Oil 15 minutes meanreverting strategy

June 28, 2017, 2:28 PM

Strategies

24 Comments

{kind=link}

Hello,

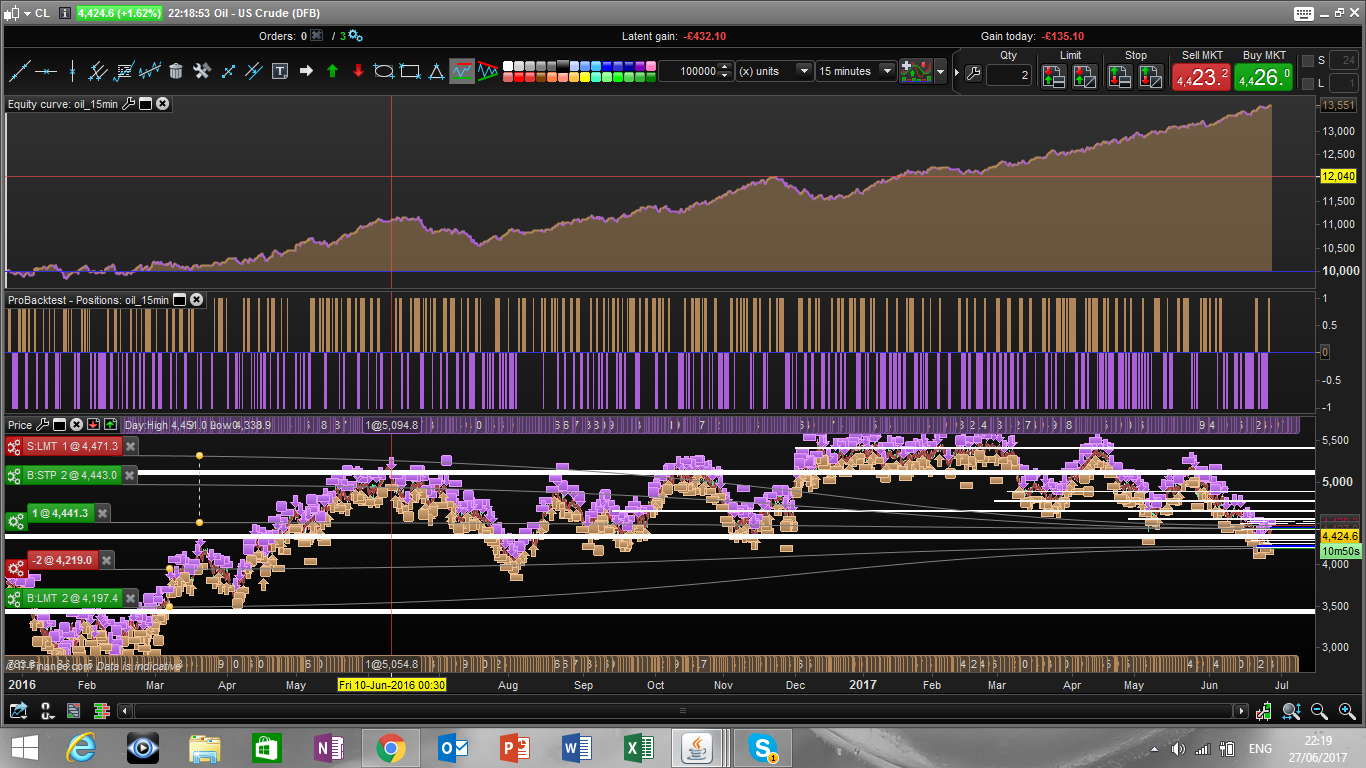

I found this nice and simple strategy playing with the “average fullness of last 5 candles” . I added a simple moving average oscillator, with 5 and 50 period and I considered mean reverting long/short condition by setting a threshold to the “average fullnes”

The strategy is really minimally optimized, I only optimized the threshold and the profit and stop target.

Results of backtest and WF are attached

Regards

Francesco

//crude oil 15 min strategy

DEFPARAM cumulateOrders = False // Cumulating positions deactivated

///parameter definition

period = 5

fastav = average[5](close)

slowav = average[50](close)

maoscillator = fastav-slowav

fullness = (Dclose(0)-Dopen(0))/abs(Dhigh(0)-Dlow(0))

avfullness = summation[period](fullness)/period

pr = 50

pl = 40

avfullnessthreshold = 0.2

cl = maoscillator > 0

cl = cl and avfullness < -avfullnessthreshold

// Conditions to enter long positions

cs = maoscillator<0

cs = cs and avfullness > avfullnessthreshold

IF cl THEN

BUY 1 PERPOINT AT MARKET

ENDIF

if cs then

sellshort 1 perpoint at market

endif

set target pprofit pr

set stop ploss pl{kind=link}

Master

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...