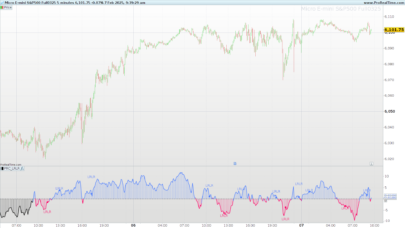

This is a system I made over 6 months ago and have been running live on the DAX 30m. It is based on identifying tops or bottoms in the price. When a breakout from these levels occur it tries to capture the movement, in either direction. It averages 1.55 trades/day and is flat overnight. It employs some simple filters and varied position sizes.

Important things to know:

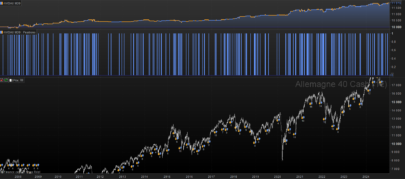

- The system is heavily optimized, in that there are many moving parts, but it has performed out of sample since Nov 2, 2016. You may want to optimize it again if you plan on running it.

- System is backtested on a spread of 1, but 1.3 or so may be more accurate.

- I have also used similar systems on lower timeframe DAX (10m and 15m), and it can be optimized for other markets.

- If you do optimize, run an OOS or live demo test before trying to run it live. I take no responsibility what you do with the code (unless you make a profit of course).

- This system is in many ways a guide on how to NOT program a strategy, but I only want to share systems that I have run live for a long time and trusted with my own money.

I can answer your questions in the comments.

Strategy code:

|

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 100 101 102 103 104 105 106 107 108 109 110 111 112 113 114 115 116 117 118 119 120 121 122 123 124 125 126 127 128 129 130 131 132 133 134 135 136 137 138 139 140 141 142 143 144 145 146 147 |

///////////////////////////////////// // Wing's Resistance Breacher // DAX 30m timeframe. Last optimized Nov 2, 2016 // // Made by user "Wing" of ProRealCode.com // https://www.prorealcode.com/user/wing/ ///////////////////////////////////// defparam cumulateorders=false stoch=Stochastic[8,3](close) mm2=exponentialaverage[8] // Position size module, 2 is the default. Can be adapted to scale with the profits ///////////////////////////////////////////////////////////////////////// positionsize=2//+2*round((strategyprofit*2)/10000) maybe= positionperf(1)<0 losses = positionperf(1)<0 and positionperf(2)<0 if losses then PositionSize = 3//+3*round((strategyprofit*2)/10000) elsif not losses then PositionSize = 2//+2*round((strategyprofit*2)/10000) Endif if maybe and not losses then positionsize=3//+3*round((strategyprofit*2)/10000) endif if positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0 then positionSize=2//+2*round((strategyprofit*2)/10000) endif if positionperf(1)>0 and positionperf(2)>0 then positionsize=1//+1*round((strategyprofit*2)/10000) endif if positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0 and positionperf(4)<0 and positionperf(5)<0 and positionperf(6)<0 then positionsize=5 endif if positionperf(1)>0 and positionperf(2)>0 and positionperf(3)>0 and positionperf(4)>0 and positionperf(5)>0 and positionperf(6)>0 then positionsize=1 endif /////////////////////////////////////////////////////////////////////////////////// // Optimization variables //////////////////////////////////////////////////////////////////////////////// bul=3.5 //long, SL but=12 // long, PT shl=6.5 // Short, SL sht=3.5 // Short PT lowt=65 // stochastic filter test=45 //stochastic filter mmlean=1.0002 // Moving average lean filter mmlean2=1.0005 // Moving average lean filter // moving averages yy=47 tt=53 //////////////////////////////////////////////////////////////////////////////// minSL=20 // minimum SL lasttime=210000 // last time to open position which=10 // Parameter of the ATR for SL/TP once mabot=0 once mabotz=0 once maboty=0 once mabotzy=0 if time<lasttime then if time>080000 and dayofweek>1 and stoch>test and mm2[1]*mmlean<mm2 and averagetruerange[which]*bul> minSL and go=1 and mm2[1]*mmlean2>mm2 and close>MaBotzy and onmarket=0 then buy PositionSize lot at market mystop=averagetruerange[which]*bul myprofit=averagetruerange[which]*but go=0 endif if time>080000 and stoch<Lowt and mm2*mmlean<mm2[1] and go=1 and mm2*mmlean2>mm2[1] and averagetruerange[which]*shl>minSL and close<MaBotz and onmarket=0 then sellshort PositionSize lot at market mystop=averagetruerange[which]*shl myprofit=averagetruerange[which]*sht go=0 endif endif // Identifying tops/bottoms in price ////////////////////////////////////////////////////////////////////// if close<average[yy] and close<exponentialaverage[tt] and MaBot=0 then MaBot=close go=1 endif if close<average[yy] and close<exponentialaverage[tt] and Mabot>0 and close<MaBot then mabot=close endif if close<average[yy] and close<exponentialaverage[tt] and Mabot>0 and close>MaBot then MaBotz=MaBot endif if close>average[yy] or close>exponentialaverage[tt] then MaBot=0 MaBotz=0 endif if close>average[yy] and close>exponentialaverage[tt] and MaBoty=0 then MaBoty=close go=1 endif if close>average[yy] and close>exponentialaverage[tt] and Maboty>0 and close>MaBoty then maboty=close endif if close>average[yy] and close>exponentialaverage[tt] and Maboty>0 and close<MaBoty then MaBotzy=MaBoty endif if close<average[yy] or close<exponentialaverage[tt] then MaBoty=0 MaBotzy=0 endif ///////////////////////////////////////////////////////////////////////////////////// // Sell at end of day if time>215300 then exitshort at market sell at market endif // Earlier friday exit. Insurance against accidental holding over weekends if dayofweek=5 and time>212300 then exitshort at market sell at market endif set target profit myprofit set stop loss mystop |

