I’m not sure ValueY is “broken” when it flatlines, I think it’s more to do with the settings that the code. Let me take a look at the code above.

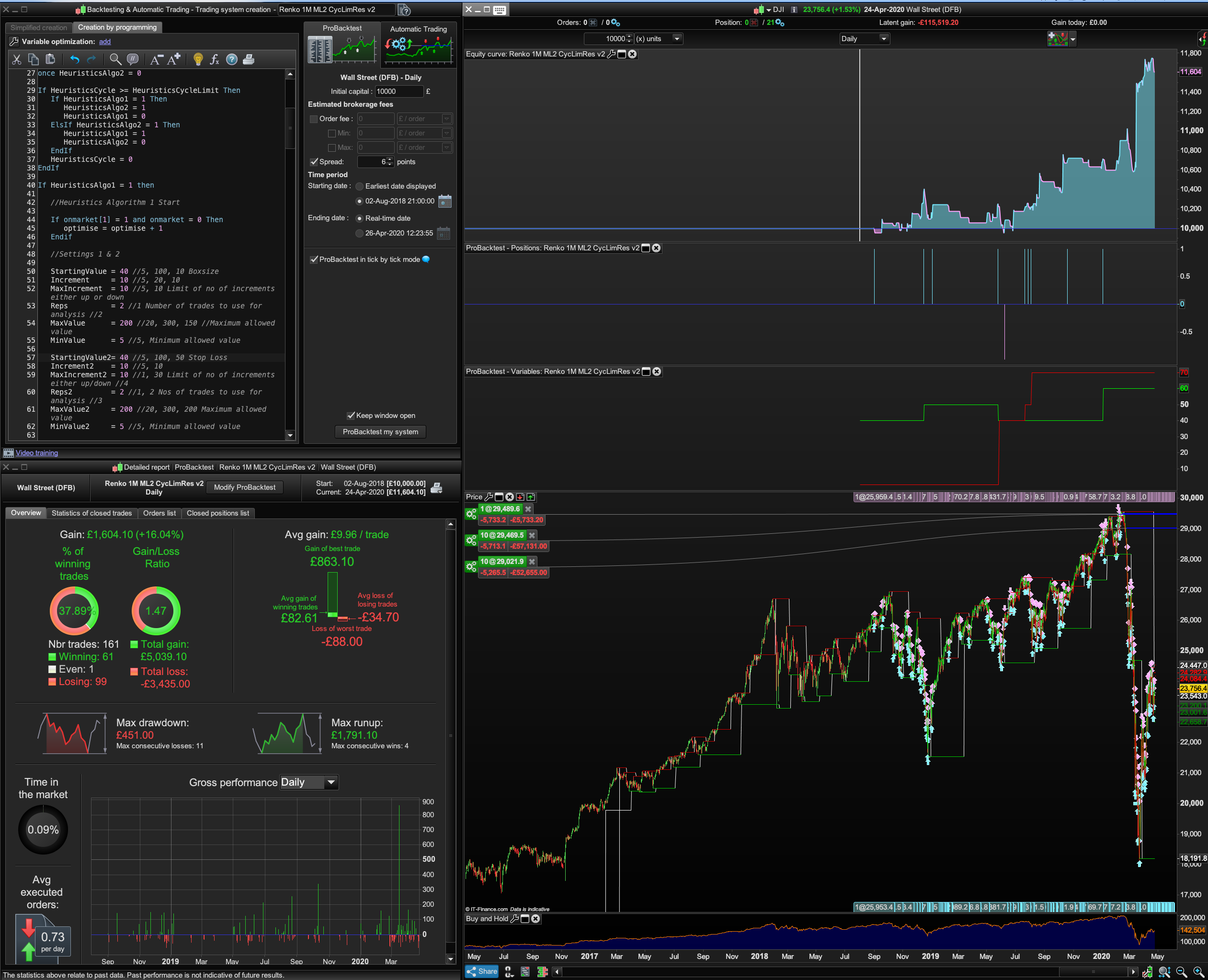

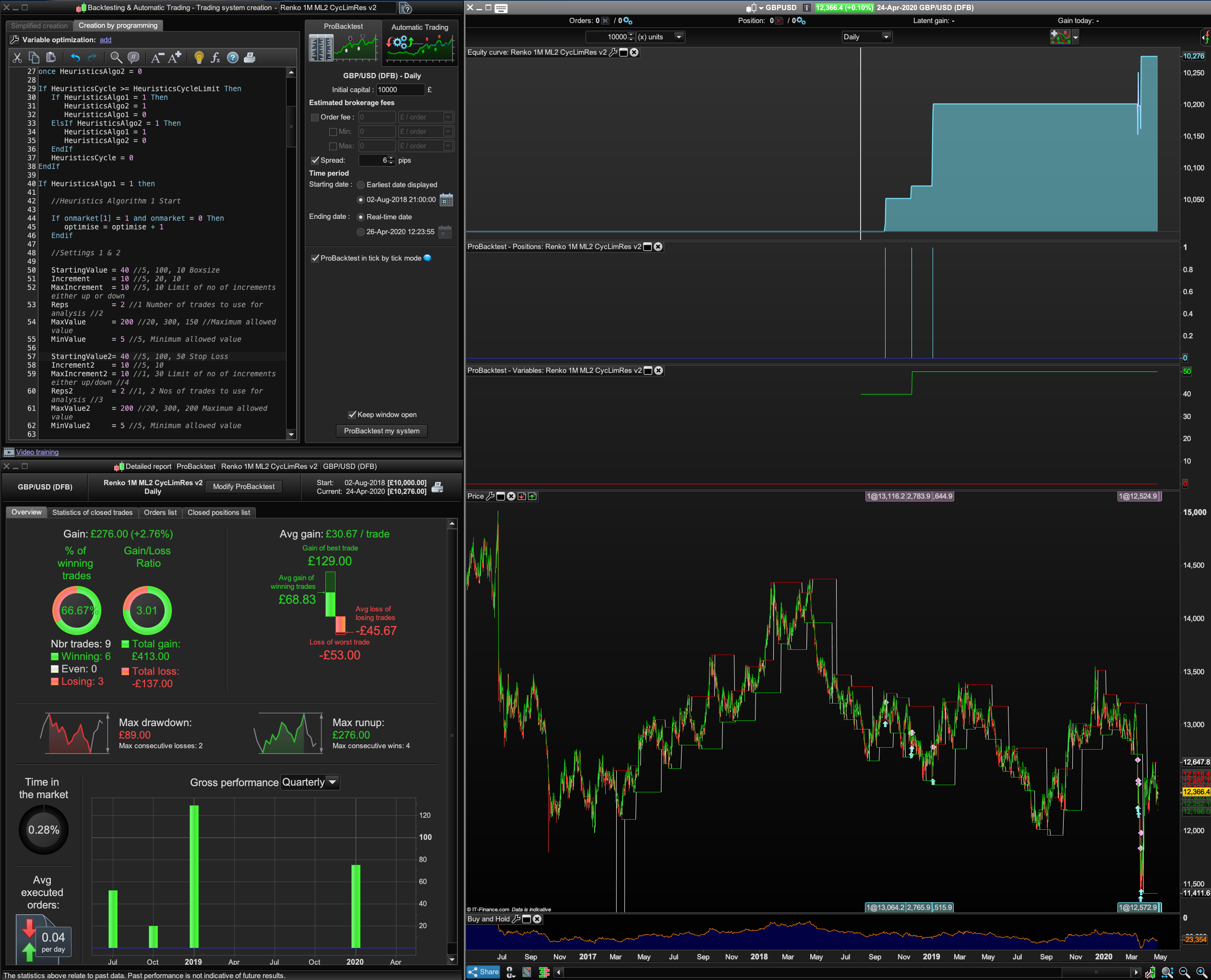

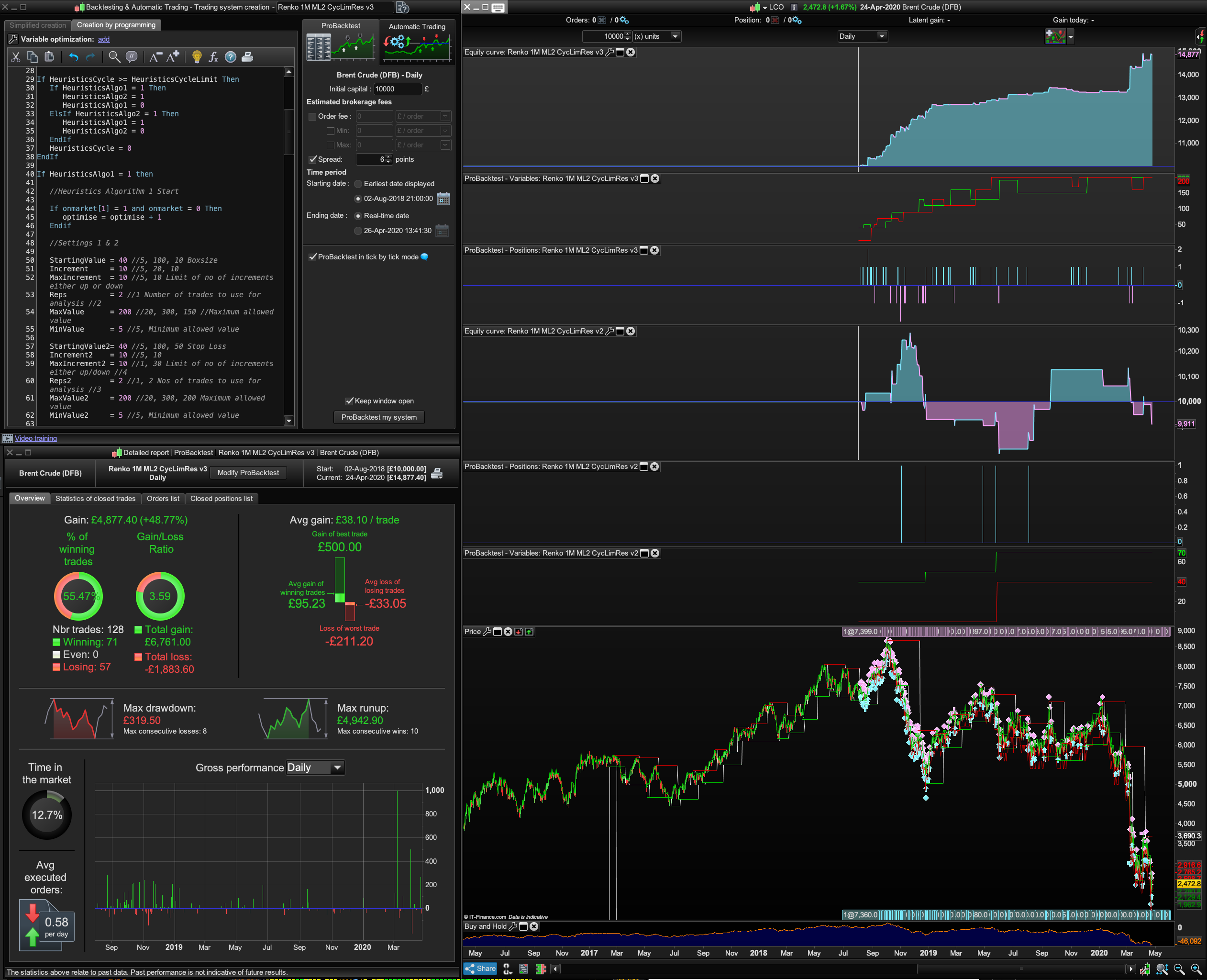

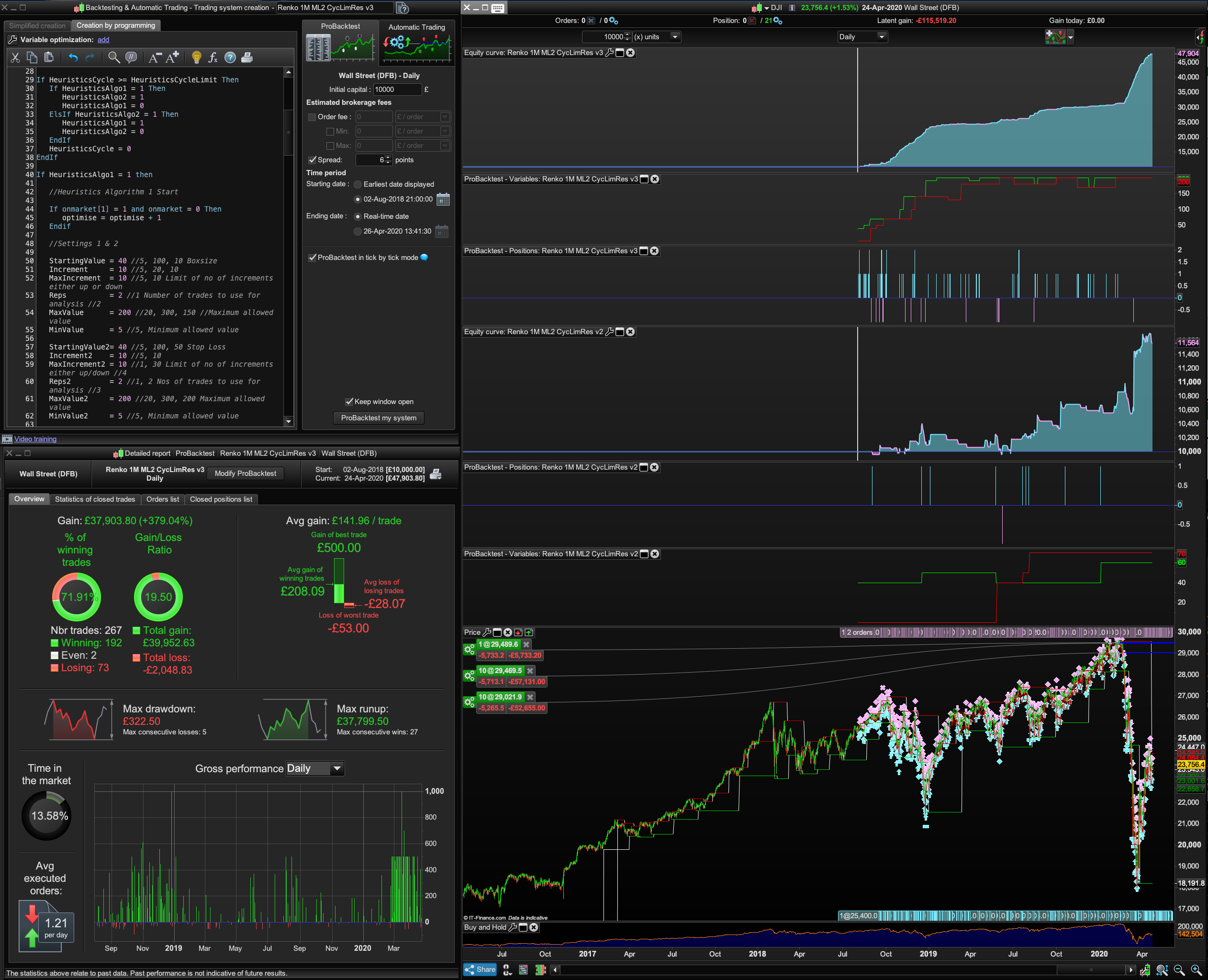

