Universal Strategy

{kind=link}

If you have followed the thread found here: https://www.prorealcode.com/topic/profitable-strategy-that-work-on-any-market/

You will be aware that I have placed a challenge to the forum to create a universal market neutral strategy. In other words a strategy that can be adapted to any market without ANY optimization. Below is my attempt at exactly this. I have opted to add a trading time filter as all markets have their sweet spot.

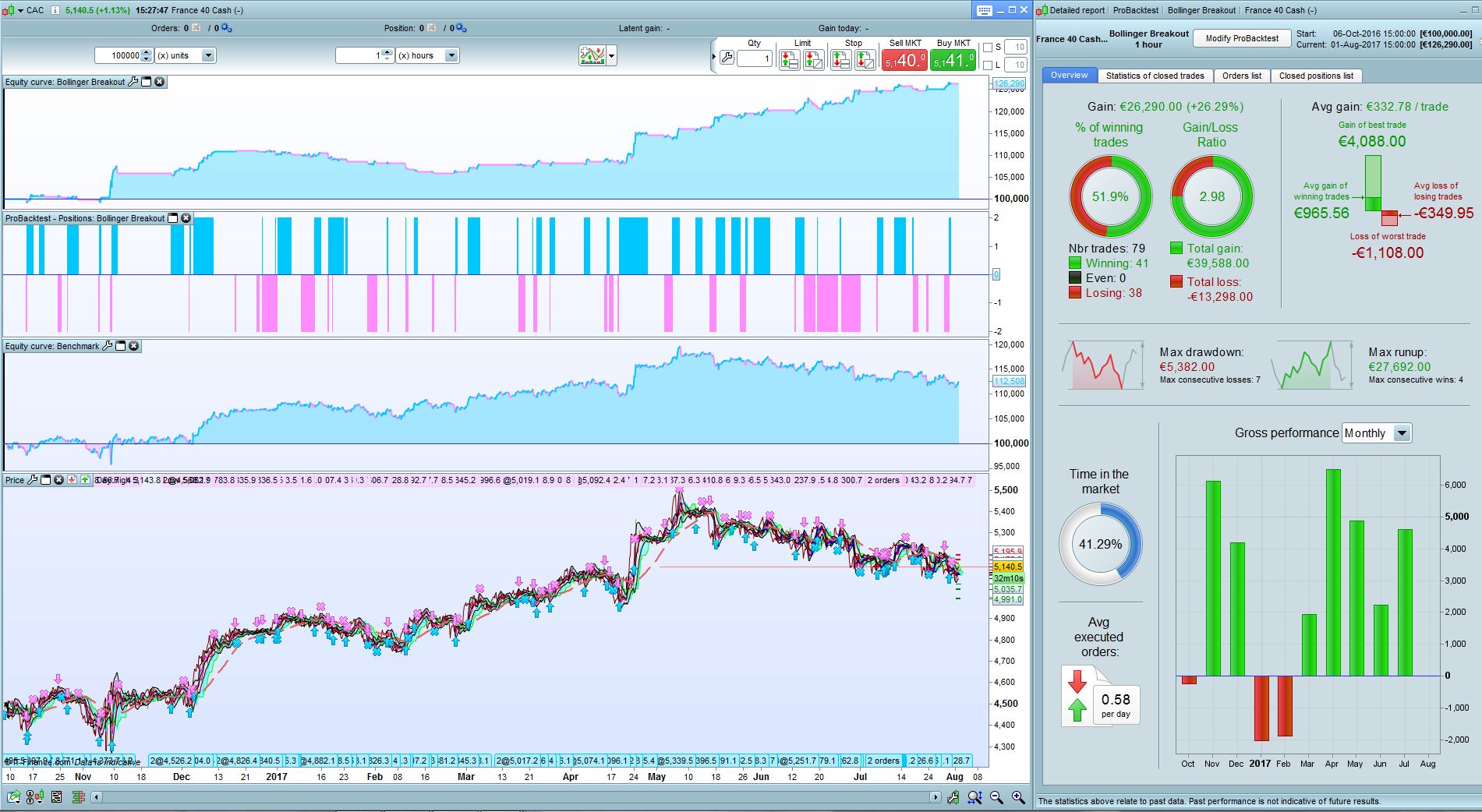

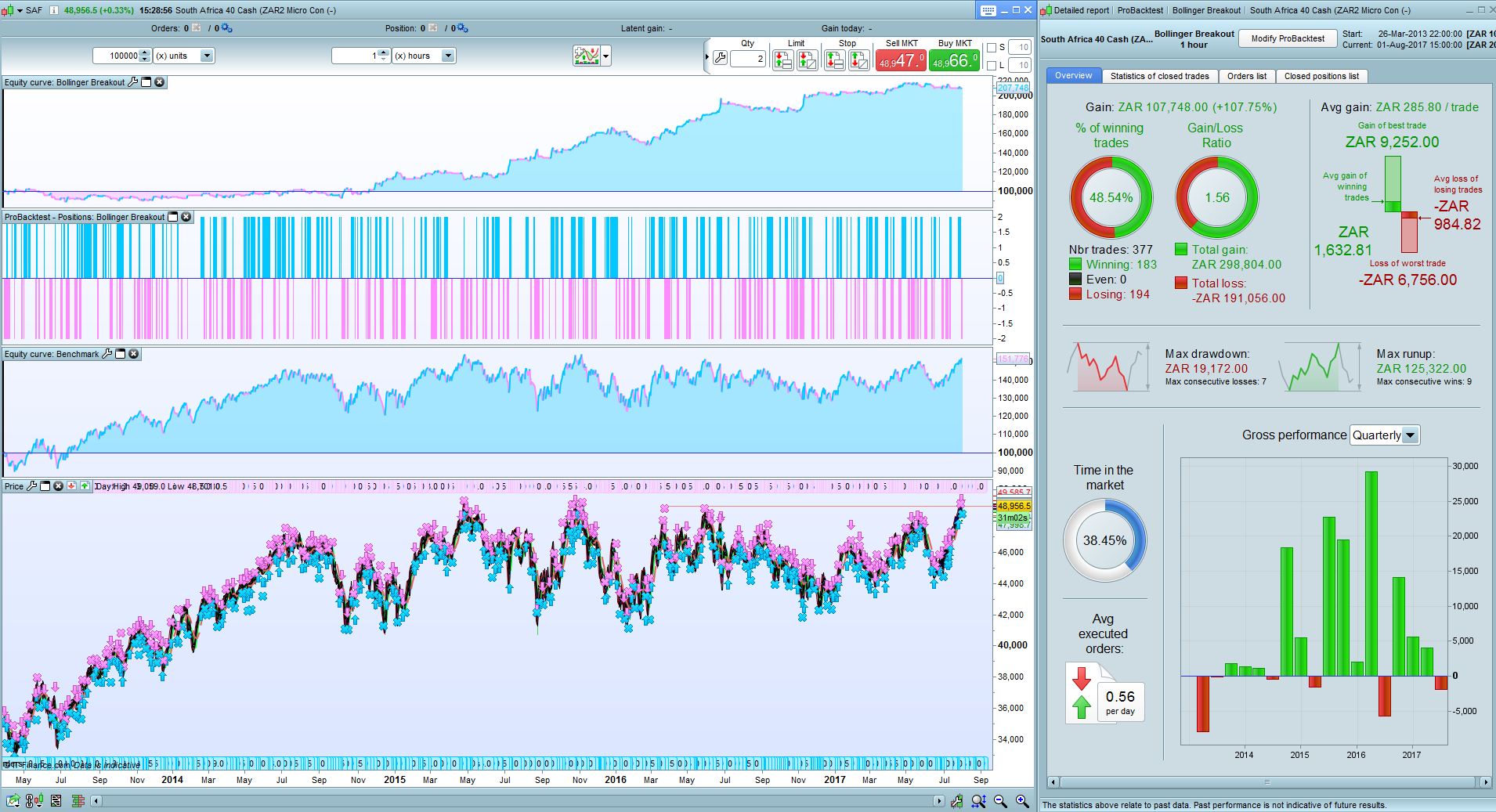

No variables have to be optimized for this strategy to work other than the trading time and spread. Attached is 2 screenshots of the same code executed on 2 different markets (same 1Hr timeframe but different spreads) where in both instances the code has significantly outperformed Buy and Hold. Spread on CAC40 set to 3 and spread on ZAF40 set to 20.

Note that this strategy was not meant to be a jaw dropper in terms of performance but rather a proof of concept that a single strategy can be applied to different markets with positive results. Obviously optimizing this strategy to individual markets will yield better results but that was never the idea. Hopefully the whole ProRealCode community can benefit from this (and even improve on it).

//Stategy: Universal Bollinger Breakout/Reversal

//Author: Juan Jacobs

//Market: Neutral

//Timeframe: 1Hr but not timeframe dependant

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