Share this

No information on this site is investment advice or a solicitation to buy or sell any financial instrument. Past performance is not indicative of future results. Trading may expose you to risk of loss greater than your deposits and is only suitable for experienced investors who have sufficient financial means to bear such risk.

ProRealTime ITF files and other attachments :

Find other exclusive trading pro-tools on ![]()

PRC is also on YouTube, subscribe to our channel for exclusive content and tutorials

Thanks Wing great strategy, I like your position sizing , did you try with other assets?

Yes, I have tried to trade gold using a strategy like this. It worked, but the spread is not as favorable. FX I have not tried at all.

Thanks, Ill try to check some ccy pairs then.

Have a nice day

Thanks,

Very interesting.

Is it still running good?

As it says in description, it has been running live since Nov 2016. Everything after Nov 2 is out of sample, and shows performance so far, which is decent. If it works tomorrow or a year from now? No idea.

Hi, how many contracts for max/min size? How big should the account size be?

The system trades 1 to 3 contracts, and 5 under extreme circumstances. If trading the DAX 1 euro/point then I suggest you have at least 2000 or 3000 euro in your account, considering the system’s past drawdown.

Wing

Can i find you on Twitter?

Hi Wing,

Your code looks quite interresting.

I was wondering if you could develop a bit more on :

how the system “decides” to trade 1 or 2 or 3 contracts as the code looks a bit complex to me, please

and if the fact that you are using previous performance positions in it means that your system should be the only one to work on a dedicated instrument

finally I am not sure I understand the “21h53” exit condition that will execute anyway at 22h00 if I m not mistaken (as the TF is 30 minutes)

Thanks again and for the time you will take to give answer.

The larger than sign (>) means that it will trigger at 54 or later, i.e. also 22:00.

Hi Wings, i did not found a forum thread for this interesting system so i post my comment here.

I’m running it live in demo account since 12 july without touching optimization, and so far it gained 455 euros. It seems pretty good, but i’ve got a big backslash of bad trading from 14 july to 26 july, 7 consecutive loss for 1k of losses. Maybe this can be avoided by optimization.

Stats are:

16 Trades: 6 win, 10 loss

1.32 Gains / Losses

Max DD: 864,60

Max consecutives lossing trade: 7

Max Runup: 878,50

Max consecutives winning trade: 2

Time on Market: 46,7%

Good work anyway.

Hi Wing, nice work!!!

question: could you put a trailing stop in it? like: after profit of points x start trailing stop with a trailing step?

like this: trailingstart = 25 //trailing will start @trailinstart points profit

trailingstep = 30 //trailing step to move the “stoploss

Seems like it always closes position at 22:00:0X time?

Sorry for not responding to a lot of you. System seems to still be going strong.

Yes, position will close at 22:00:0X, since execution/calculation is not always immediate.

I can’t put a trailing stop in it, but you can.

Not posting my Twitter for certain reasons.

Hi Wing, I have been using your code and it has been quite profitable until now indeed! So first of all thank you very much for sharing it. I am wondering as there are many variables, which one would you choose in case you wanted to reoptimize it? Thank you!!!

Thank you. I also run it so I am glad it has worked. To optimize I would prioritise the SL and TP. The other variables are filters and not as important. Notably, the short SL is greater than short TP, which is unusual.

Hi Wing, First of all : bravo ! Your strategy is great. Anyway in demo, it looks like October 2017 (which is not over yet) is quite poor. The worst performing month since you started it live if I am not mistaken. Anyway, overall, strategy is great.

Would it be worth to backtest it in Walk Forward ? (can’t do it myself).

