New test, again..:-)

I think may be the values for rep, increment and so on..wasn’t good. So I did a backtest on it !

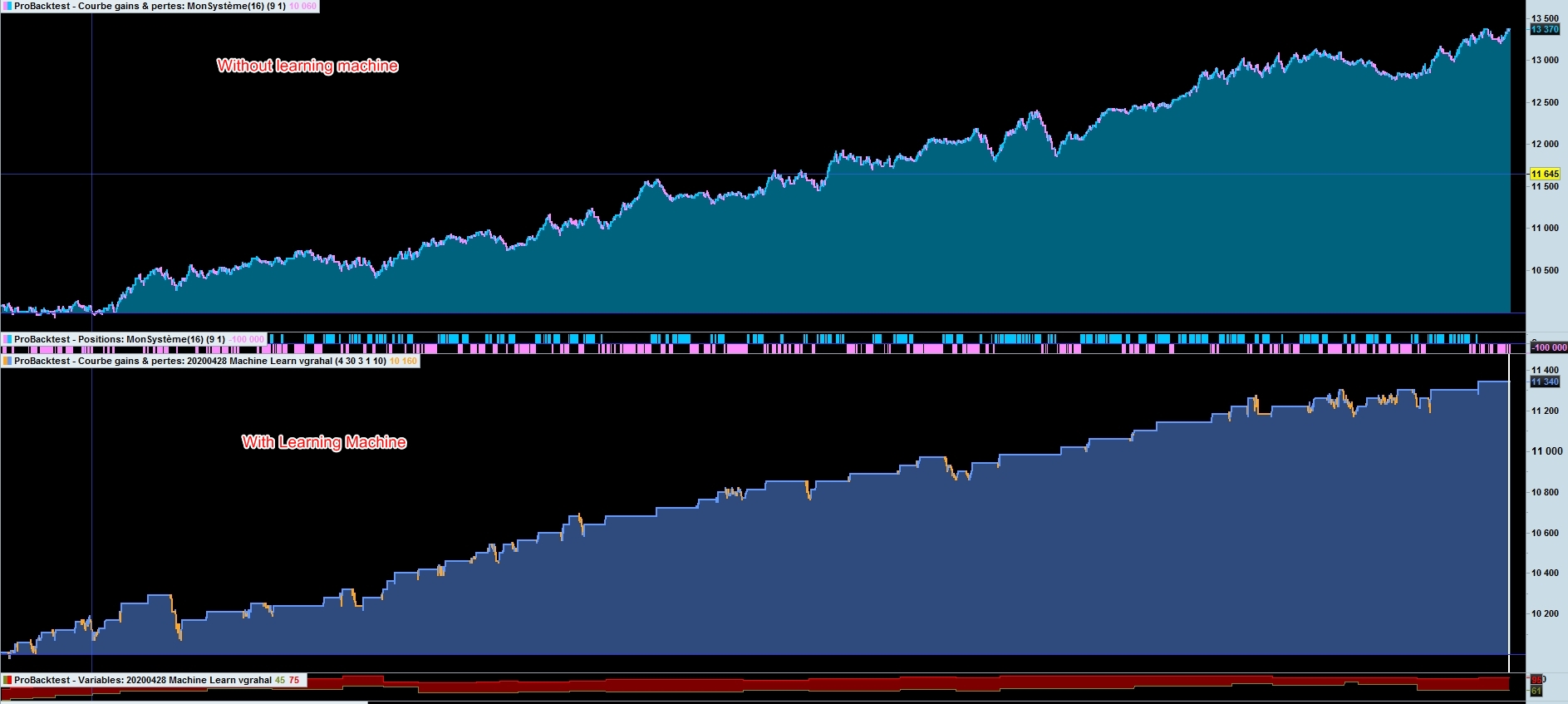

It’s much better, but with a lot less profit than the stupid simple crossing average code. But less trades

Next…

Bard

BardParticipant

Master

That’s a bunch of time wasted. Knew there was something off but not exactly what. At least v4 ts had this covered.

I never look at this as wasted effort, because all the time I’m working on these systems (even with an unrealistic trailing stop), I’m constantly still thinking of new ideas to try out and develop.

