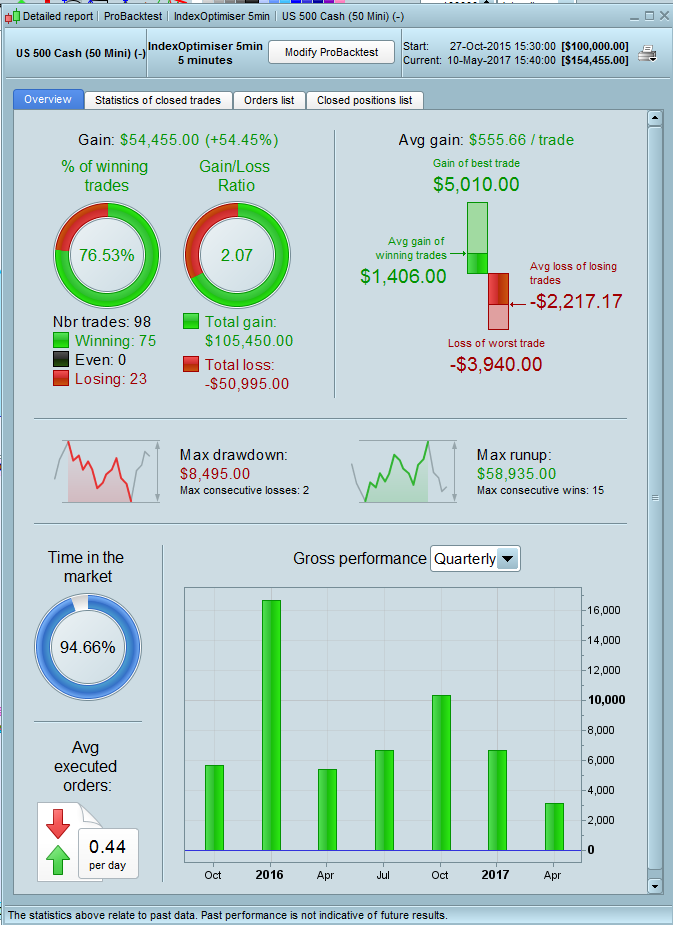

SP500 Optimizer 5min Strategy

{kind=link}

Good Day

I have been a silent member of this community for quite some time but suppose as time would allow I would try to become more active. I have been developing PRT strategies for almost 2 years now and have quite a few running live and profitable on various indexes and FX Pairs. I still need to get to a point where I can freely share my strategies but still find that slightly difficult (especially knowing some people sell your IP for profit). Anyhow this is just one of the many rabbit hole strategies I have developed in an effort to outperform a given index.

I actually wrote this today when the idea came to me to write a small time frame strategy that attempts to enter the market and take profit as soon as possible with the ability to stop and reverse direction quickly if the position becomes unprofitable. I am sure the general idea can be adapted to other timeframes and markets.

///Spread set to 0.9 points

possize = 1

pointsp = 20 //points where profit is to be locked in

pointsb = 36 //points where stop is to be taken

fast = average[11,4](close)

medium = average[13,4](close)

If countofposition = 0 then

If fast > medium then

BUY possize CONTRACT AT open + averagetruerange[3](close)*2 stop

EndIf

EndIf

If longonmarket and close >= positionprice + pointsp then

If close < close[1] then

SELL AT MARKET

EndIf

ElsIf longonmarket and close <= positionprice - pointsb then

SELLSHORT possize*2 CONTRACT AT MARKET

EndIf

If shortonmarket and close <= positionprice - pointsp then

If close > close[1] then

EXITSHORT AT MARKET

EndIf

ElsIf shortonmarket and close >= positionprice + pointsb then

BUY possize*2 CONTRACT AT MARKET

EndIf

SET TARGET pPROFIT 50

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}