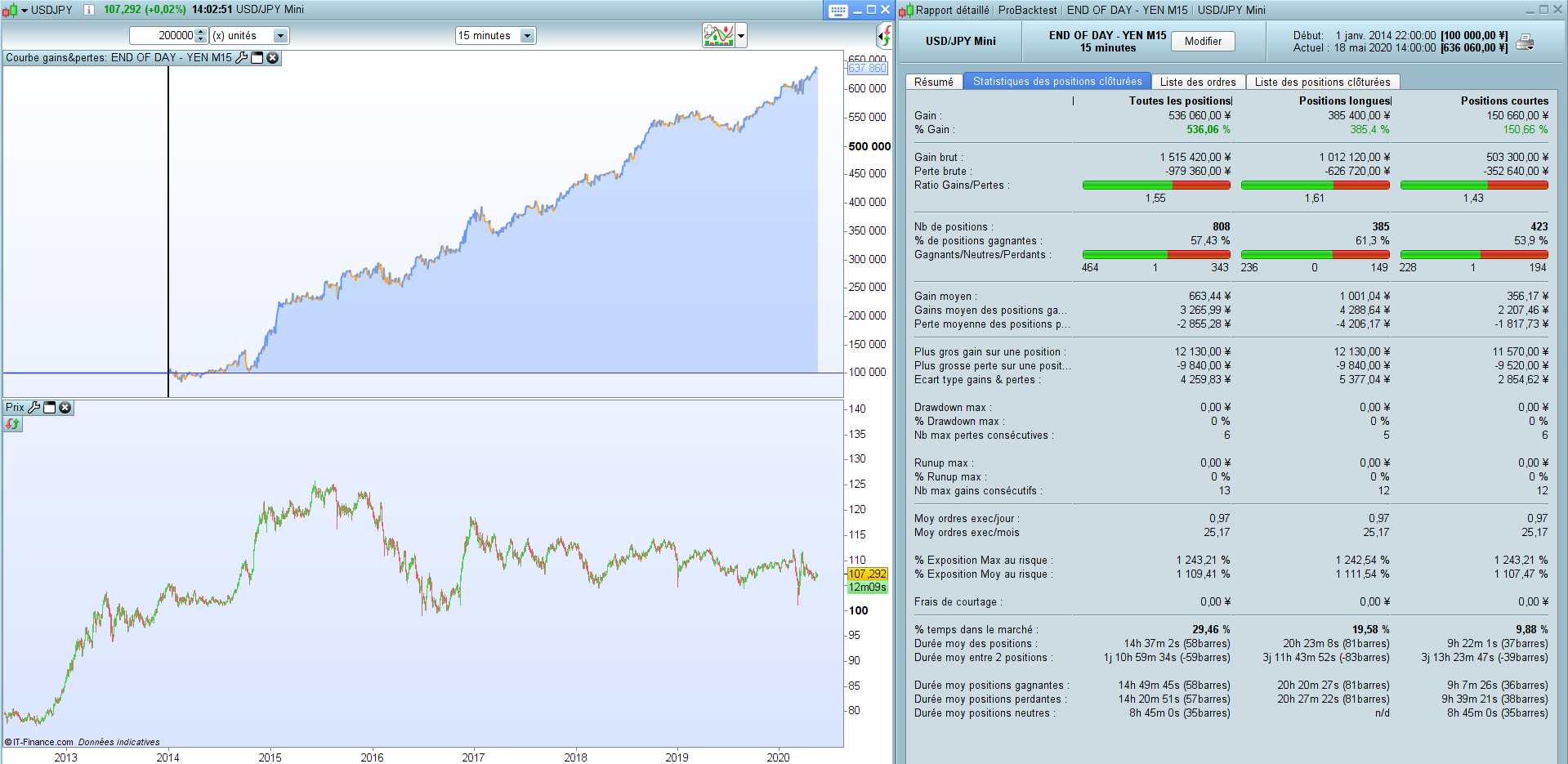

End Of Day - YEN M15

May 22, 2020, 10:37 AM

Strategies

39 Comments

{kind=link}

Dear All,

Here is a simple strategy, a slight improvement of my “End of Day USD/JPY“.

The timeframe is M15.

The strategy is so simple that it doesn’t need explanations (see in the code).

You can adapt the parameters, so that you can use it on USD/JPY (the best), AUD/JPY, EUR/JPY, GBP/JPY.

Regards,

// END OF DAY - YEN

// www.doctrading.fr

Defparam cumulateorders = false

// TAILLE DES POSITIONS

n = 1

// PARAMETRES

// high ratio = few positions

// AUD/JPY : ratio = 0.5 / SL = 0.8 / TP = 1.2 / Period = 12

// EUR/JPY : ratio = 0.6 / SL = 1 / TP = 0.8 / Period = 8

// GBP/JPY : ratio = 0.5 / SL = 0.6 / TP = 1 / Period = 8

// USD/JPY : ratio = 0.5 / SL = 1 / TP = 0.8 / Period = 12

ratio = 0.5

// HORAIRES

startTime = 210000

endTime = 231500

exitLongTime = 210000

exitShortTime = 80000

// STOP LOSS & TAKE PROFIT (%)

SL = 1

TP = 0.8

Period = 12

// BOUGIE REFERENCE à StartTime

if time = startTime THEN

amplitude = highest[Period](high) - lowest[Period](low)

ouverture = close

endif

// LONGS & SHORTS : every day except Fridays

// entre StartTime et EndTime

if time >= startTime and time <= endTime and dayOfWeek <> 5 then

buy n shares at ouverture - amplitude*ratio limit

sellshort n shares at ouverture + amplitude*ratio limit

endif

// Stop Loss & Take Profit

set stop %loss SL

set target %profit TP

// Exit Time

if time = exitLongTime then

sell at market

endif

if time = exitShortTime then

exitshort at market

endif

Download

Filename:

End-Of-Day-YEN-M15.itf

Downloads:

933

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...