Re: Renko ML2 1Month v4 ts (Trailing Stop). That was a such a great idea on coming up with the ML2 Boxsize L/S concept. Really smart, because I’ve been testing/experimenting Boxsize L/S v4 ts against ML1’s for Long and Short boxsizes governed by just ValueX, against ML1’s just for either boxsize or ML1’s on the take profit number and your ML2 Boxsize L/S performs far better.

I wondered though, how does it know if it should use percentage or points for stops, what determines that switch?

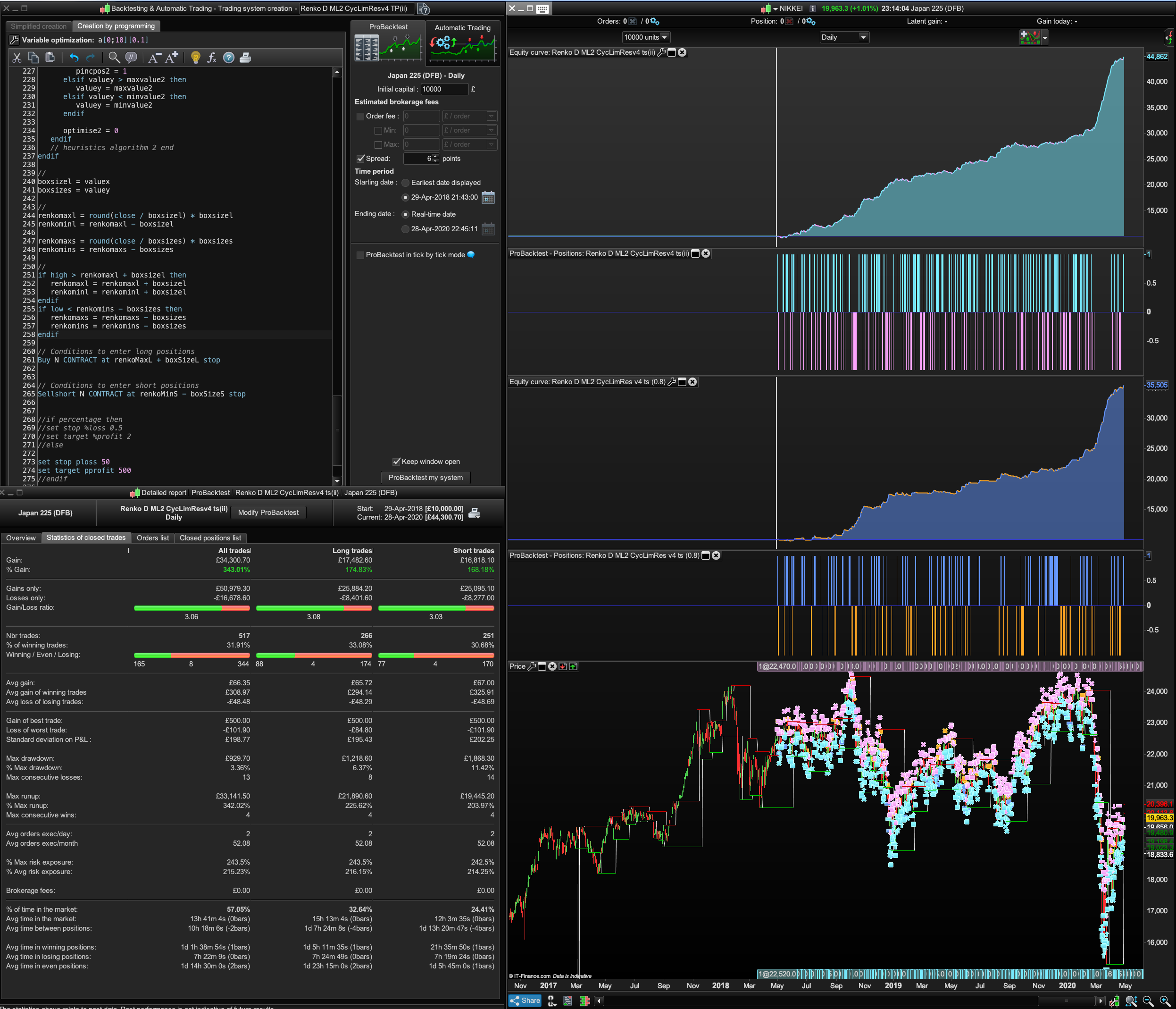

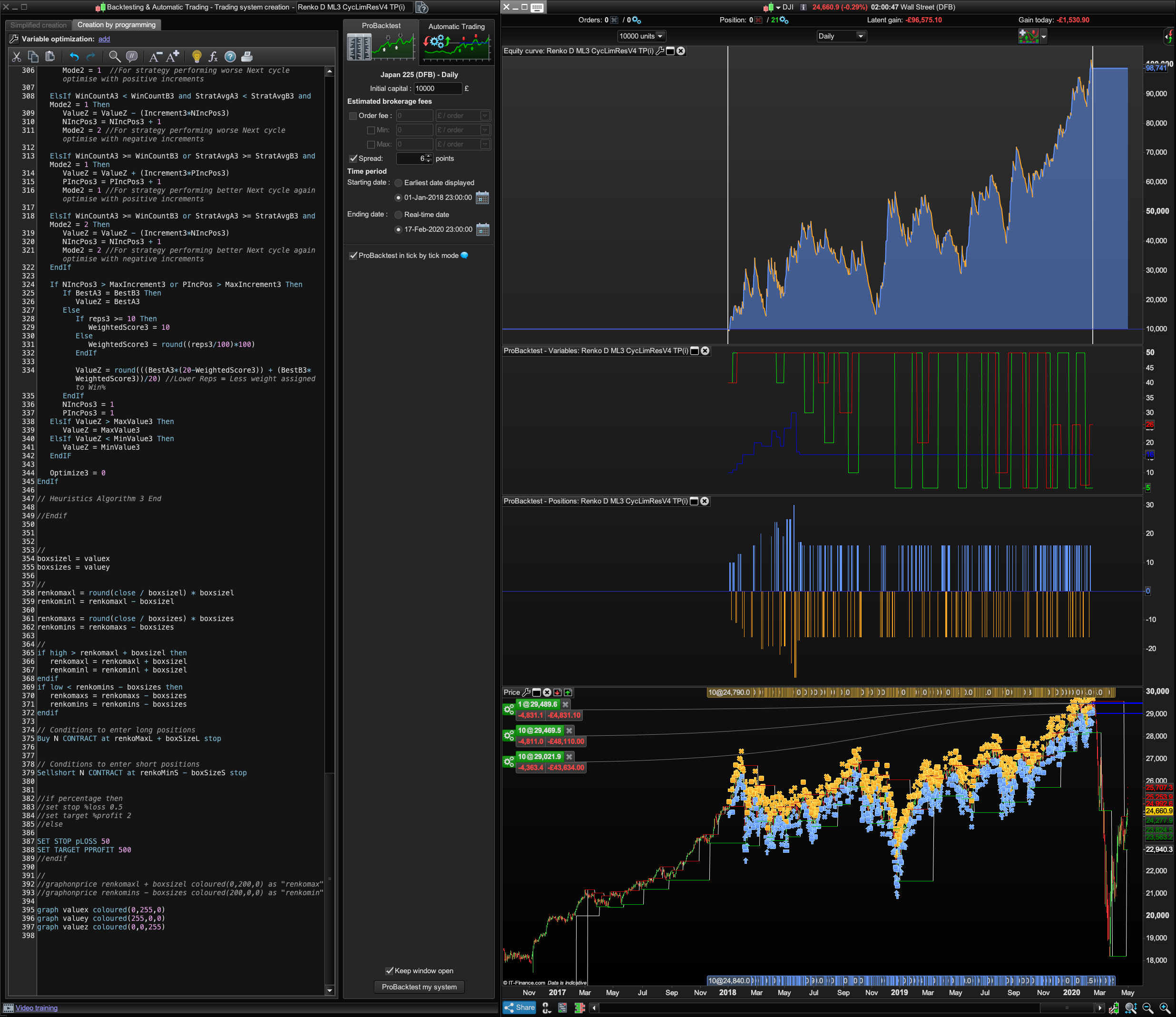

I did play around with the sophisticated ts settings, doing optimisations and manually changing figures. I tried different percentages for ts1, 2 and 3 but couldn’t get profit to vary. My thought is that the system maybe needs to be really allowed to “breath“ and make out like a bandit whenever possible rather than being restricted with a smart plan to tighten the ts when the profits climb to squeeze more profit out of the position. I then replaced the ts code with the standard TP at 500 and the new pLoss at 50 (now that we know trailing stops are pointless with tbt tests) and it performs even better. About another £10k better on the Nikkei Ap2018-2020. Please see image.

