The "Keep It Simple and Stupid" strategy

{kind=link}

Hello everyone,

I wanted to test a strategy that I used manually in Day Trading on the DAX in graphs 5 minutes.

The problem is that it is not always easy to backtest a manual strategy, particularly it is difficult to determine the slope of the moving averages, the levels of supports / resistances, etc.

So I slightly adapted the parameters for automatic trading.

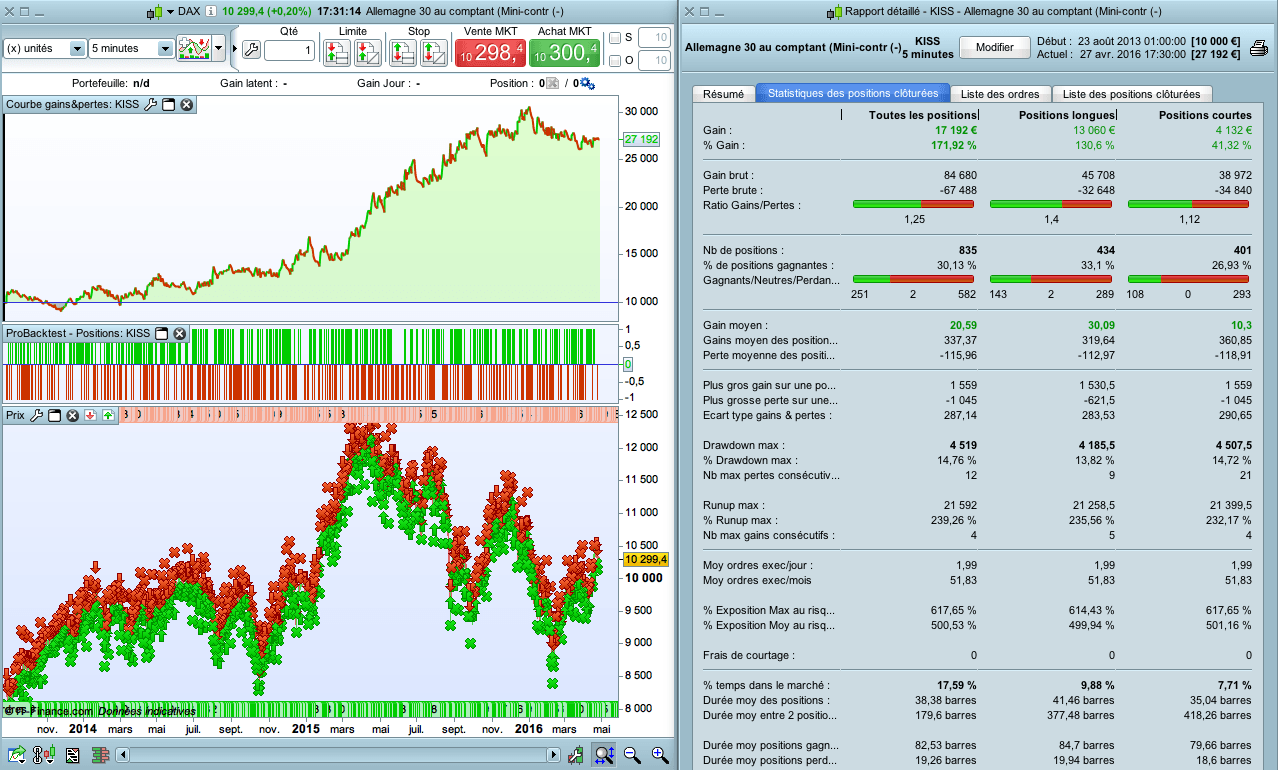

We have a profit factor of 1.25 (spread included in the backtest) ; in manual trading I am rather at a profit factor of 1.5 (but exit rules are slightly different, on a trailing stop that is difficult to adapt) . I’m quite happy with my backtest that looks pretty close to reality. The strategy is very simple, it is the “KISS”, Keep It Simple and Stupid strategy. It uses only three moving averages, we trade with the trend.

Note that the test is positive in M5 timeframe (but I can only test it on 2,5 years), it is much worse on the upper timeframes.

Defparam cumulateorders = false

Ctime = time > 080000 and time < 180000

MM200 = average[200](close)

MM180 = average[180](close)

MM20 = average[20](close)

// ACHAT

ca1 = MM20 > MM180 and MM180 > MM200

ca2 = MM200 > MM200[1] and MM180 > MM180[1] and MM20 > MM20[1]

ca3 = close crosses over MM20

ca4 = close > open and close > close[2]

ca5 = ADX[14] > 12

IF Ctime and ca1 and ca2 and ca3 and ca4 and ca5 THEN

buy at market

ENDIF

Sell at MM180 stop

// VENTE

cv1 = MM20 < MM180 and MM180 < MM200

cv2 = MM200 < MM200[1] and MM180 < MM180[1] and MM20 < MM20[1]

cv3 = close crosses under MM20

cv4 = close < open and close < close[2]

cv5 = ADX[14] > 12

IF Ctime and cv1 and cv2 and cv3 and cv4 and cv5 THEN

sellshort at market

ENDIF

Exitshort at MM180 stop

// Clôture des positions le soir

IF time = 200000 THEN

sell at market

exitshort at market

ENDIF