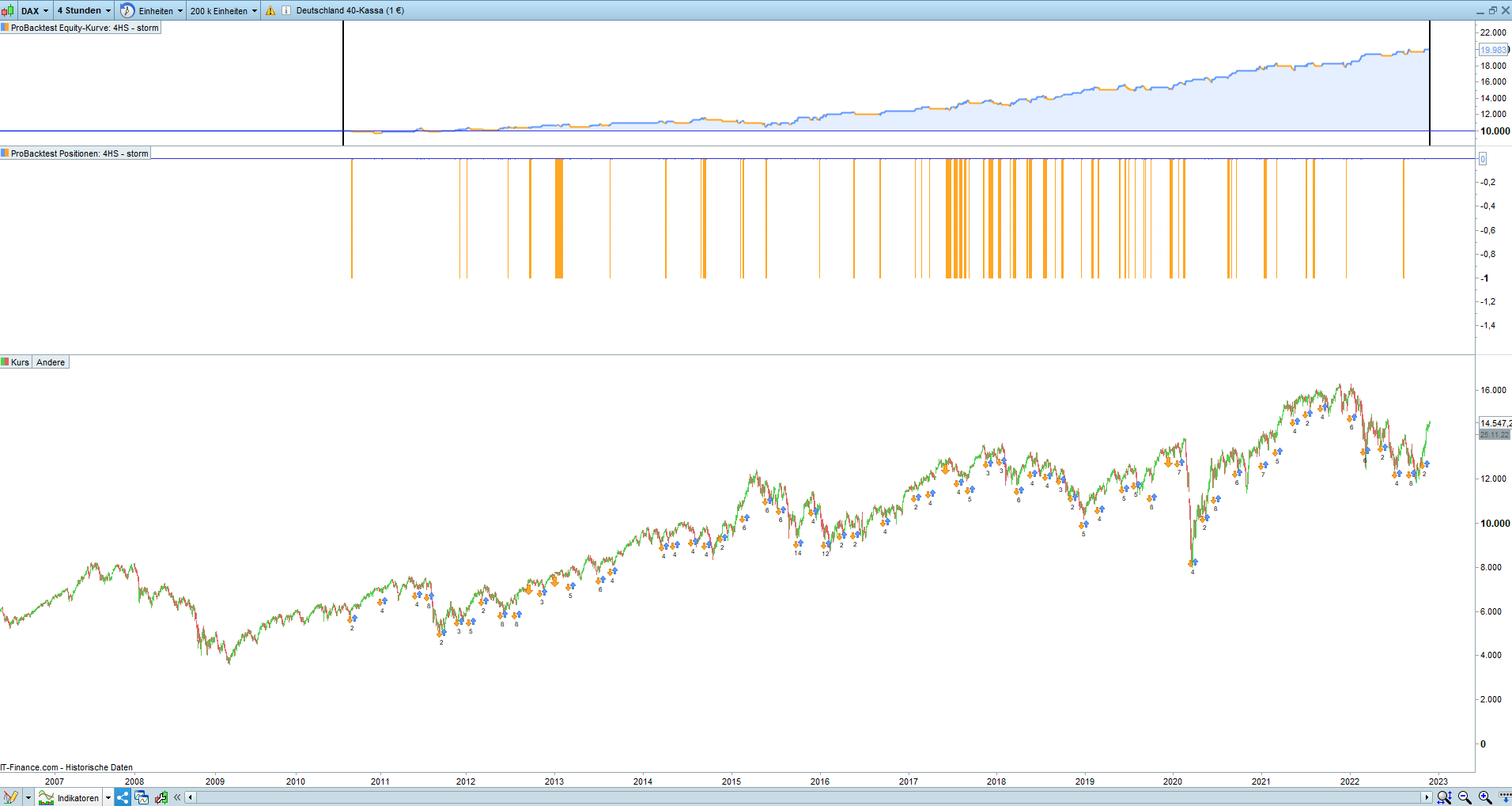

STORM - Short On Rising Markets

November 29, 2022, 1:35 PM

Strategies

6 Comments

{kind=link}

It’s pretty simple.

We take a fast average and a slow average.

We set two filters: the ATR and the time.

Now if the fast average is above the slow average and we get a simple 3 candle reversal we sell.

There is a fifty fifty chance, but this time we win.

//------------------------------------------------------------------

// OnlyShort Strategy on Dax

// Dax 1 Euro Mini

// TimeZone europe, berlin

// TimeFrame 4H

// MainCode : 4HS STORM - ShorT On Rising Markets

// created and coded by JohnScher

//------------------------------------------------------------------

defparam cumulateorders = false // works with true too

once ordersize = 1

//Pentuple Exponential Moving Average

period1 = 50

Period = MAX(Period1, 1)

MA1 = ExponentialAverage[Period](close)

MA2 = ExponentialAverage[Period](MA1)

MA3 = ExponentialAverage[Period](MA2)

MA4 = ExponentialAverage[Period](MA3)

MA5 = ExponentialAverage[Period](MA4)

MA6 = ExponentialAverage[Period](MA5)

MA7 = ExponentialAverage[Period](MA6)

MA8 = ExponentialAverage[Period](MA7)

PEMA = (8 * MA1) - (28 * MA2) + (56 * MA3) - (70 * MA4) + (56 * MA5) - (28 * MA6) + (8 * MA7) - MA8

//Hull Moving Average

period2 = 100

Period2 = MAX(Period2, 1)

HMA = WeightedAverage[ROUND(SQRT(Period2))](2 * WeightedAverage[ROUND(Period2 / 2)](close) - WeightedAverage[Period2](close))

// filter time

tm = openmonth <> 4 and openmonth <> 10

td = opendayofweek >= 2 and opendayofweek <= 5

tt = time >= 090000 and time <= 210000

// conditions

c1 = close > PEMA

c2 = PEMA > HMA

c3 = close < close[1] // 3-candle-revers, could be tested with some bearish candlestick pattern

c4 = close[2] < close[1]

c5 = averagetruerange [5] > 40 // filter, someone could be find betterone

// maincode

if tm and td and tt then

if c1 and c2 and c3 and c4 and c5 then

sellshort ordersize contracts at market

endif

endif

// fifty fifty chance

set stop %loss 2

set target %profit 2

// no trailing, no strategyprofit, no ...

Download

Filename:

STORM-ShortOnRisingMarkets.itf

Downloads:

354

Veteran

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...