Open Range Breakout DAX 5/15M

June 10, 2016, 4:40 PM

Strategies

27 Comments

{kind=link}

Hi guys,

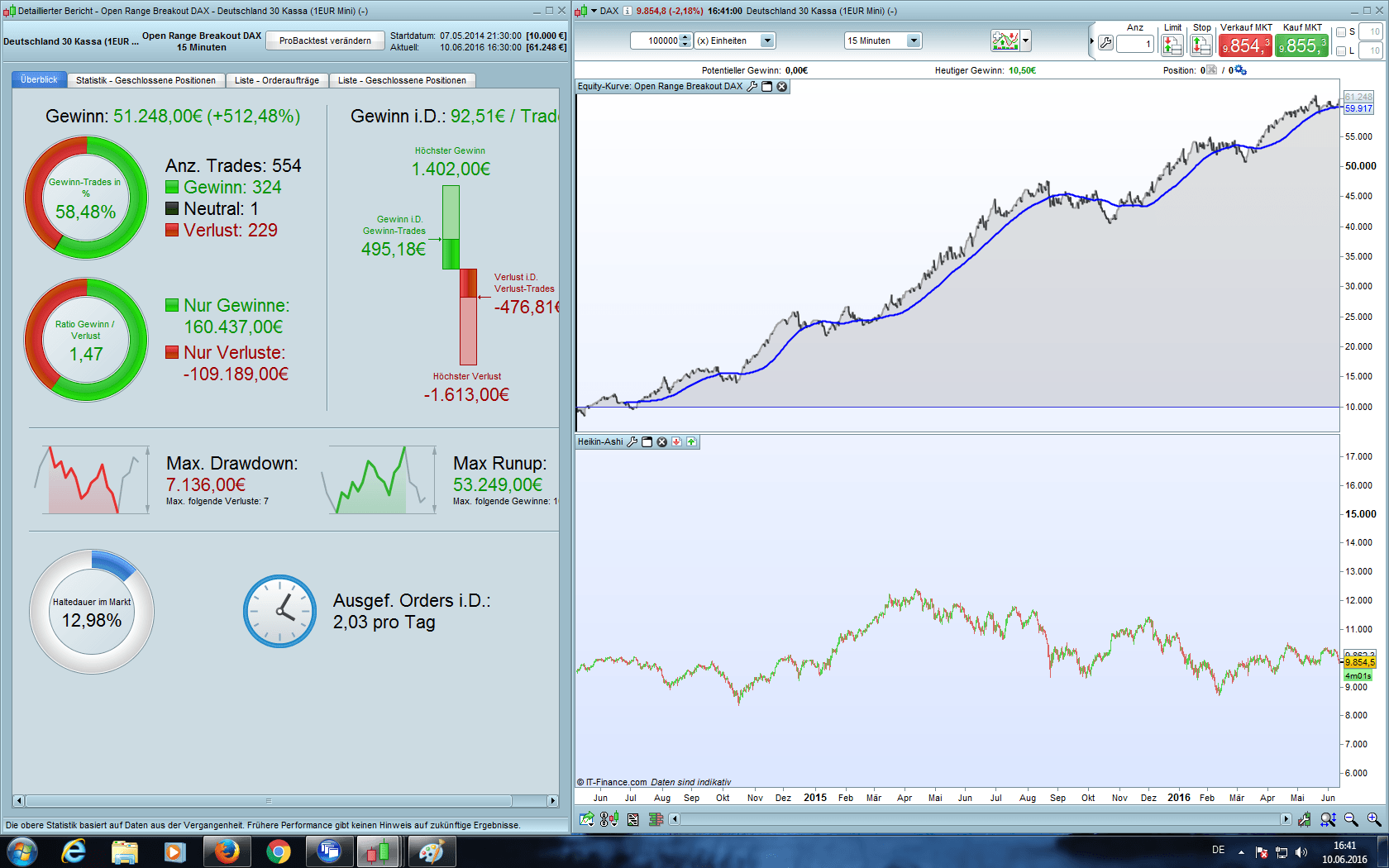

Open range breakout systems are very popular. They are simple and reliable with volatile instruments like the DAX. I trade the ORB together with the equity curve because as all breakout systems they could have some ugly drawdown phases. These concept is very easy and is described perfectly here in the Blog. Add to the equity curve a simple moving average and trade only if the curve is above the MA could help to avoid ugly losses.

I want to share an easy ORB strategy works profitable in M5 and M15 – this is not a big thing but maybe helpful for some PRT beginners.

have fun

Reiner

// Open Range Breakout DAX 5/15M

// code-parameter

DEFPARAM FlatAfter = 173000

// window high/low calculation

ONCE StartTime = 90000

ONCE EndTime = 93000

// trading window

ONCE BuyTime = 93000

ONCE SellTime = 173000

// money management

ONCE Capital = 10000

ONCE Risk = 0.01

ONCE StopLoss = 10

ONCE equity = Capital + StrategyProfit

ONCE maxrisk = round(equity*Risk)

ONCE PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

// fixed position size

//ONCE PositionSize = 10

//signal line

signal = Tema[5](close)

// calculate high/low and sl/tp

IF Time >= StartTime AND Time <= EndTime THEN

IF TIME = StartTime THEN

DailyHigh = High

DailyLow = Low

ENDIF

IF High > DailyHigh THEN

DailyHigh = High

ENDIF

IF Low < DailyLow THEN

DailyLow = Low

ENDIF

sl = DailyHigh - DailyLow

tp = sl

TradeCounterLong = 0

TradeCounterShort = 0

ENDIF

// position management

IF Time >= BuyTime AND Time <= SellTime THEN

// Long

IF Not LONGONMARKET AND signal CROSSES OVER DailyHigh AND TradeCounterLong = 0 THEN

// long

IF (Time >= 93000 AND Time <= 113000) OR (Time >= 130000 AND Time <= 171500) THEN // no trading during lunch

BUY PositionSize CONTRACT AT MARKET

TradeCounterLong = TradeCounterLong + 1

ENDIF

ENDIF

// short

IF Not SHORTONMARKET AND signal CROSSES UNDER DailyLow AND close < DClose(1) AND TradeCounterShort = 0 THEN

IF Time >= 93000 AND Time <= 150000 THEN // short breakouts after 1500 are not profitable

SELLSHORT PositionSize CONTRACT AT MARKET

TradeCounterShort = TradeCounterShort + 1

ENDIF

ENDIF

// close positions

IF Time = SellTime THEN

IF LONGONMARKET THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND Time = SellTime THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

// stops and targets

SET STOP LOSS sl

SET TARGET PROFIT tp

ENDIF

Download

Filename:

Open-Range-Breakout-DAX-5-15M.itf

Downloads:

963

Veteran

Code artist, my biography is a blank page waiting to be scripted. Imagine a bio so awesome it hasn't been coded yet.

Author’s Profile

Loading...