If hour > 0 and hour < 18 then //(CAC: 0-18, ZA: 0-18, DAX: 9-13,OMX: 8-11, US: 8-16, FTSE: 15-22, DOW: 8-22, EUR/USD: 9-23, AUD/USD: 3-17, GBP/USD: 10-23, EUR/GBP: 0-13, USCrude: 17-21, BrentCrude: 16-22, Gold: <2 or >22)

possize = 2

Else

possize = 0

EndIf

If dayofweek >= 5 and hour > 22 Then

If longonmarket Then

Sell at market

ElsIf shortonmarket Then

Exitshort at market

EndIf

EndIf

// Conditions to enter long positions

Periods = 42

Deviations = 1.618

PRICE = LOG(customclose)

alpha = 2/(PERIODS+1)

if barindex < PERIODS then

EWMA = AVERAGE[3](PRICE)

else

EWMA = alpha * PRICE + (1-alpha)*EWMA

endif

error = PRICE - EWMA

dev = SQUARE(error)

if barindex < PERIODS+1 then

var = dev

else

var = alpha * dev + (1-alpha) * var

endif

ESD = SQRT(var)

BollU = EXP(EWMA + (DEVIATIONS*ESD))

BollL = EXP(EWMA - (DEVIATIONS*ESD))

LongMA = Average[100](close)

RS2 = RSI[2](close)

ATR = AverageTrueRange[2](close)

If close > LongMA and RS2 > 70 and close[1] > BollU and close > BollU and open > open[2] Then

Buy possize contract at market

ElsIf close > LongMA and RS2 < 50 and close[1] > BollU and close < BollU Then

Sellshort possize contract at market

EndIf

If close < LongMA and RS2 < 40 and close[1] < BollL and close < BollL and open < open[2] Then

Sellshort possize contract at market

ElsIf close < LongMA and RS2 > 50 and close[1] < BollL and close > BollL Then

Buy possize contract at market

EndIf

If longonmarket and ((close < close[1] - ATR and RS2 < 5)) Then

Sell at market

ElsIf shortonmarket and ((close > close[1] + ATR and RS2 > 95)) Then

Exitshort at market

EndIf{kind=link}