The "RSI 2P" from Larry Connors

July 19, 2016, 1:50 PM

Strategies

4 Comments

{kind=link}

Hi all,

Here is another strategy from Larry Connors, that I did coded for us.

It was designed for M30 timeframe, on various indices / forex / raw materials. But my tests show that is is most of time unprofitable.

I also find that some values are profitable with it, on higher timeframes.

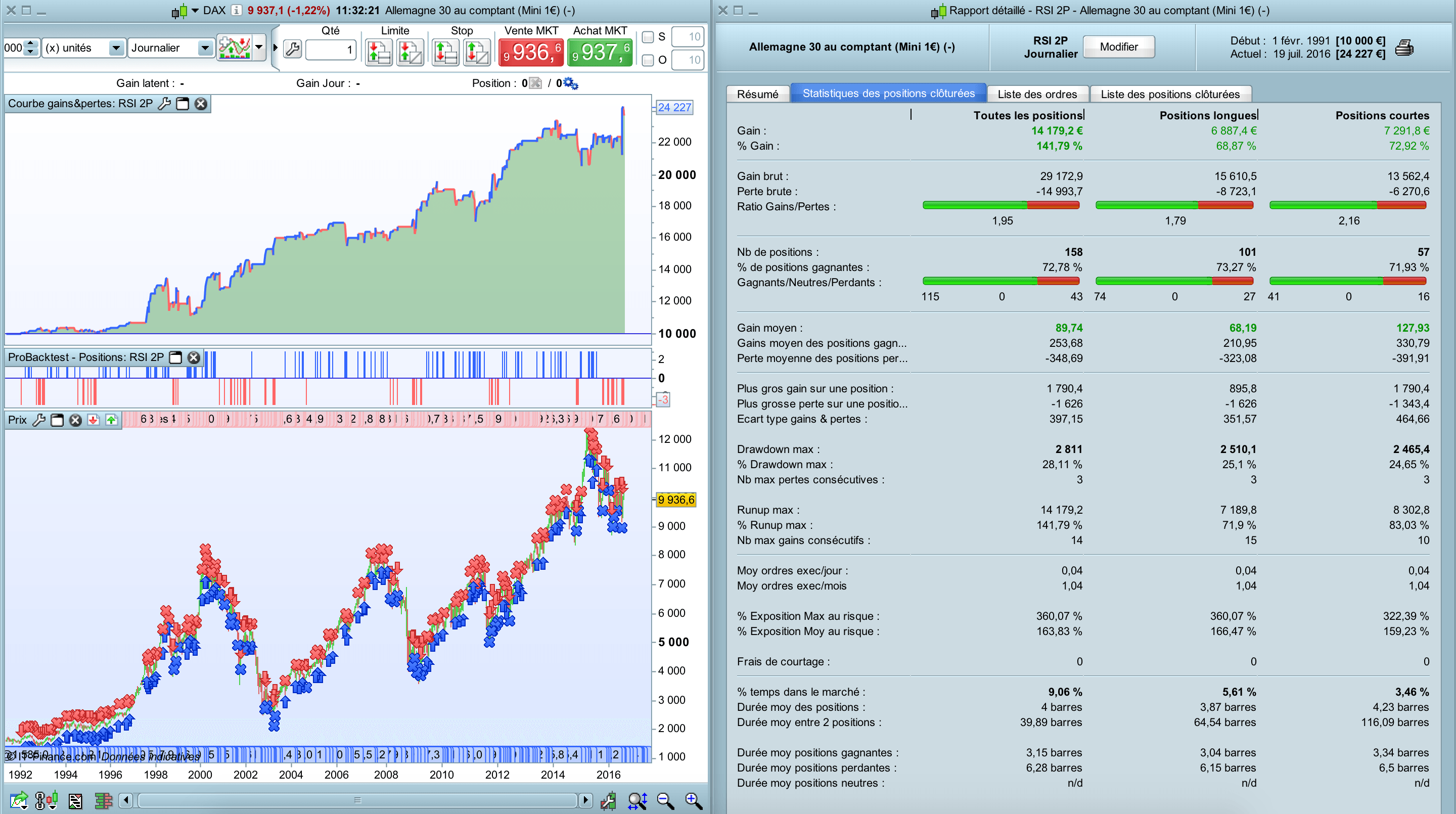

For example as show in the backtest picture (CFD Germany 30, 1€ per point, spread 1 point, daily timeframe).

RULES aver very simple :

BUY if :

- close > SMA200

- RSI2 < 5

CLOSE BUY if :

- close > SMA5

That’s all.

Opposite rules for SELL positions.

Larry Connors didn’t use stop loss ; but you can set one.

// RSI 2P

// de Larry Connors

// www.doctrading.fr

DEFPARAM CUMULATEORDERS = false

n = 3 // mettre ce que vous voulez

// INDICATEURS

MM200 = average[200](close)

MM5 = average[5](close)

RSI2 = RSI[2](close)

// ACHAT

ca1 = close > MM200

ca2 = RSI2 < 5

IF ca1 and ca2 then

BUY n shares at market

ENDIF

// SORTIE ACHAT

IF close > MM5 THEN

sell at market

ENDIF

// VENTE

cv1 = close < MM200

cv2 = RSI2 > 95

IF cv1 and cv2 THEN

SELLSHORT n shares at market

ENDIF

// SORTIE VENTE

IF close < MM5 THEN

exitshort at market

ENDIF

Download

Filename:

RSI-2P.itf

Downloads:

343

Master

Hello, I'm Marc.

Nice to meet you.

Author’s Profile

Loading...