Can we trust “pLOSS 50” being respected properly by tbt test though? Seems to be throwing up far less tbt warnings, most of those being triggered by edits to settings 1 & 2.

Tomorrow I am going to see if I can get an ML3 working, so far not, maybe because of the wrong cycle heuristic code. But I noticed with the Ehlers Oscillators with an attempted ML3 system (2 correctly working ML’s and the third not being factored into the profit performance), that it produced better profits when the 3rd albeit not fully working ML3 was added compared to the ML2 version (x for long entry threshold and y for short entry).

Paul

PaulParticipant

Master

I wondered though, how does it know if it should use percentage or points for stops, what determines that switch?

I wasn’t sure what I preferred best, so I added them both to compare quickly. Tend to prefer %.

The v4 ts version came to a loss of 50 points yesterday but before it het +220 points gain. Candles are read when they are done so if using daily timeframe it looks this ts isn’t a good solution to take profit in the same day/candle. A profit target should work though as you said.

now again it tipped +150 for this day.

Can we trust “pLOSS 50” being respected properly by tbt test though?

yes I think so but it can be bigger when there are gaps.

PaulParticipant

Master

@

zilliq hi, do you have any change/improvement on the ML engine we could test out (demo) live? I’ve running code with / without ML and they have the same results. Thanks! ps added pic v4 ts

Hi

@paul

Not sure to understand

You ask if I did a change in the ML code ? If so, the answer is no

I use the simple/stupid strategy and add the ML with 3 trials (With the version of Grahal, yours et the one of Brad)

And as you see, I see no improvement

I reply to your question ?

PaulParticipant

Master

Here’s try on 1 ML engine, choosing from in this case 5 best optimisation results (from without ML). So it means 1 ML engine can have many parameters. On short timeframe, run optimisation a few days later and add that the first 5 and build a database.

Makes it sense? No! Still fun to try.

startingvalue = 1 //5, 100, 10 boxsize

increment = 1 //5, 20, 10

maxincrement = 5 //5, 10 limit of no of increments either up or down

reps = 5 //1 number of trades to use for analysis //2

maxvalue = 5 //20, 300, 150 //maximum allowed value

minvalue = 1 //5, minimum allowed value

//heuristics algorithm 1 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise = optimise + 1

endif

once valuex = startingvalue

once pincpos = 1 //positive increment position

once nincpos = 1 //negative increment position

once optimise = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode1 = 1 //switches between negative and positive increments

//once wincountb = 3 //initialize best win count

//graph wincountb coloured (0,0,0) as "wincountb"

//once stratavgb = 4353 //initialize best avg strategy profit

//graph stratavgb coloured (0,0,0) as "stratavgb"

if optimise = reps then

wincounta = 0 //initialize current win count

stratavga = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i = 1 to reps do

if positionperf(i) > 0 then

wincounta = wincounta + 1 //increment current wincount

endif

stratavga = stratavga + (((positionperf(i)*countofposition[i]*close)*-1)*-1)

next

stratavga = stratavga/reps //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2"

//graph stratavga*-1 as "stratavga"

//once besta = 300

//graph besta coloured (0,0,0) as "besta"

if stratavga >= stratavgb then

stratavgb = stratavga //update best strategy profit

besta = valuex

endif

//once bestb = 300

//graph bestb coloured (0,0,0) as "bestb"

if wincounta >= wincountb then

wincountb = wincounta //update best win count

bestb = valuex

endif

if wincounta > wincountb and stratavga > stratavgb then

mode1 = 0

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 1 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 1 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 2 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 2 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

endif

if nincpos > maxincrement or pincpos > maxincrement then

if besta = bestb then

valuex = besta

else

if reps >= 10 then

weightedscore = 10

else

weightedscore = round((reps/100)*100)