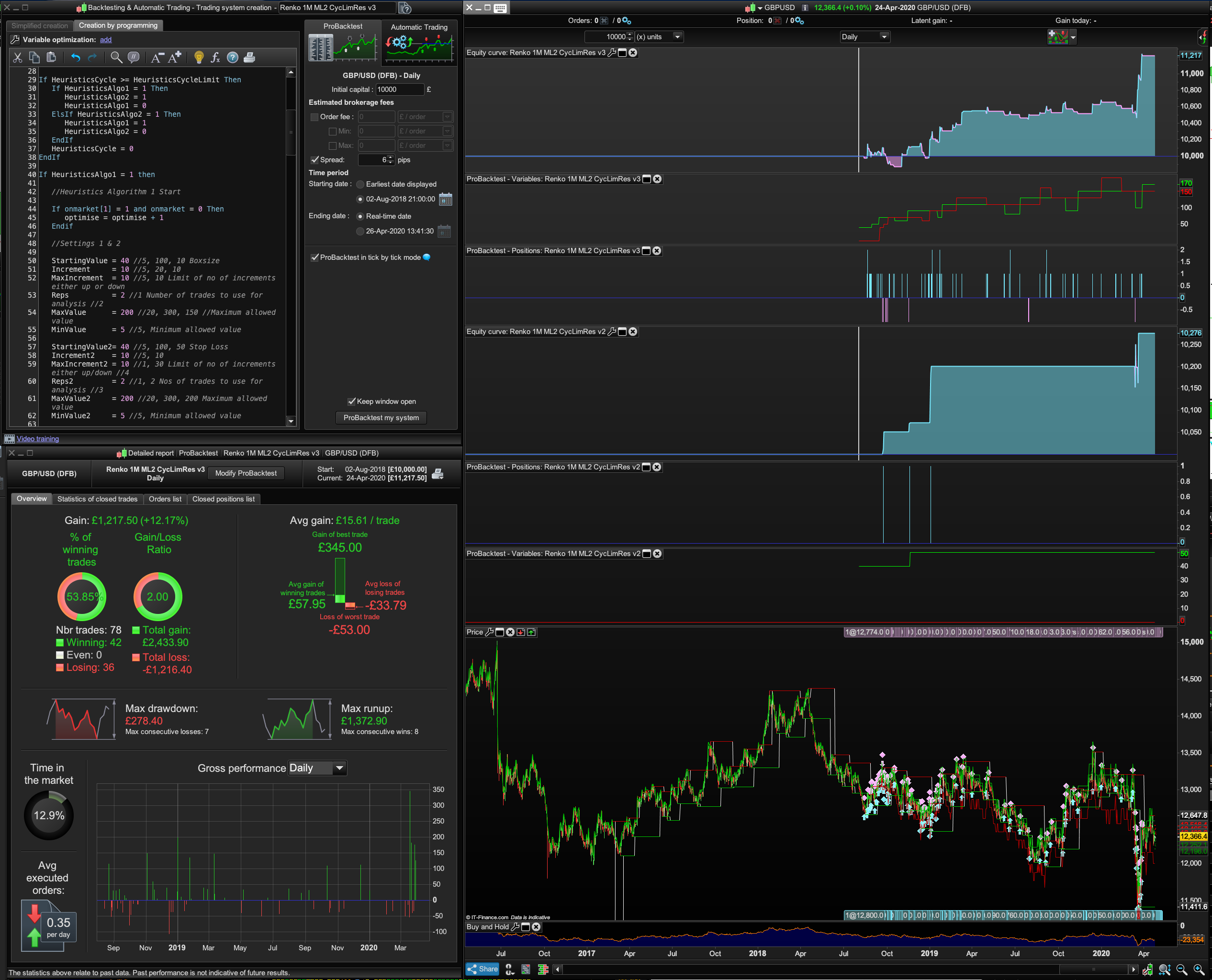

Meanwhile can you please check the logic of your Long/Short BoxSize idea with my very simple entry conditions in Renko ML2 v3 below because the results are good not just on the Dow and £/$ but also on other instruments. I like to think a system is robust if it’s simple and can be applied to other markets

particularly when you don’t have to alter settings to adjust for volatility. Great job.

