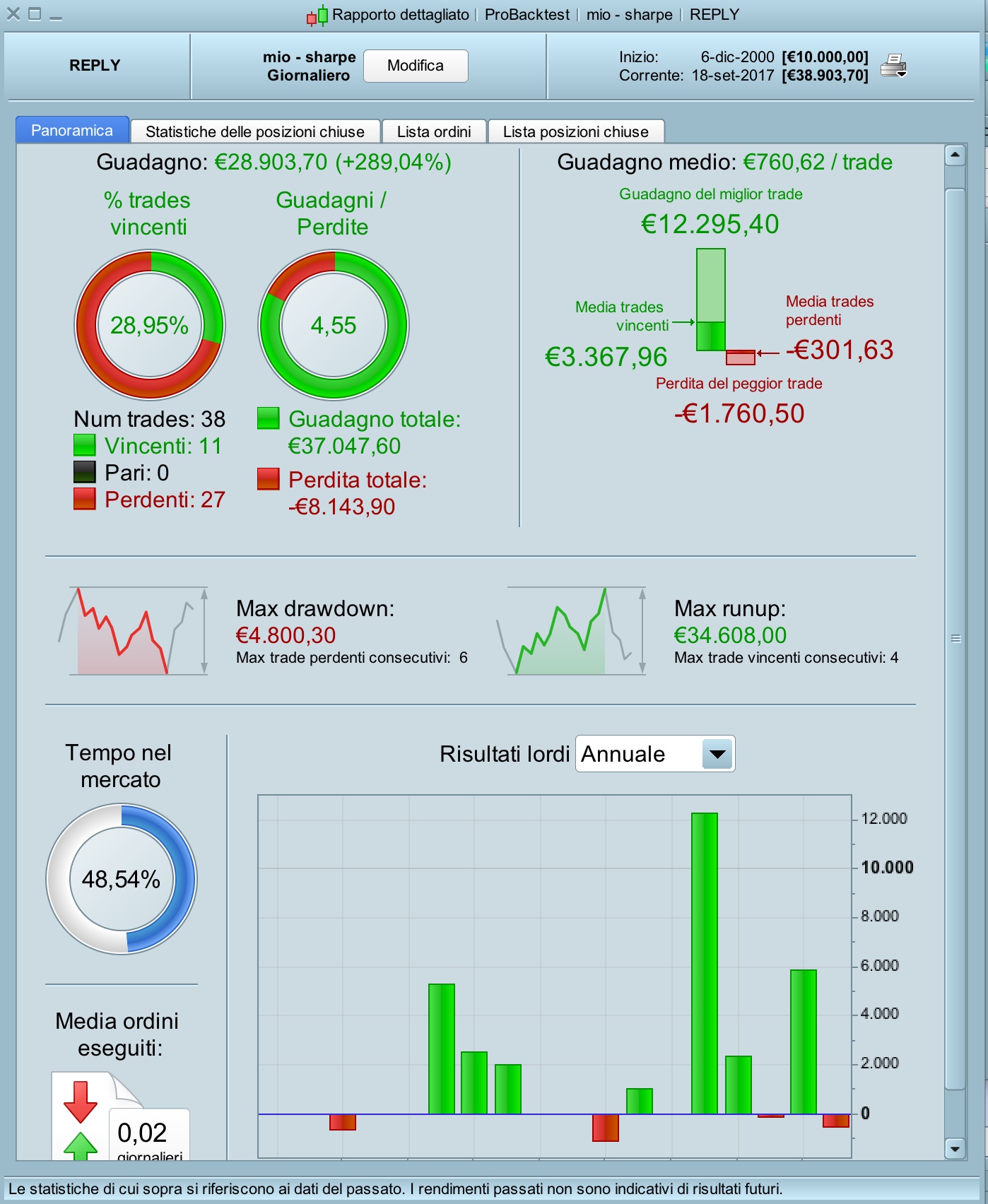

Modified SHARPE index portfolio strategy

September 19, 2017, 7:22 AM

Strategies

12 Comments

{kind=link}

This simple strategy is a LONG only. It enters the market when the modified SHARPE index crosses definitely above 1 (I used 1 to cut false signals but 0 could work just fine) and exits in one of the following cases:

1. price crosses below SMA256

2. when, at a trimester check, SHARPE index is not anymore above 1

3. after one year of investment

It works best with 20-30 stocks portfolios, so this strategy should be launched on a selection of stocks.

Blue skies!!

// Definizione dei parametri del codice

DEFPARAM CumulateOrders = False // Posizioni cumulate disattivate

//n=1

//p=254

// Condizioni per entrare su posizioni long

idx, ignored = CALL "Mio - indice di Sharpe PRT"[254]

sma254=average[254](close)

lim=n*5*1.1

c1=summation[5](idx)>lim

c11=close>sma254

IF c1 and c11 THEN

BUY 10000 CASH AT market

ENDIF

c3=longonmarket and (barindex-tradeindex)>p

c4=close crosses under sma254

c5=longonmarket and (barindex-tradeindex)>66 and (barindex-tradeindex)<71

c6=longonmarket and (barindex-tradeindex)>130 and (barindex-tradeindex)<135

c7=longonmarket and (barindex-tradeindex)>196 and (barindex-tradeindex)<201

IF c3 then

SELL AT market

ENDIF

if c4 then

sell at market

//sell at low*0.99 stop

endif

if (c5 or c6 or c7) and (summation[5](idx)<lim) then

sell at market

endif

Download

Filename:

mio-sharpe-PRT-AT.itf

Downloads:

327

Master

Code artist, my biography is a blank page waiting to be scripted. Imagine a bio so awesome it hasn't been coded yet.

Author’s Profile

Loading...