Sell in May, Buy in October : it works!

{kind=link}

Hi all !

We will check the well-known adage traded “Sell in May , Buy in October .”

So I decided to code the strategy and check on various indices.

You will be surprised at the results!

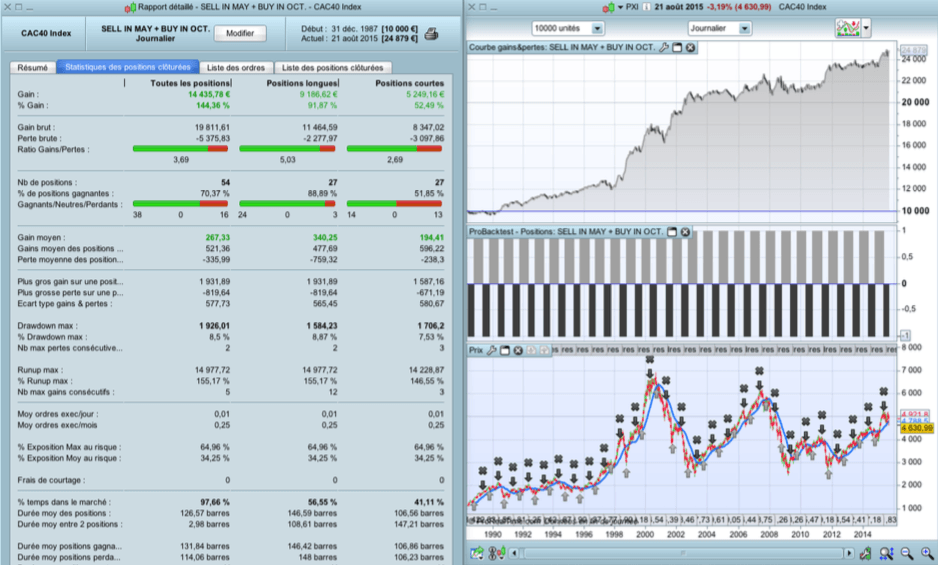

For example, the CAC40 : from 31/12/1987 to 21/08/2015 (my backtest data when I had realized the test) we have 70% winning trades, with higher earnings than average losses and a profit factor of 3.69.

And if you separate long and short positions, positions “long” only give 88.89 % success rate, with a profit factor of 5.03 !

You can check the strategy is clearly winning over as many indexes : DAX30, FTSE, S&P500, NIKKEI, NASDAQ Composite, Dow Jones.

So I give you the code of the backtest (excerpt from one of my e-books), you can test and verify for yourself.

Best Regards,

Marc (from France)

DEFPARAM CumulateOrders = False

IF currentmonth = 10 THEN

BUY 1 shares at market

ENDIF

IF currentmonth = 5 THEN

SELL at market

ENDIF

IF currentmonth = 5 THEN

SELLSHORT 1 shares at market

ENDIF

IF currentmonth = 10 THEN

EXITSHORT at market

ENDIF