//-------------------------------------------------------------------------

// Main code : Nneless Renko DJI 1Month v3 Machine Learning (ML2)

//https://www.prorealcode.com/topic/machine-learning-in-proorder/page/3/#post-121130

//-------------------------------------------------------------------------

//https://www.prorealcode.com/topic/why-is-backtesting-so-unreliable/#post-110889

// Definition of code parameters

//DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//defparam preloadbars = 1000

//defparam flatbefore = 080000

//defparam flatafter = 215500

//

//once tradetype = 1 // [1]long&short;[2]long;[3]short

//

//once reenter = 1

//once positionperftype = 1 // [0] reenter always; [1] reenter positionperf < 0

//ctime=time>=080000 and time<180000

n=1

HeuristicsCycleLimit = 2

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 then

//Heuristics Algorithm 1 Start

If onmarket[1] = 1 and onmarket = 0 Then

optimise = optimise + 1

Endif

//Settings 1 & 2

StartingValue = 40 //5, 100, 10 Boxsize

Increment = 10 //5, 20, 10

MaxIncrement = 10 //5, 10 Limit of no of increments either up or down

Reps = 2 //1 Number of trades to use for analysis //2

MaxValue = 200 //20, 300, 150 //Maximum allowed value

MinValue = 5 //5, Minimum allowed value

StartingValue2= 40 //5, 100, 50 Stop Loss

Increment2 = 10 //5, 10

MaxIncrement2 = 10 //1, 30 Limit of no of increments either up/down //4

Reps2 = 2 //1, 2 Nos of trades to use for analysis //3

MaxValue2 = 200 //20, 300, 200 Maximum allowed value

MinValue2 = 5 //5, Minimum allowed value

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Negative Increment Position

once optimise = 0 //Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode1 = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If optimise = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*Close)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode1 = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode1 = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode1 = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode1 = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode1 = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode1 = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode1 = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode1 = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode1 = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

optimise = 0

EndIf

// Heuristics Algorithm 1 End

ElsIf HeuristicsAlgo2 = 1 Then

// Heuristics Algorithm 2 Start

If onmarket[1] = 1 and onmarket = 0 Then

optimise2 = optimise2 + 1

Endif

//Settings 2

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Negative Increment Position

once optimise2 = 0 //Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If optimise2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i2) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i2)*countofposition[i2]*Close)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode2 = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA2

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

optimise2 = 0

EndIf

// Heuristics Algorithm 2 End

Endif

boxSizeL = ValueX

boxSizeS = ValueY

renkoMaxL = ROUND(close / boxSizeL) * boxSizeL

renkoMinL = renkoMaxL - boxSizeL

renkoMaxS = ROUND(close / boxSizeS) * boxSizeS

renkoMinS = renkoMaxS - boxSizeS

IF high > renkoMaxL + boxSizeL THEN

renkoMaxL = renkoMaxL + boxSizeL

renkoMinL = renkoMinL + boxSizeL

endif

if low < renkoMinS - boxSizeS THEN

renkoMaxS = renkoMaxS - boxSizeS

renkoMinS = renkoMinS - boxSizeS

ENDIF

//

//c1 = renkoMaxL + boxSizeL

//c2 = renkoMinS - boxSizeS

// Conditions to enter long positions

//If c1 then

Buy N CONTRACT at renkoMaxL + boxSizeL stop

//EndIf

// Conditions to enter short positions

//If c2 then

Sellshort N CONTRACT at renkoMinS - boxSizeS stop

//EndIf

// Stops and targets

//SET STOP %loss 0.5

Set stop ptrailing 50 //100

SET TARGET PPROFIT 500 //Orig 150 //Best 500

graphonprice renkomaxl + boxsizel coloured(0,200,0) as "renkomax"

graphonprice renkomins - boxsizes coloured(200,0,0) as "renkomin"

GRAPH ValueX coloured(0,255,0)

GRAPH ValueY coloured(255,0,0)

//graphonprice newsl coloured(0,0,255,255) as "trailingstop atr"

Edit: What does adding

once ValueX

= StartingValue etc, do that it wasn’t doing before that code was added? Cheers.