FTSE MIB goes up at night strategy

April 19, 2017, 2:39 PM

Strategies

10 Comments

{kind=link}

Hello everyone.

I have coded for PRT this strategy that is based on the publicly available informations on Andrea Unger idea which exploits the fact that the FTSE Mib goes up mainly during night hours.

The idea is simple: buy the index at 5.30 PM and sell it at 9.30 AM.

In the code I added some filters that were discussed in a webinar by Andrea Unger, basically you buy the index at 5.30PM if the open price at 09.30 is < of the previous close and if the closing price at 5.30 pm is lower than the 2 previous daily lowest.

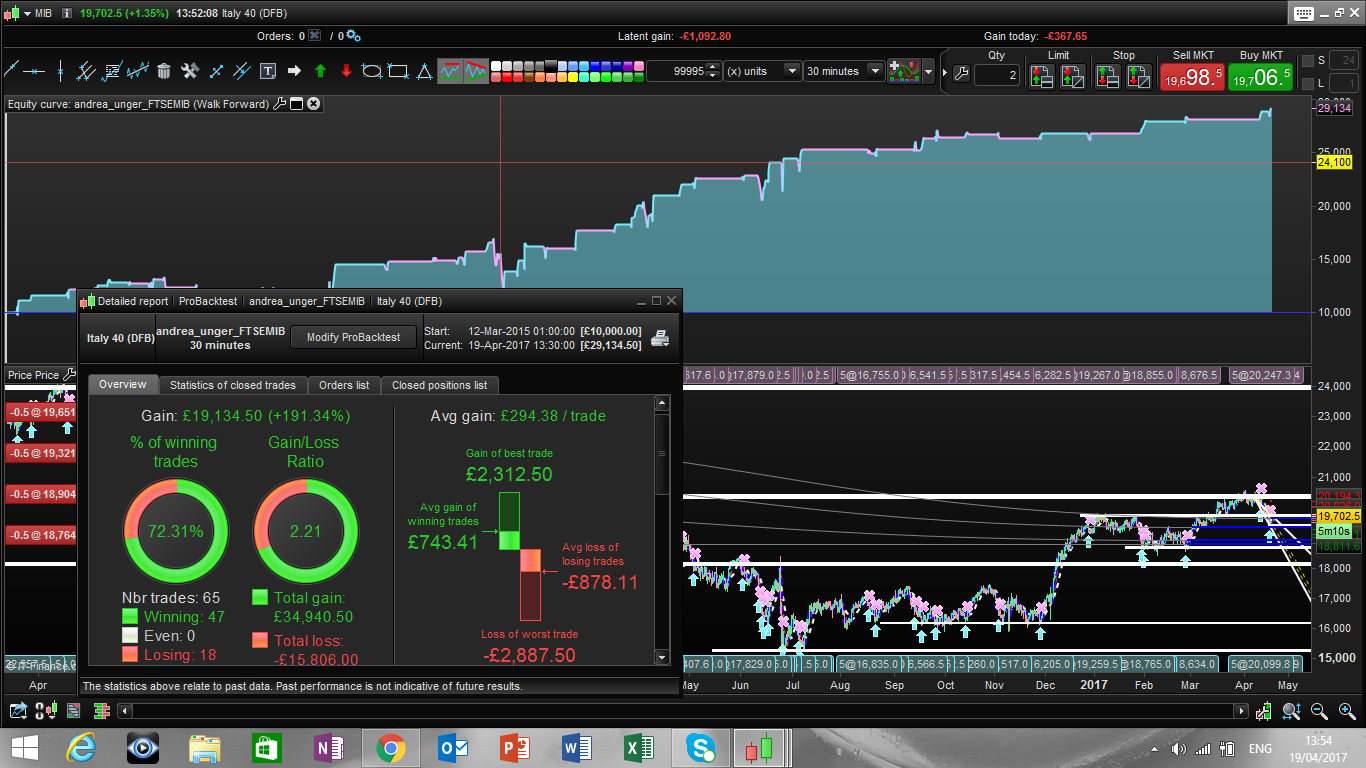

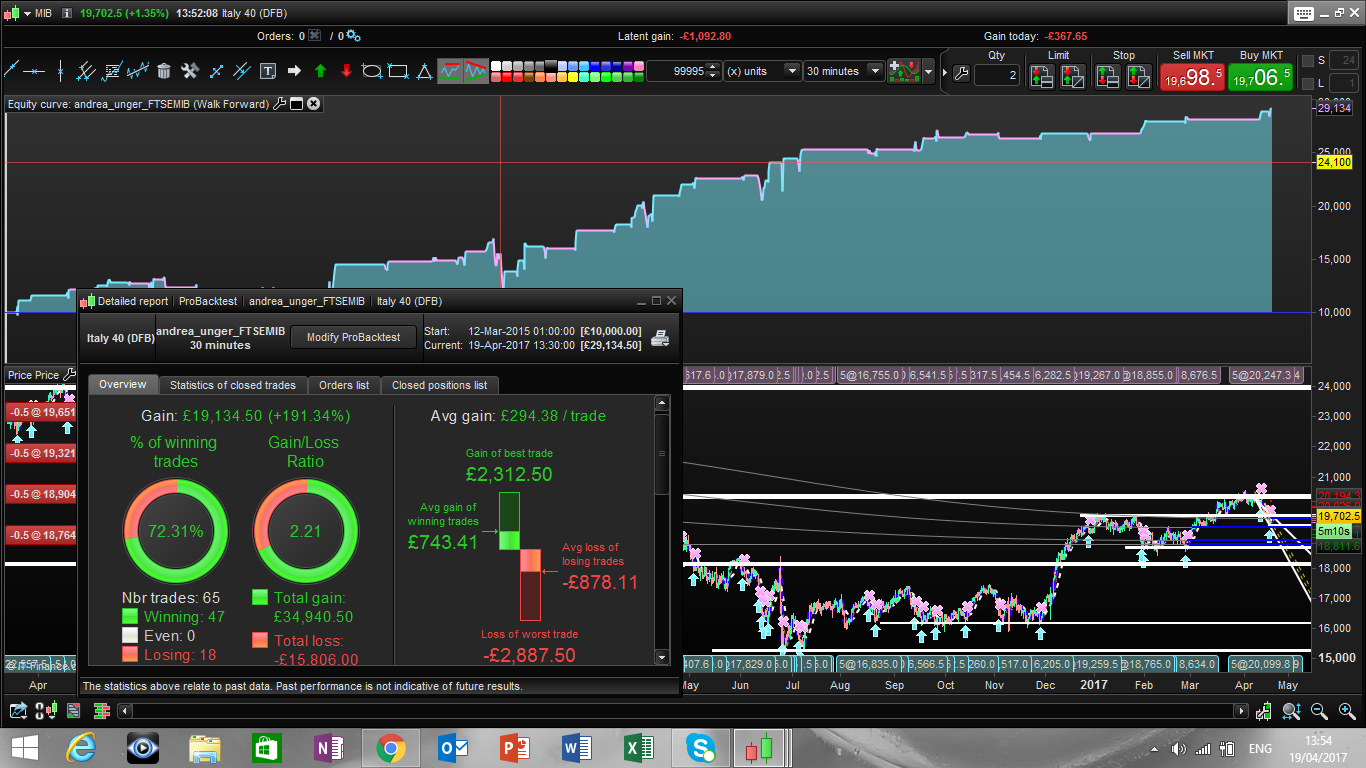

Results and code is attached.

Let me know what you think!

Many thanks

Francesco

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

timenter = time = 173000

timexit = time = 093000

timeobsopen = time = 093000

if timeobsopen Then

priceopen = open

endif

timeobsclose = time = 173000

if timeobsclose then

priceclose = open

endif

c1 = priceopen < DClose(1)

min1 = Dlow(1)

min2 = Dlow(2)

//min3 = Dlow(3)

result = Min(min1,min2)

//minimo = Min(result,min3)

c2 = (priceclose <= result)

size = 5

c3 = c1 and c2

IF c3 AND timenter THEN

BUY size PERPOINT AT MARKET

ENDIF

if timexit then

sell at market

endif

Download

{kind=link}

Filename:

AU_FTSEMIB.png

Downloads:

167

Download

Filename:

andrea_unger_FTSEMIB.itf

Downloads:

262

Master

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...