SP500 - riding the trend

September 4, 2017, 4:54 PM

Strategies

16 Comments

{kind=link}

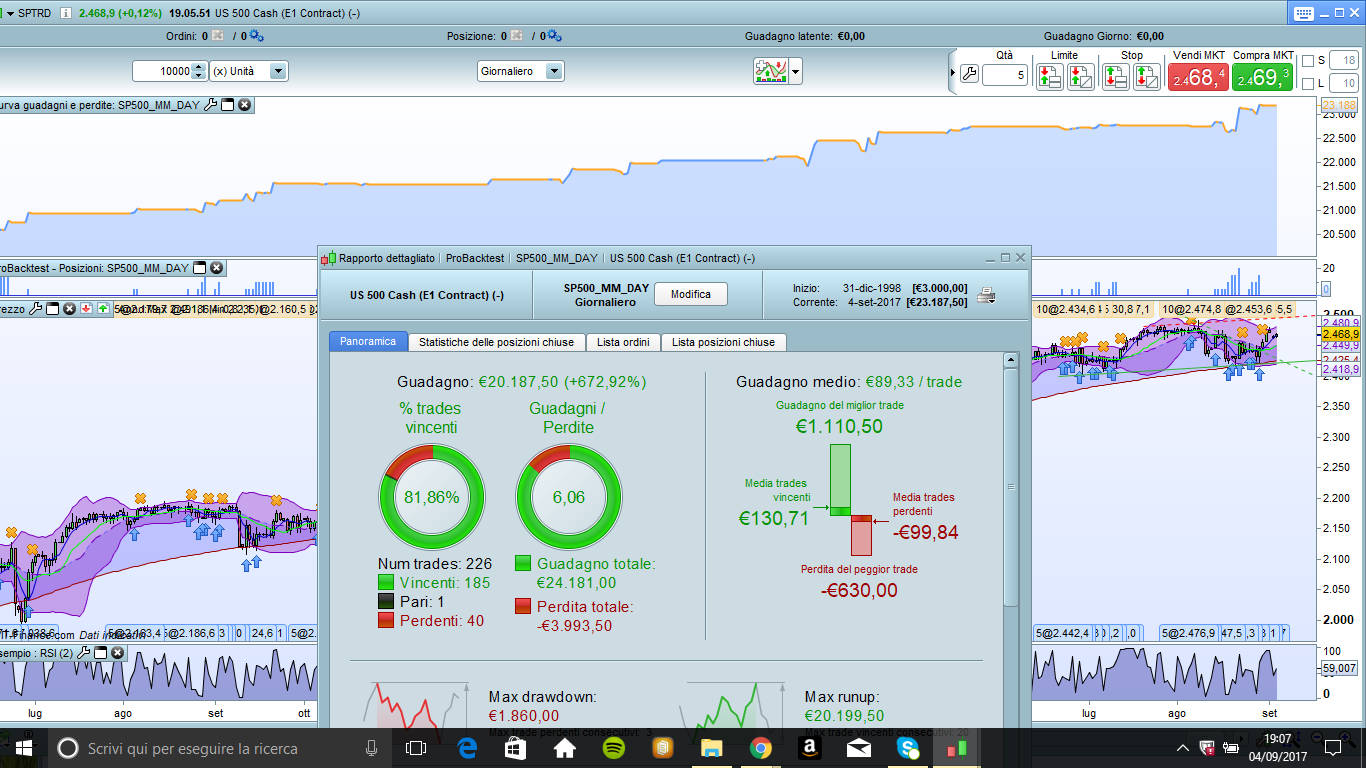

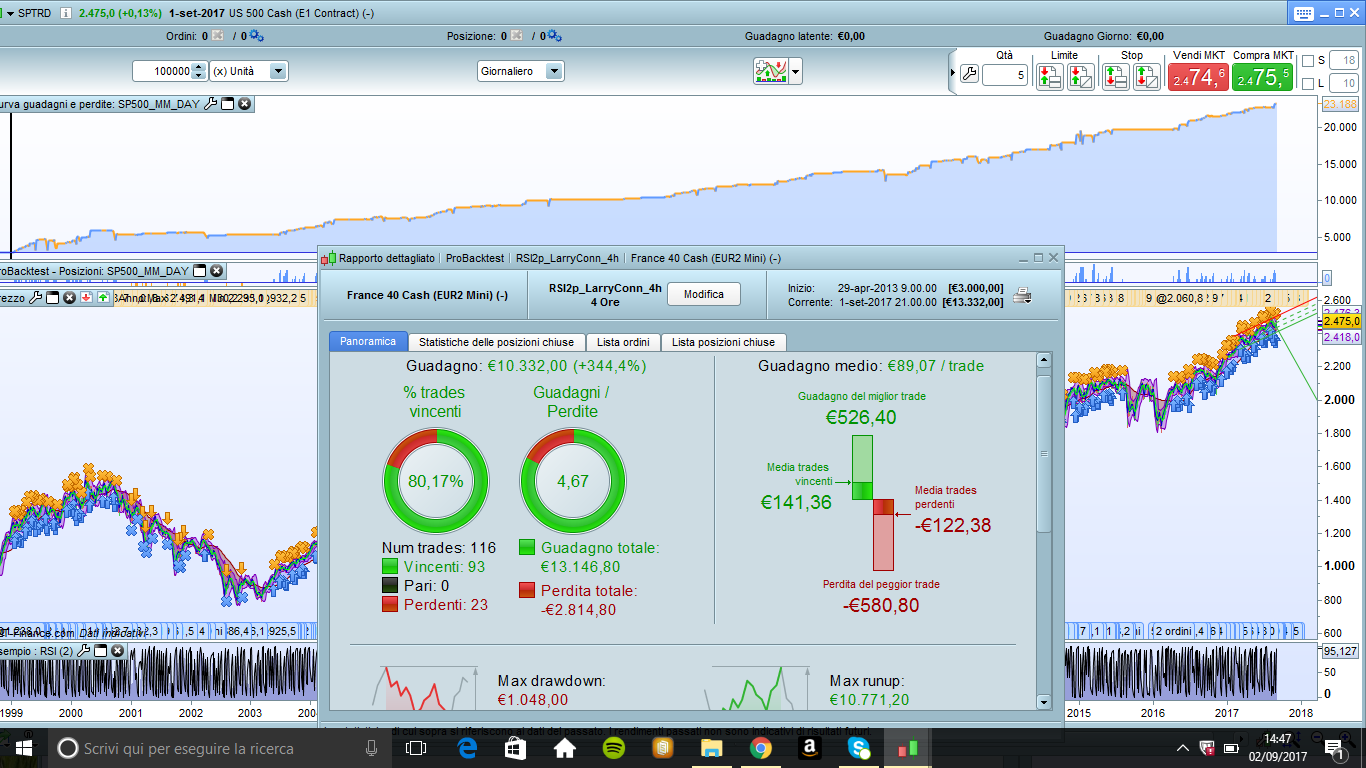

Simple strategy on S&P500 with “controlled” averaging down orders. Strategy has stoploss (100 points by default). Default is 5 contracts per order, but you can modify it in the code if you want (please adapt it to your account size). Could be adapted to other markets for sure.

// TF Giornaliero

// JR1976 TRADERS

// Molto Buono con Cumulate order LONG

// MM125=filtro lungo periodo , MM14 media di corto periodo per le operazioni long , MM4 media di corto periodo per le operazioni short + check RSI 2

// TIme Frame DAYLY

// MAX dd ...

// Loss ...

// JR1976 TRADERS

DEFPARAM Cumulateorders = true

//defparam flatafter = 220000

//defparam flatbefore = 130000

MM125=average[125](close)

MM14=average[14](close)

MM4=average[4](close)

RSI2 = RSI[2](close)

//h1 = high > Bollingerup[20]

short = RSI2 > 90

mm200=average[200](close)

// Condizioni per entrare su posizioni long

IF NOT LongOnMarket and close >MM125 and MM125>MM125[1] and close<MM14 THEN

