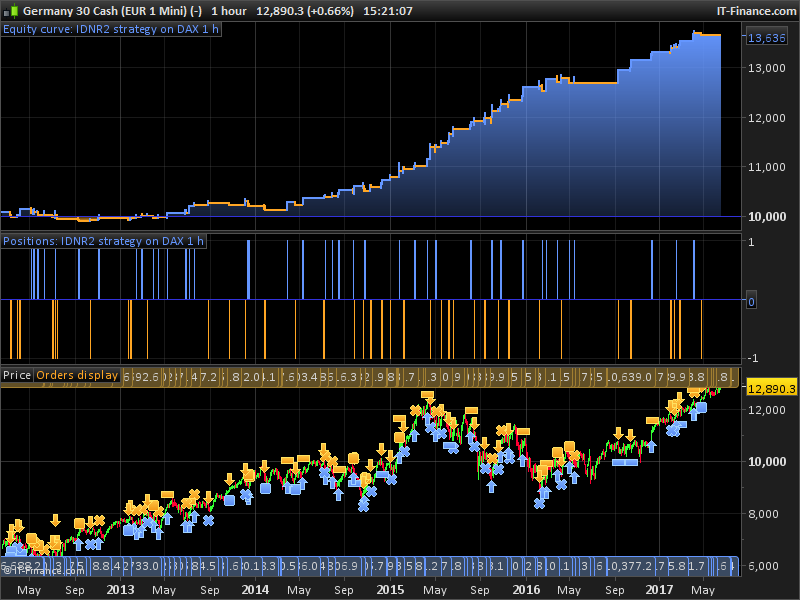

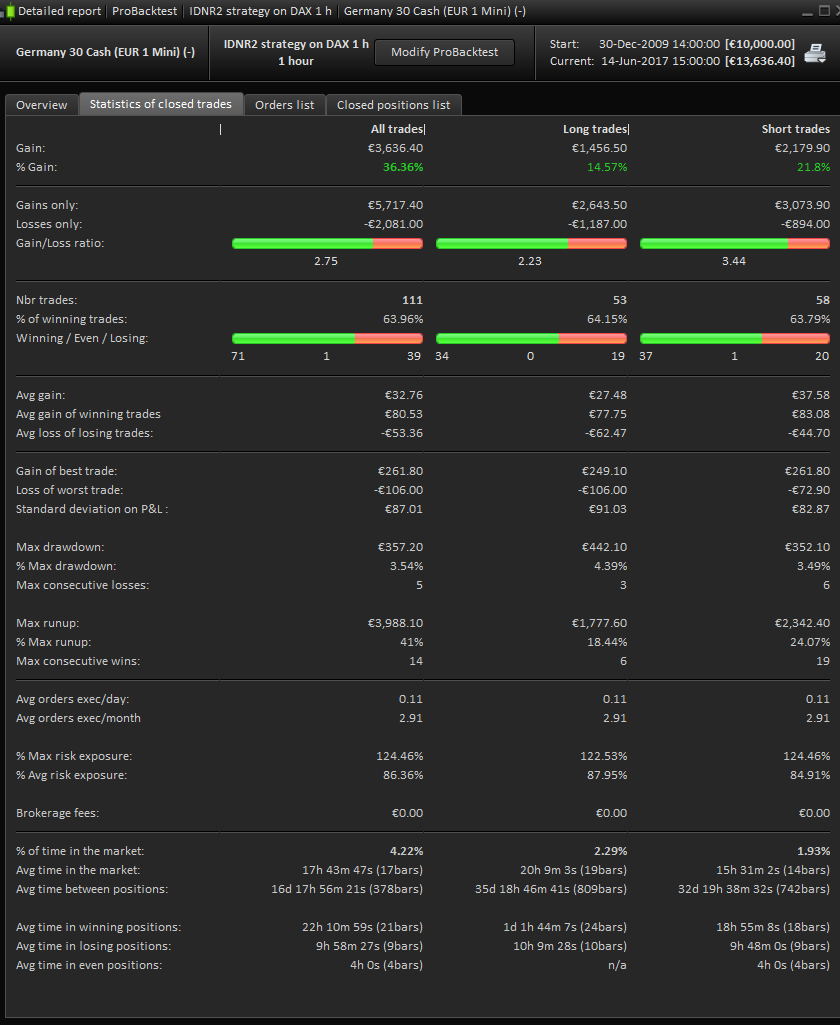

IDNR2 pattern strategy on DAX 1 h

June 14, 2017, 2:24 PM

Strategies

14 Comments

{kind=link}

I just wrote this strategy

It works very well on dax 1 h

It is based on the IDNR pattern with 2 periods instead of 4

As filter It uses the following: the squeze of the bollinger band (band width < lowest[period]) , adx > min and atr[1] > atr[period]

As trailing stop I used a code that I found in this library

It does not seem over fitted because changing parameters the result remains good and also It seems to work quite well on FTSE MIB 1 h too

However It seem to me that It makes too few trades on the historic that I have available to be sure of its reliability

NR10 = high < high[1] and low > low[1]and range < LOWEST[2](range)[1]

bbwdt =BollingerBandWidth[20](close) < lowest[17](BollingerBandWidth[20](close)[1])

// long entry

l1 = nr10

l1 = l1 and bbwdt

l1 = l1 and hour < 20

l1 = l1 and adx[10] > 17

l1 = l1 and AverageTrueRange[1](close) > AverageTrueRange[9](close)

IF not onmarket AND l1 THEN

BUY 1 CONTRACTS AT high+1.5 stop

ENDIF

// short entry

s1 = nr10

s1 = s1 and bbwdt

s1 = s1 and hour < 20

s1 = s1 and adx[10] > 17

s1 = s1 and AverageTrueRange[1](close) > AverageTrueRange[9](close)

IF not onmarket AND s1 then

SELLSHORT 1 CONTRACTS AT low -1.5 stop

ENDIF

// TRAILING STOP LOGIK

TGL =AverageTrueRange[14](close)*2.5

TGS=AverageTrueRange[14](close)*1.7

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

//stop and target

SET STOP PLOSS AverageTrueRange[14](close)*2.7

SET TARGET PPROFIT AverageTrueRange[14](close)*7.2

Download

{kind=link}

Filename:

IDNR-pattern-strategy-trading-result.png

Downloads:

289

Download

Filename:

IDNR2-strategy-on-DAX-1-h.itf

Downloads:

637

Veteran

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...