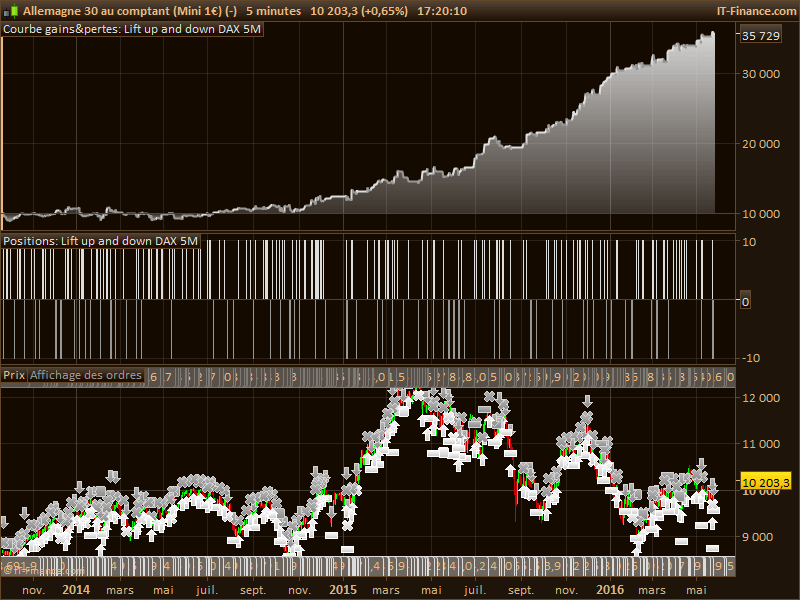

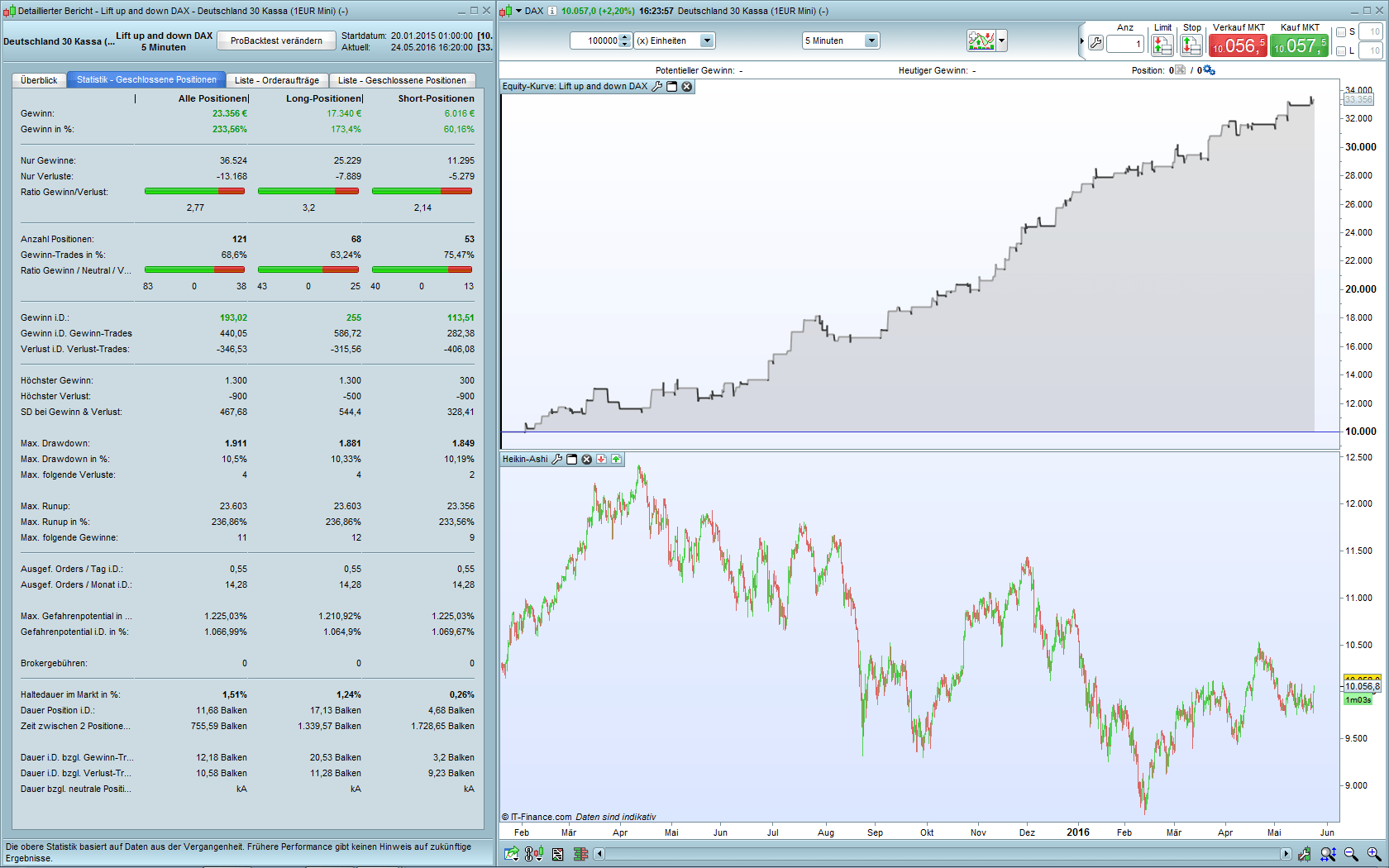

Lift up and down DAX 5M

May 25, 2016, 4:19 PM

Strategies

35 Comments

{kind=link}

Hi guys,

I want to share one of my DAX trading ideas based on cross over/under yesterdays high and low in combination with volatile intraday trading windows and certain week days. The approach is very simple works without indicators but seems to be very robust and reliable.

I have inserted Adolfo’s litle beauty concerning money management but fixed position size is possible as well (simply remove the comment).

Comments and improvements are welcome.

have fun

Reiner

// Lift up and down DAX 5M

// Code-Parameter

DEFPARAM FlatAfter = 113000

// trading window

ONCE BuyTime = 84500

ONCE SellTime = 113000

// money management

// variable position size - thanks Adolfo :-)

ONCE Capital = 10000

ONCE Risk = 0.01

ONCE StopLoss = 10

ONCE equity = Capital + StrategyProfit

ONCE maxrisk = round(equity*Risk)

ONCE PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

// fixed position size

// ONCE PositionSize = 10

// manage number of trades

IF Time = BuyTime THEN

LongTradeCounter = 0

