Strategy TrendImpulse v1

April 28, 2020, 8:24 AM

Strategies

21 Comments

{kind=link}

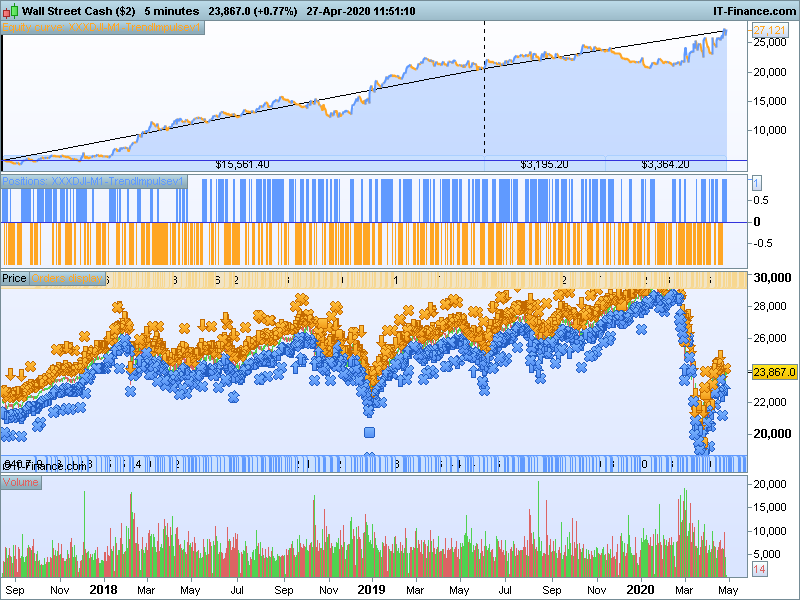

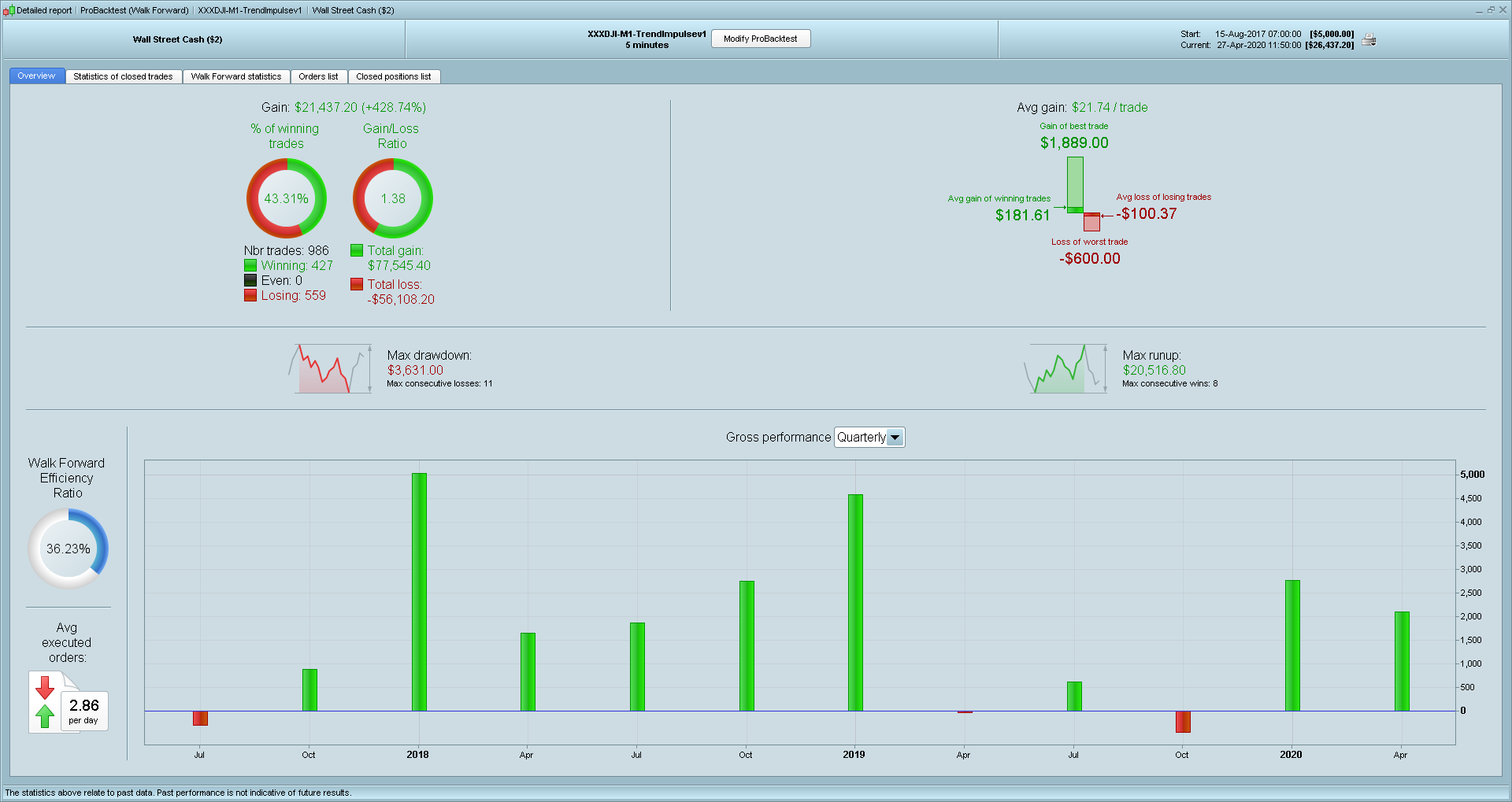

Here is a new strategy on Wall Street/DJI 5 min TF that utilize Perfect Trend Line as entry/exit and Trend Impulse Filter as trend direction. All credits to the original author.

DLS code is added to avoid high spread period. Time Zone used is UTC+08:00.

Forum for discussion https://www.prorealcode.com/topic/strategy-trendimpulse-v1/

DEFPARAM CumulateOrders = false

DEFPARAM PRELOADBARS = 1000

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

timeok = NOT(time >051500- USDLS AND time <053000 - USDLS) AND NOT(time >060000 - USDLS AND time <070000 - USDLS)

timeframe(5 minute)

thigh1 = Highest[SlowLength](high)+ SlowPipDisplace*pointsize

tlow1 = Lowest[SlowLength](low)- SlowPipDisplace*pointsize

thigh2 = Highest[FastLength](high)+ FastPipDisplace*pointsize

tlow2 = Lowest[FastLength](low)- FastPipDisplace*pointsize

if barindex>2 then

if Close>line1[1] then

line1 = tlow1

else

line1 = thigh1

endif

if Close>line2[1] then

line2 = tlow2

else

line2 = thigh2

endif

endif

if (Close[0]<line1[0] and Close[0]<line2[0]) then

trend = 1

endif

if (Close[0]>line1[0] and Close[0]>line2[0]) then

trend = -1

endif

if (line1[0]>line2[0] or trend[0] = 1) then

trena = 1

endif

if (line1[0]<line2[0] or trend[0] = -1) then

