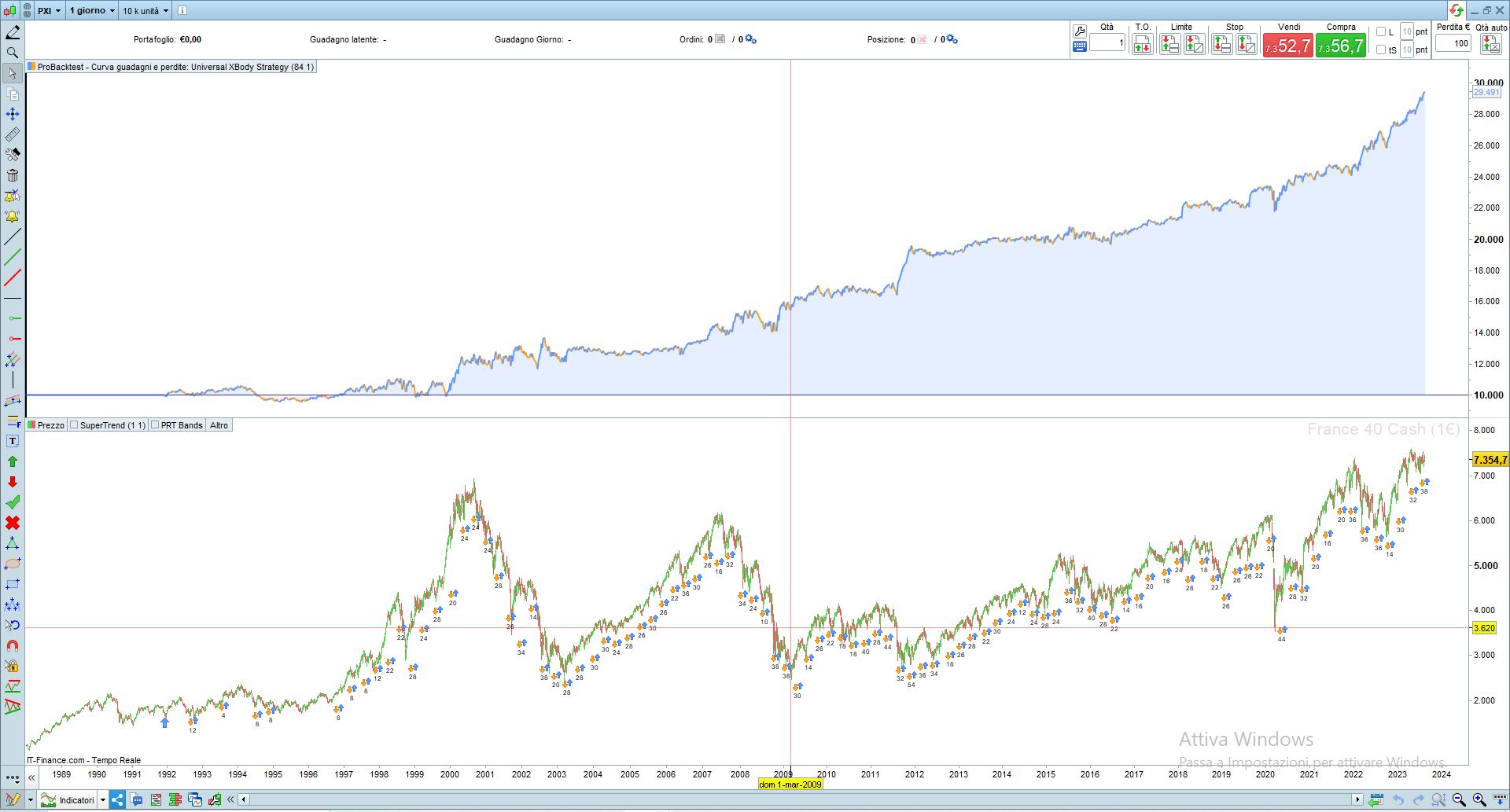

Universal XBody Strategy on CAC (1Day)

{kind=link}

Hello everyone,

I have the pleasure to share with you this simple but practical, universal daily strategy (for Forex, Indices, and Stocks), optimized on the CAC from 1992 to today. I hope that this opensource contribution can bring more developments in the field of automatic trading strategies on prorealtime, and demonstrate once and for all that a strategy to work does not necessarily have to be complicated, indeed (as I see it) the simpler it is, the more likely it is to work in the future as in the past.

- Brief explanation

The strategy has 3 fundamental parameters to optimize primarily which are: Period, Mode, and invertsignal. Once these have been chosen, we move on to the optimization of the two filters: filter1 and filter2. Finally, if you want you can add, a stop loss based on the average true average.

Here is the code

//Universal XBody STrategy

// instrument: CAC40

// timeframe : Daily

// Spread: 4

// created and coded by davidelaferla

//————————————————————————-

//-------------------------------------------------------------------------

defparam cumulateorders=false

//***********************************************************************************************************

N = 1

//------------------ SYSTEM VARIABLES---------------------------------------

//CAC40 Values: -------------------------------------------- Ottimization info

period=978// Optimize best value for each Symbol, range=1-1000, with step=1

mode=1// Optimize the best trading mode , range=1-4, with step=1

invertsignal=1// 1=positive signal, -1=negative signal, range=-1-1, with step=2

//***********************************************************************************************

//------------------ SYSTEM FILTER---------------------------------------

filter1=51// to set after the variable optimization, range=1-100, with step=1

filter2=0// to set after the variable optimization, range=1-100, with step=1

//------------------ INDICATOR ---------------------------------------

body=close-open

var=(body-body[1])

sumvar=summation[period](var)

if sumvar>filter1*pipsize then

green=(sumvar)

endif

if sumvar<-filter2*pipsize then

red=(sumvar)

endif

if mode=1 then

c1=red<red[1]

c2=green>green[1]

endif

if mode=2 then

c1=red>red[1]

c2=green<green[1]

endif

if mode=3 then

c1=red<red[1]

c2=green<green[1]

endif

if mode=4 then

c1=red>red[1]

c2=green>green[1]

endif

if c1 then

signal=1*invertsignal

elsif c2 then

signal=-1*invertsignal

endif

// Conditions for entering long positions and exit short positions

IF signal>0 then

BUY n contract AT market

ENDIF

// Conditions for entering short positions and exit long positions

IF signal<0 THEN

SELLSHORT n CONTRACTs AT market

ENDIF