endif

valuex = round(((besta*(20-weightedscore)) + (bestb*weightedscore))/20) //lower reps = less weight assigned to win%

endif

nincpos = 1

pincpos = 1

elsif valuex > maxvalue then

valuex = maxvalue

elsif valuex < minvalue then

valuex = minvalue

endif

optimise = 0

endif

// heuristics algorithm 1 end

if valuex=1 then

boxsizeL=5

boxsizeS=50

elsif valuex=2 then

boxsizeL=15

boxsizeS=40

elsif valuex=3 then

boxsizeL=40

boxsizeS=30

elsif valuex=4 then

boxsizeL=5

boxsizeS=25

elsif valuex=5 then

boxsizeL=10

boxsizeS=45

endif

graph valuex

//graph boxsizel

//graph boxsizes

So it means 1 ML engine can have many parameters

Hahah great idea … you’ve leveraged the ML engine!

Thank You for sharing Paul

PaulParticipant

Master

I reply to your question ?

Yes fully thanks!

@

Bard About the ts on a daily tf. If using mtf, but daily without updateonclose for the % trailingstop, would it be correctly done if onmarket & exited on the same daily bar? Or need the ts to be modified for that? Anyway todays result +500! Who thought a target 500 points would make sense lol! Can take a few losses of 50 points now 🙂

BardParticipant

Master

Excellent idea, re leveraging the ML engine! How would the code be written for Renko ML1 to actually self optimise and try out and step through those 5 values in lines 95 to 110? I can’t picture it.

If using mtf, but daily without updateonclose for the % trailingstop, would it be correctly done if onmarket & exited on the same daily bar? Or need the ts to be modified for that?

Sorry not following, could you explain more please about what you want to try and achieve with the Multi TF and “without updateonclose” and “would it be correctly done if onmarket & exited on the same daily bar?”

If you’re using MTF, which other TF apart from Daily are you referring to?

Kerchinnngggg! €337! Take the ts off and let the system rip!

(It’s the sound of a shop cash register machine when you open it to put money in it, ha ha)

And on the subject of where to turn the ML algo to next: It has to be Money Management and Trade Size!

