QU Trading Strategy DAX Indices CFD

November 7, 2016, 10:38 AM

Strategies

48 Comments

{kind=link}

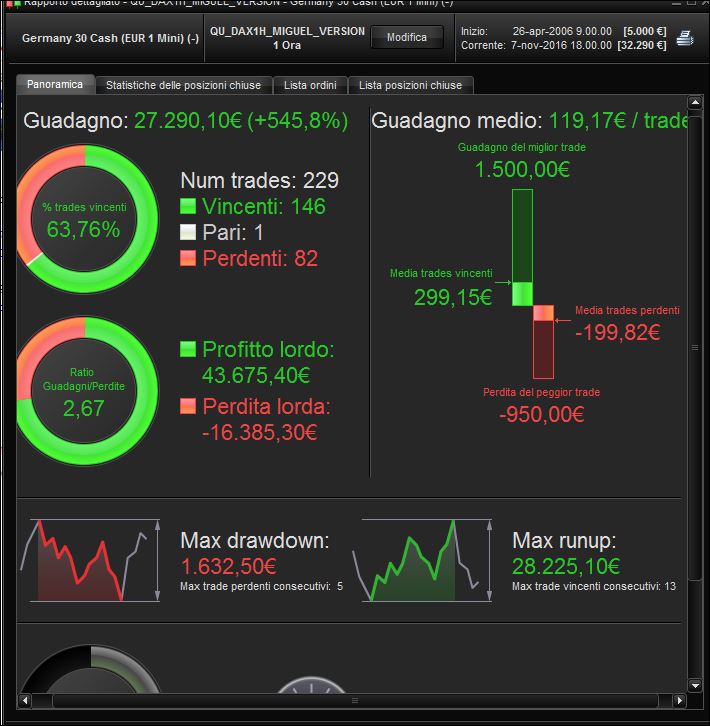

This is a Multiday Strategy on DAX cfd of Ig Market- Time Frame 1 Hour

Signals are taken from QQE indicator and Universal indicator participates as filter.

The Seasonal optimization is Reiner’s Idea, that work well which we know.

The position are followed by a trailing stop.

Test result are made with DAX 1 € mini Spread 2

Time Frame 1 Hour

Since 26.04.2006 to 01.11.2016

The strategy needs also 3 technical indicators that are also attached at the bottom of the post. These technical indicators are original ones found on the site and modified for the strategy.

// Definizione dei parametri del codice

DEFPARAM CumulateOrders = FALSE // Posizioni cumulate disattivate

// define position and money management parameter

ONCE positionSize = 1

// define saisonal position multiplier >0 - long

ONCE Januaryl = 1

ONCE Februaryl = 1

ONCE Marchl = 2

ONCE Aprill = 1

ONCE Mayl = 1

ONCE Junel = 3

ONCE Julyl = 2

ONCE Augustl = 1

ONCE Septemberl = 1

ONCE Octoberl = 3

ONCE Novemberl =2

ONCE Decemberl = 2

// saisonal pattern long position

IF CurrentMonth = 1 THEN

saisonalPatternMultiplierl = Januaryl

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplierl = Februaryl

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplierl = Marchl

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplierl = Aprill

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplierl = Mayl

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplierl = Junel

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplierl = Julyl

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplierl = Augustl

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplierl = Septemberl

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplierl = Octoberl

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplierl = Novemberl

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplierl = Decemberl

ENDIF

// define saisonal position multiplier >0 short

ONCE Januarys = 2

ONCE Februarys = 1

ONCE Marchs = 1

ONCE Aprils = 1

ONCE Mays = 3

ONCE Junes = 2

ONCE Julys = 1

ONCE Augusts = 1

ONCE Septembers = 3

ONCE Octobers = 1

ONCE Novembers = 1

ONCE Decembers = 1

// saisonal pattern short position

IF CurrentMonth = 1 THEN

saisonalPatternMultipliers = Januarys

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultipliers = Februarys

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultipliers = Marchs

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultipliers = Aprils

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultipliers = Mays

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultipliers = Junes

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultipliers = Julys

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultipliers = Augusts

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultipliers = Septembers

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultipliers = Octobers

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultipliers = Novembers

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultipliers = Decembers

ENDIF

// Condizioni per entrare su posizioni long

ignored, indicator1, ignored = CALL "QQE_QUDAX1HBUY"

ignored, indicator3, ignored = CALL "QQE_QUDAX1HSELL"

indicator2, ignored = CALL "UNIV_QUDAX1H_LOW"

c1 = (indicator1 CROSSES OVER 50)

c2 = (indicator2 <= 0)

c3=(indicator1>68)

c4=(indicator1<34)

// Condizioni per entrare su posizioni short

c5 = (indicator3 CROSSES UNDER 50)

c6 = (indicator2 >= 0)

C7 = (indicator3<35)

C8=(indicator3>56)

IF c1 AND c2 THEN

IF saisonalPatternMultiplierl > 0 THEN // check saisonal booster setup and max position size

BUY positionSize * saisonalPatternMultiplierl CONTRACT AT MARKET

ENDIF

ENDIF

IF C3 OR C4 THEN

SELL AT MARKET

ELSIF c5 AND c6 THEN

IF saisonalPatternMultipliers > 0 THEN // check saisonal booster setup and max position size

SELLSHORT positionSize * saisonalPatternMultipliers CONTRACT AT MARKET

ENDIF

ENDIF

IF C7 OR C8 THEN

EXITSHORT AT MARKET

ENDIF

// TRAILING STOP LOGIK

TGL =131

TGS= 100

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ONCE maxCandlesShortWithoutProfit =68// limit short loss latest after 85 candles

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ms = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF SHORTONMARKET AND ms THEN

EXITSHORT AT MARKET

ENDIF

set stop Ploss 500

set target Pprofit 500

Download

{kind=link}

Filename:

QU_DAX1H_MIGUEL.jpg

Downloads:

762

Download

Filename:

UNIV_QUDAX1H_LOW.itf

Downloads:

894

Download

Filename:

QU-DAX-1-H-turbo-V1.itf

Downloads:

1012

Download

Filename:

QQE_QUDAX1HSELL.itf

Downloads:

913

Download

Filename:

QQE_QUDAX1HBUY.itf

Downloads:

1048

Master

My name is Alessandro, i'm a trader since 2006

You can find me on my website: <a href="http://www.automatictrading.it/" rel="dofollow">www.automatictrading.it</a>

<strong>(trading programming services Italy)</strong>

Italy

Author’s Profile

Loading...