BUY 5 CONTRACTS AT high stop

trading = 0

ENDIF

//if trading < 7 then

if trading < 5 then

//IF LongOnMarket and close>mm200 and Close-TRADEPRICE(1)>1 then

IF LongOnMarket and close>mm200 and TRADEPRICE(1)- close>1 then

BUY 5 CONTRACTS AT market

trading = trading +1

ENDIF

endif

// Condizioni per uscire da posizioni long

//If LongOnMarket AND close>mml and close>close[1] THEN

If LongOnMarket AND close>MM14 THEN

SELL AT market

ENDIF

// Stop e target: Inserisci qui i tuoi stop di protezione e profit target

if not shortonmarket and close<MM125 and MM125<MM125[1] and close>MM4 and short then

sellshort 5 contracts at low-3 stop

endif

if shortonmarket and close<MM4 and close<close[1] and TRADEPRICE(1)- close>1 then

exitshort at market

endif

//if shortonmarket then

//exitshort at high+10 stop

//endif

//set target pprofit 25

set stop ploss 100

Download

Filename:

SP500-riding-the-trend.itf

Downloads:

888

Download

{kind=link}

Filename:

1504538817l8cp4.png

Downloads:

435

Veteran

Algo trader

https://Scaffardi.blog

Author’s Profile

Loading...