BardParticipant

Master

Hi

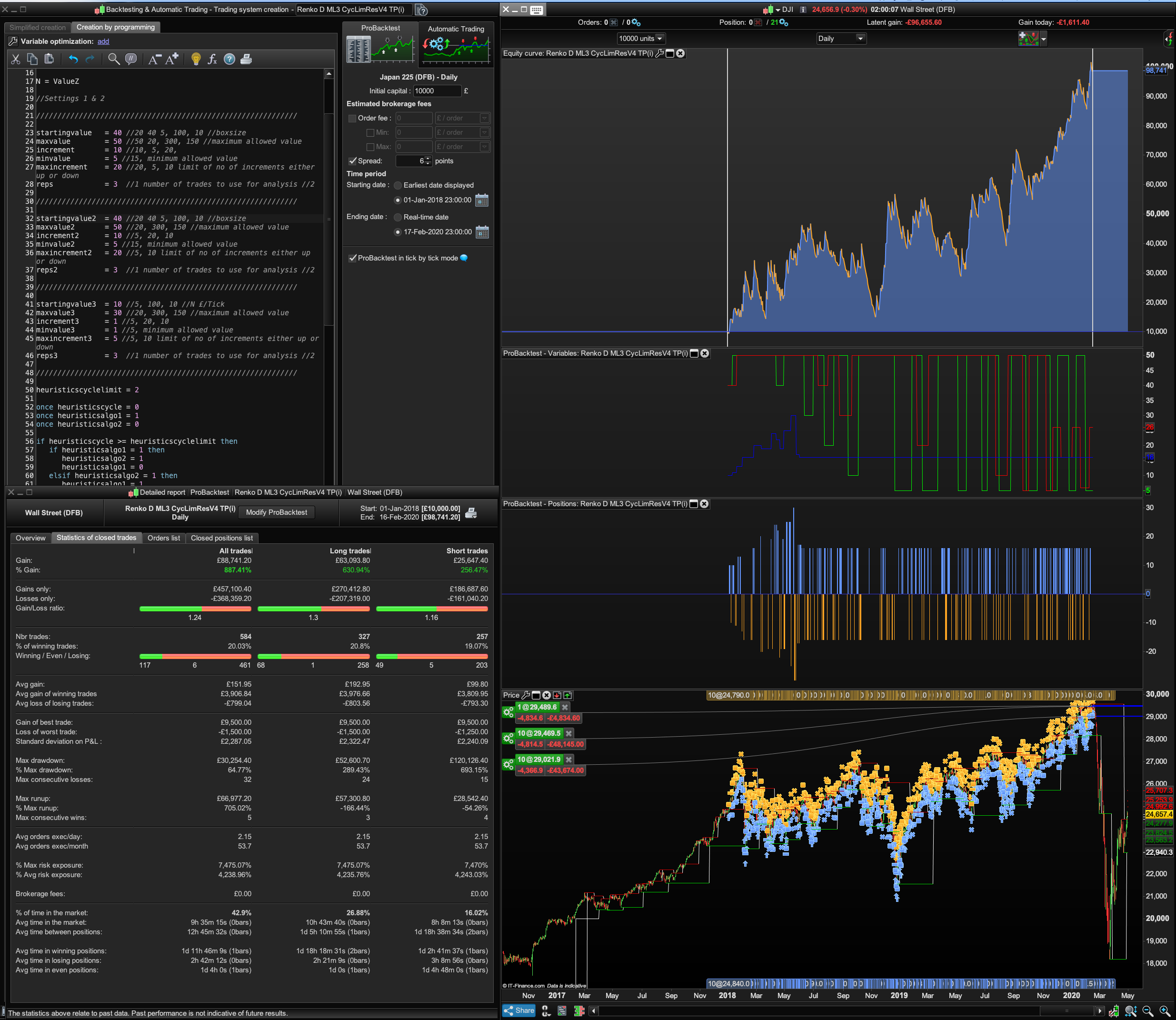

@Paul, or anyone with better coding skills than me, can anyone figure out if this HeuristicsCycle code looks right for an ML3 version?

I cannot get an ML3 version (using algo 3 for £/tick N) to work properly when coded. It’s like the ML2’s v4 without the trailing stop, but with one more part added, i.e., number 3 algo and using the line: elsif heuristicsalgo3 = 1 then… When I use it it does not take any trades?

HeuristicsCycleLimit = 3

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

once HeuristicsAlgo3 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo1 = 0

HeuristicsAlgo2 = 1

HeuristicsAlgo3 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

HeuristicsAlgo3 = 0

ElsIf HeuristicsAlgo3 = 1 Then

HeuristicsAlgo1 = 0

HeuristicsAlgo2 = 0

HeuristicsAlgo3 = 1

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

The only way I can get the Value Z Money Mgt algo = “N” to work (pls see screens and GraphZ blue line) is to use the “HeuristicsCycleLimit = 2” version and then // out the “elsif heuristicsalgo3 = 1 then” line of code. I have had that blue line work to the end to other tests.