Thanks again.

I ran a test with the code, in demo account, since 06/24/17

71 Trades

thereof 34 profit

thereof 37 loss

Profit: 1.838 Euro

max drawdown 416 Euro

max Runup 520 Euro

Ich habe einen Test laufen lassen mit dem Code , im Demo-Account, seit 24.06.17

71 Trades

davon 34 Gewinn

davon 37 Verlust

Gewinn: 1.838 Euro

max Drawdown 416 Euro

max Runup 520 Euro

Demnächst werde ich den Backtest für diesen Zeitraum drüber laufen lassen und die Ergebnisse vergleichen. Bin gespannt. Wenn die Ergebnisse einigermaßen identisch sind, werde ich versuchen mit 2,3 Oszillatoren das Ergebnis zu verbessern.

Liebe Grüße

JohnScher

Interesting system. I tried to understand the method to determine new highs and lows, and I think there is a logical error in lines 125-128. I think these lines are supposed to mean : When close is below one of the averages (close<average[yy] or close0 (close>MaBotzy), ALTHOUGH there is NO uptrend.

For the short positions, I think this is correctly coded. Lines 108-111 mean that there is no downtrend anymore, and both the low of the downtrend MaBot and the threshold for short positions MaBotz are set to 0. In line 83, this means, that in the following bar, a short position can NEVER be opened, because close cannot be smaller than 0 (value of MaBotz). This is correct, because there is no downtrend (close is above one of the averages) and therefore no short positions can be opened.

I think that “in principle”, in order to make the decisions for long and short orders equivalent, the values of MaBoty and MaBotzy should be set to a very large value in lines 126 and 127, for example MaBoty=1000000000, and MaBotzy=1000000000. Then, in the next bar, a long position will also NEVER be opened in line 76, because there is no uptrend.

Am I wrong, or did I understand something in the wrong way ?

I try once again. Part of my previous post disappeared, and it is therefore unintelligible.

Interesting system. I tried to understand the method to determine new highs and lows, and I think there is a logical error in lines 125-128. I think these lines are supposed to mean : When close is below one of the averages (close<average[yy] or close0 (close > MaBotzy) is always true, a new long position can ALWAYS be opened in the next bar, although there is no uptrend.

For the short positions, I think this is correctly coded. Lines 108-111 mean that there is no downtrend anymore, and both the low of the downtrend MaBot and the threshold for short positions MaBotz are set to 0. In line 83, this means, that in the following bar, a short position can NEVER be opened, because close cannot be smaller than 0 (value of MaBotz). This is correct, because there is no downtrend (close is above one of the averages) and therefore no short positions can be opened.

I think that “in principle”, in order to make the decisions for long and short orders equivalent, the values of MaBoty and MaBotzy should be set to a very large value in lines 126 and 127, for example MaBoty=1000000000, and MaBotzy=1000000000. Then, in the next bar, a long position will also NEVER be opened in line 76, because there is no uptrend.

Am I wrong, or did I understand something in the wrong way ?

Same thing again. Post was truncated. Once again the lost remarks :

I think there is a logical error in lines 125-128. I think these lines are supposed to mean : When close is below one of the averages (close<average or close0 (close > MaBotzy) is always true, a new long position can ALWAYS be opened in the next bar, although there is no uptrend.

Does not work. Sorry, not my fault.

Only MaBotzy in line 127 should be set to a large value, for example MaBotzy = 10000000. MaBoty must be set to 0 in line 126, this is correctly coded. When MaBotzy is 0, in line 76 this would mean that the threshold above which a new long position can be opened is 0, i.e. a long position could always be opened.

I agree with verdi55. As it is now, the code will only test for a breakout on the upside (lines 113 to 128) when the close is above the MA and EMA. But, when the close is below the MA and EMA the system will still trade long because the condition for this is close > mabotzy and mabotzy = 0. Therefore it is entering long positions, without actually testing for a breakout, whenever the close is below the MA and EMA.

I also agree with his other comment that this will be fine as long as you are in a long-term uptrend, but when a long downtrend comes along it will hurt.

The system greatly favors long over short positions, because MaBotzy=0 in line 127 and MaBotz=0 in line 110. This means it will work fine in long-term upward trends, but probably not so well in long-term downward trends, i.e. in a traditional baisse.

Hello Verdi,

I’m not sure to understand what you mean..Did you tried to test with your correction?

Does anyone trade the program real and in a live account?

I have it running in demo account, see attachment.

yes i’m running it live

http://prntscr.com/hzhvfx

http://prntscr.com/hzhvzh

http://prntscr.com/hzhwcc

I’ve been running it live since 26th of september with MM, P/L is 1.08 and total gain is about €288. Not too great considering I’m running the dynamic position code which takes more than one contract at a time.

