Renko automated trading system

December 14, 2016, 8:38 AM

Strategies

11 Comments

{kind=link}

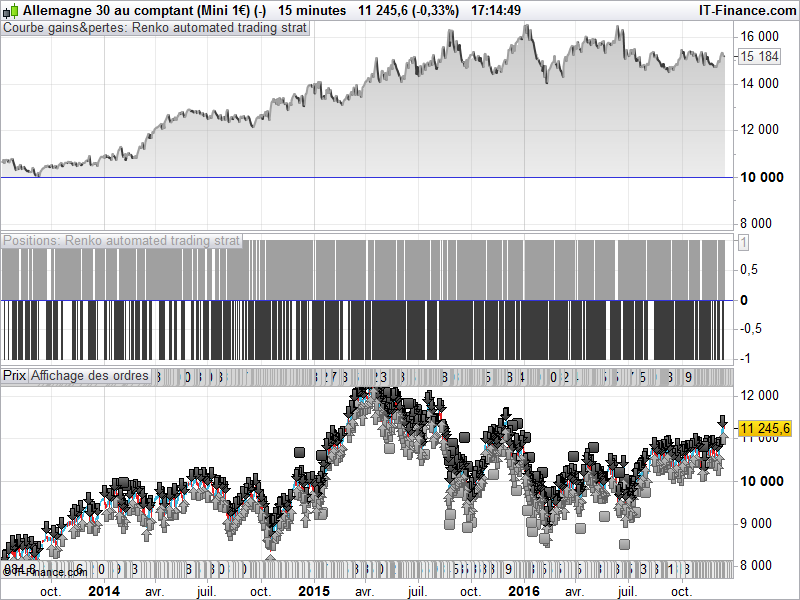

Renko trading system (very general, applicable e.g. for DAX 15 min chart) goes long when at least 2 upbricks appear after a downtrend of 2 bricks or more goes short when 2 downbricks appear after an uptrend of 2 bricks or more.

“bricksize” is the length of a Renko brick in points and be modified (line 3).

“BIfirst” is the first bar in the chart that defines the position of all other Renko bricks. Can be left out, but can makes a big difference.

defparam cumulateorders = false

bricksize = 22

BIfirst = 1

n = 1

If barindex >= BIfirst then

ONCE upbrick = close

ONCE downbrick = close - bricksize

buysignal = 0

shortsignal = 0

IF close >= upbrick + bricksize THEN

newbricksup = (round(((close - upbrick) / bricksize) - 0.5))

diffup = newbricksup * bricksize

downbrick = downbrick + diffup

upbrick = upbrick + diffup

totalbricksup = totalbricksup + newbricksup

totalbricksdown = 0

If (totalbricksup[1] = 0 OR totalbricksup[1] = 1) AND totalbricksup >= 2 then

buysignal = 1

endif

ELSIF close <= downbrick - bricksize THEN

newbricksdown = (round(((downbrick - close) / bricksize) - 0.5))

diffdown = newbricksdown * bricksize

upbrick = upbrick - diffdown

downbrick = downbrick - diffdown

totalbricksdown = totalbricksdown + newbricksdown

totalbricksup = 0

If (totalbricksdown[1] = 0 OR totalbricksdown[1] = 1) AND totalbricksdown >= 2 then

shortsignal = 1

endif

ENDIF

endif

If buysignal = 1 then

buy n contracts at market

endif

If shortsignal = 1 then

sellshort n contracts at market

endif

set stop ploss 120

Download

Filename:

Renko-automated-trading-strat.itf

Downloads:

404

Veteran

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...