trena = -1

endif

if trena<>trena[1] then

if trena=1 then

//bear

prefecttrend = 2

else

//bull

prefecttrend = 1

endif

endif

timeframe(default)

once bb = src

if barindex>length then

src = (highest[length](high)+lowest[length](low))/2

rising = src-src[length]>0

falling = src-src[length]<0

aa = rising or falling

bb = exponentialaverage[centertrend](aa*src+(1-aa)*bb[1])

//—-

if bb>bb[1] then

//bull

trendimpulse = 1

elsif bb<bb[1] then

//bear

trendimpulse = 2

endif

endif

//====== Enter market - start =====

// LONG side

C1 = trendimpulse = 1 AND prefecttrend[1] = 2 AND prefecttrend = 1

IF timeok AND Not OnMarket AND C1 THEN

BUY 1 CONTRACT AT MARKET

SET STOP pLOSS SL

ENDIF

// SHORT side

C2 = trendimpulse = 2 AND prefecttrend[1] = 1 AND prefecttrend = 2

IF timeok AND Not OnMarket AND C2 THEN

SELLSHORT 1 CONTRACT AT MARKET

SET STOP pLOSS SL

ENDIF

//====== Enter market - end =====

//====== Exit market - start =====

X1 = prefecttrend[1] = 1 AND prefecttrend = 2

IF LONGONMARKET AND X1 THEN

SELL AT MARKET

ENDIF

X2 = prefecttrend[1] = 2 AND prefecttrend = 1

IF SHORTONMARKET AND X2 THEN

EXITSHORT AT MARKET

ENDIF

//====== Exit market - end =====

Download

Filename:

XXXDJI-M1-TrendImpulsev1-1.itf

Downloads:

1131

Download

{kind=link}

Filename:

DJI-5-minutes-2020_04_27-04h47_Result.png

Downloads:

560

Veteran

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...