Hi,

I’ve had this strategy running for a month now. But during this period, it has not made any trade. But in a backtest it should have done it. What am I doing wrong?

Have I installed the code incorrectly? Have enough money on your account so it can not be that!

Thanks for your help :))

/////////////////////////////////////

defparam cumulateorders=false

DEFPARAM PRELOADBARS = 150

stoch=Stochastic[8,3](close)

mm2=exponentialaverage[8]

// Position size module, 2 is the default. Can be adapted to scale with the profits

/////////////////////////////////////////////////////////////////////////

positionsize=2//+2*round((strategyprofit*2)/10000)

maybe= positionperf(1)<0

losses = positionperf(1)<0 and positionperf(2)<0

if losses then

PositionSize = 3//+3*round((strategyprofit*2)/10000)

elsif not losses then

PositionSize = 2//+2*round((strategyprofit*2)/10000)

Endif

if maybe and not losses then

positionsize=3//+3*round((strategyprofit*2)/10000)

endif

if positionperf(1)<0 and positionperf(2)<0 and positionperf(3)0 and positionperf(2)>0 then

positionsize=1//+1*round((strategyprofit*2)/10000)

endif

if positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0 and positionperf(4)<0 and positionperf(5)<0 and positionperf(6)0 and positionperf(2)>0 and positionperf(3)>0 and positionperf(4)>0 and positionperf(5)>0 and positionperf(6)>0 then

positionsize=1

endif

///////////////////////////////////////////////////////////////////////////////////

// Optimization variables

////////////////////////////////////////////////////////////////////////////////

bul=3.5 //long, SL

but=12 // long, PT

shl=6.5 // Short, SL

sht=3.5 // Short PT

lowt=65 // stochastic filter

test=45 //stochastic filter

mmlean=1.0002 // Moving average lean filter

mmlean2=1.0005 // Moving average lean filter

// moving averages

yy=47

tt=53

////////////////////////////////////////////////////////////////////////////////

minSL=20 // minimum SL

lasttime=210000 // last time to open position

which=10 // Parameter of the ATR for SL/TP

once mabot=0

once mabotz=0

once maboty=0

once mabotzy=0

if time080000 and dayofweek>1 and stoch>test and mm2[1]*mmlean minSL and go=1 and mm2[1]*mmlean2>mm2 and close>MaBotzy and onmarket=0 then

buy PositionSize lot at market

mystop=averagetruerange[which]*bul

myprofit=averagetruerange[which]*but

go=0

endif

if time>080000 and stoch<Lowt and mm2*mmleanmm2[1] and averagetruerange[which]*shl>minSL and close<MaBotz and onmarket=0 then

sellshort PositionSize lot at market

mystop=averagetruerange[which]*shl

myprofit=averagetruerange[which]*sht

go=0

endif

endif

// Identifying tops/bottoms in price

//////////////////////////////////////////////////////////////////////

if close<average[yy] and close<exponentialaverage[tt] and MaBot=0 then

MaBot=close

go=1

endif

if close<average[yy] and close0 and close<MaBot then

mabot=close

endif

if close<average[yy] and close0 and close>MaBot then

MaBotz=MaBot

endif

if close>average[yy] or close>exponentialaverage[tt] then

MaBot=0

MaBotz=0

endif

if close>average[yy] and close>exponentialaverage[tt] and MaBoty=0 then

MaBoty=close

go=1

endif

if close>average[yy] and close>exponentialaverage[tt] and Maboty>0 and close>MaBoty then

maboty=close

endif

if close>average[yy] and close>exponentialaverage[tt] and Maboty>0 and close<MaBoty then

MaBotzy=MaBoty

endif

if close<average[yy] or close215300 then

exitshort at market

sell at market

endif

// Earlier friday exit. Insurance against accidental holding over weekends

if dayofweek=5 and time>212300 then

exitshort at market

sell at market

endif

set target profit myprofit

set stop loss mystop

I do not run this strategy myself, currently. As for why it is not taking trades live: Do you have it running the correct timeframe? Have you put a position limit too low? Even if you get no trades going through, do you see any rejected orders?

Hey,

Yes it´s running in 30 m timeframe. I had it running and it made two trads in january. Then I thought I needed to add (PRELOADBARS = 150) but that has not helped! Strange that it made two trads and then no more.

How do I know if position limit is too low?

No rejected orders!

Can I ask you why you do not have the strategy running?

Big thanks for your help, I’m quite new to this so happy for all the help I can get. Finds this super interesting :))

There’s a few threads on the forum about backtest and live trades being different at times. I suggest looking in them for reasons.

I run 0 automated strategies at the moment, but that’s just me being picky with running suitable systems and not distracting myself from manual trading (which I do a lot).

are u still active Wing?