ShortTradeCounter = 0

ENDIF

// long on Monday until Thursday with filter close is above MA(14) and max 2 trades per day

IF Not LongOnMarket AND Time >= BuyTime AND close CROSSES OVER DHigh(1) AND close > Average[14](close) AND LongTradeCounter < 2 AND CurrentDayOfWeek <> 5 THEN

BUY PositionSize CONTRACT AT MARKET

LongTradeCounter = LongTradeCounter + 1

sl = 50

tp = 130

ENDIF

// short on Monday and Tuesday with filter close is under MA(9) and max 2 trades per day

IF Not ShortOnMarket AND Time >= BuyTime AND close CROSSES UNDER DLow(1) AND close < Average[9](close) AND ShortTradeCounter < 2 AND CurrentDayOfWeek < 3 THEN

SELLSHORT PositionSize CONTRACT AT MARKET

ShortTradeCounter = ShortTradeCounter + 1

sl = 90

tp = 30

ENDIF

// exit

IF LongOnMarket AND Time = SellTime THEN

SELL AT MARKET

ENDIF

IF ShortOnMarket AND Time = SellTime THEN

EXITSHORT AT MARKET

ENDIF

// stop and target

SET STOP pLOSS sl

SET TARGET pPROFIT tp

Download

Filename:

Lift-up-and-down-DAX-5M.itf

Downloads:

639

Download

{kind=link}

Filename:

lift-up-and-down-dax-1464100457l84cp.png

Downloads:

220

Veteran

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...