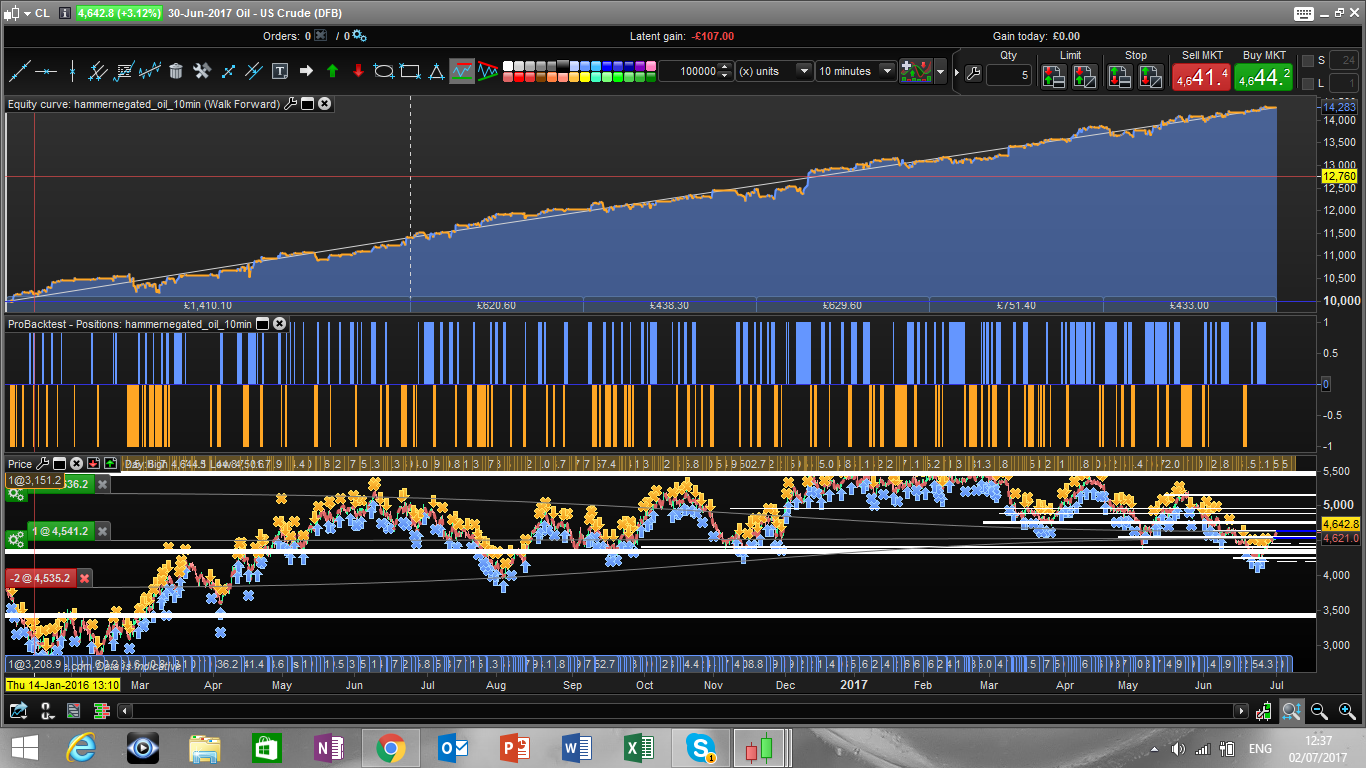

Oil 10min "hammernegated" pattern strategy

{kind=link}

Dear all,

I found this nice strategy by playing with candlestickpatterns with 2 candles.

Basically I considered the “hammer negated” pattern, where you have first an hammer candle (body on the upper or lower 25% of the candle) and then a candle which negate the hammer so in case we have a bullish hammer, then we have a candle whose body is within yesterday candle shadow. I hope it is clear as I have no idea how to draw candles on the laptop.

I added then a few moving average that identifies momentum, and opted for trailing stops.

The only thing I have optimized here are trailing stops level. All the moving average period, the parameter that defines the candlestick pattern are not optimized, no target profit either. Thats why WF results are pretty impressive.

Only downside as usual is that I dont have more than 100K history.

Enjoy

Francesco

defparam cumulateorders = false

av1 = average[5](close)

av2 = average[10](close)

av3 = average[50](close)

x = 0.5

bull = close> av1 and close >av2 and close > av3

bear = close <av1 and close <av2 and close <av3

//n= 1

hammerup = min(open[1],close[1])>high[1]-(high[1]-low[1])/3 //and timeok

hammerupnegated= max(open,close)<min(open[1],close[1]) and abs(open-close)/(high-low)>x

cs = hammerup and hammerupnegated and bear

hammerdown = max(open[1],close[1])<low[1]+(high[1]-low[1])/3 //and timeok

hammerdownnegated = min(open,close)>max(open[1],close[1]) and abs(open-close)/(high-low)>x

cl = hammerdown and hammerdownnegated and bull

if cs then

sellshort 1 contract at market

endif

if cl then

buy 1 contract at market

endif

//TRAILING STOP

TGL =18

TGS= 24

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

//set target pprofit n*averagetruerange[14]

//set stop ploss m*averagetruerange[14]

{kind=link}

{kind=link}