) trades till 1 per day

//Setting Stop loss and trailing stop loss //Dynamic for indices

once SL = round(close * SLPerc/10000)

once trailingstop = round(close * (TrailSLPerc)/10000)

// Conditions to OPEN positions

//1/TEMA trend turn into positive(long) or turns into negative (short)

//2/ DI increases, but starts negative (Long) or decreases, but starts with positive value (short)

// Conditions to CLOSE positions

//1/Trailing stop loss hit

//2 Trailing stop is reduced after 12 trading bars

iTema = TEMA[Tema2](close) //default TEMA 20

iDI = TEMA[3](DI[DI2](close)) //default TEMA 14

if time >= StartE And time <= StartL and OTD and not onmarket then

IF iTema > iTema[1] and iTema[1] < iTema[2] and iDI > iDI[1] and iDI < 0 then

BUY N shares AT MARKET

SET STOP ploss SL

// long sell conditie (bovengeschikt aan short sell and dligneJ < Avd

else

IF iTema < iTema[1] and iTema[1] > iTema[2] and iDI < iDI[1] and iDI > 0 THEN

SELLSHORT N shares AT MARKET //short sell conditie

SET STOP pLOSS SL

endif

endif

endif // einde aankoop

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if barindex - tradeindex(1) > Duration then //normal trailing stop adjusted for factor, which decreases trailing stip

if tradeprice(1)-MINPRICE >= Factor * trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE + Factor * trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

else //normal trailing stop

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if barindex - tradeindex(1) > 12 then //normal trailing stop adjusted for factor, which decreases trailing stip

if MAXPRICE-tradeprice(1)>= Factor * trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE- Factor * trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

else //normal trailing stop

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

{kind=link}