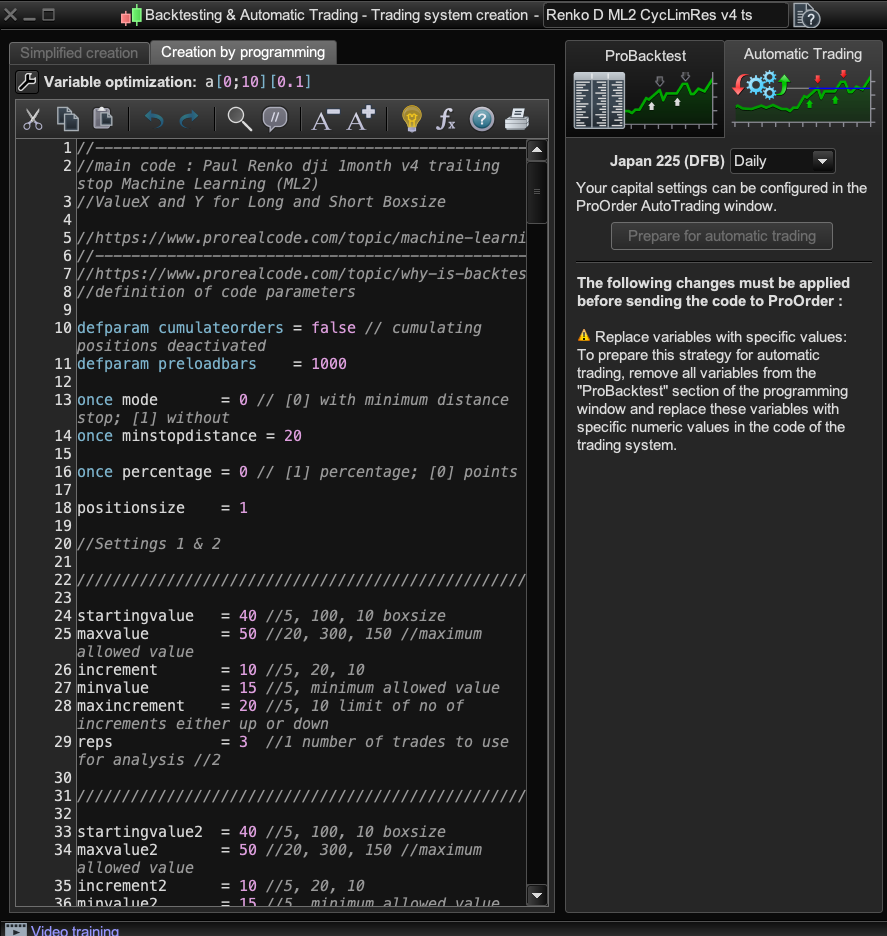

I have tried ValueZ replacing the N’s in the buy code but get an error from PRT asking me to report. Maybe N cannot be ValueZ? I really think though if N can be replaced with ValueZ and we can get the money management ML3 algo coded right the performance will increase. I’ve seen it do £25k in two months using N in the buy code before a tbt warning came on. I’ve attached the “work in progress” Renko ML3 V4 below.

can anyone figure out if this HeuristicsCycle code looks right for an ML3 version?

Try below …

HeuristicsCycleLimit = 3

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

once HeuristicsAlgo3 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo1 = 0

HeuristicsAlgo2 = 1

HeuristicsAlgo3 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 0

HeuristicsAlgo2 = 0

HeuristicsAlgo3 = 1

ElsIf HeuristicsAlgo3 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

HeuristicsAlgo3 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

PaulParticipant

Master

If you’re using MTF, which other TF apart from Daily are you referring to?

it’s daily with updateonclose and daily without updateonclose as a test. The question is how do we get a trailingstop working in 1 daily candle, where then entry & exit are in that same bar? (and without going to lower timeframes).

How would the code be written for Renko ML1 to actually self optimise and try out and step through those 5 values in lines 95 to 110? I can’t picture it.

So those values in those lines 95-110 you put in manually you found in the optimisation sheet. On a 5s timeframe you could daily add 1 or 2. The engine start which valuex which uses that specific boxsize for l&s. If results are good it should stick to it, if not it should take another valuex which has 2 other boxsizes assigned, so it cycles to those 5 or more numbers from valuex. 2ML is better obviously but still I find above interesting.

Good to see work started on ML3. We got ML working in a backtest as graph showed, have you seen a difference trying live with and without 2 ML engines?

PaulParticipant

Master

because using ML and a long & short strategy at the same time, how does the engine know which direction is preforming poorly? There is no reference too long or short win% or average gain, it takes all results into account to change all parameters (ml1 or ml1-2)

Does that mean focussing a strategy on long specifically and another on short is better?

PaulParticipant

Master

and last one, using 1 ML engine with increments of 5, code of juanj on p1 or p2.

it start out at correct 15 up to 50, but when there’s a drop it ends op with 23 which is not with factor 5 and after that everything is off.

startingvalue = 20 //5, 100, 10 boxsize

ResetPeriod = 1 //Specify no of months after which to reset optimization

increment = 5 //5, 20, 10

maxincrement = 5 //5, 10 limit of no of increments either up or down

reps = 2 //1 number of trades to use for analysis //2

maxvalue = 50 //20, 300, 150 //maximum allowed value

minvalue = 15 //5, minimum allowed value

BardParticipant

Master

The question is how do we get a trailing stop working in 1 daily candle, where then entry & exit are in that same bar?

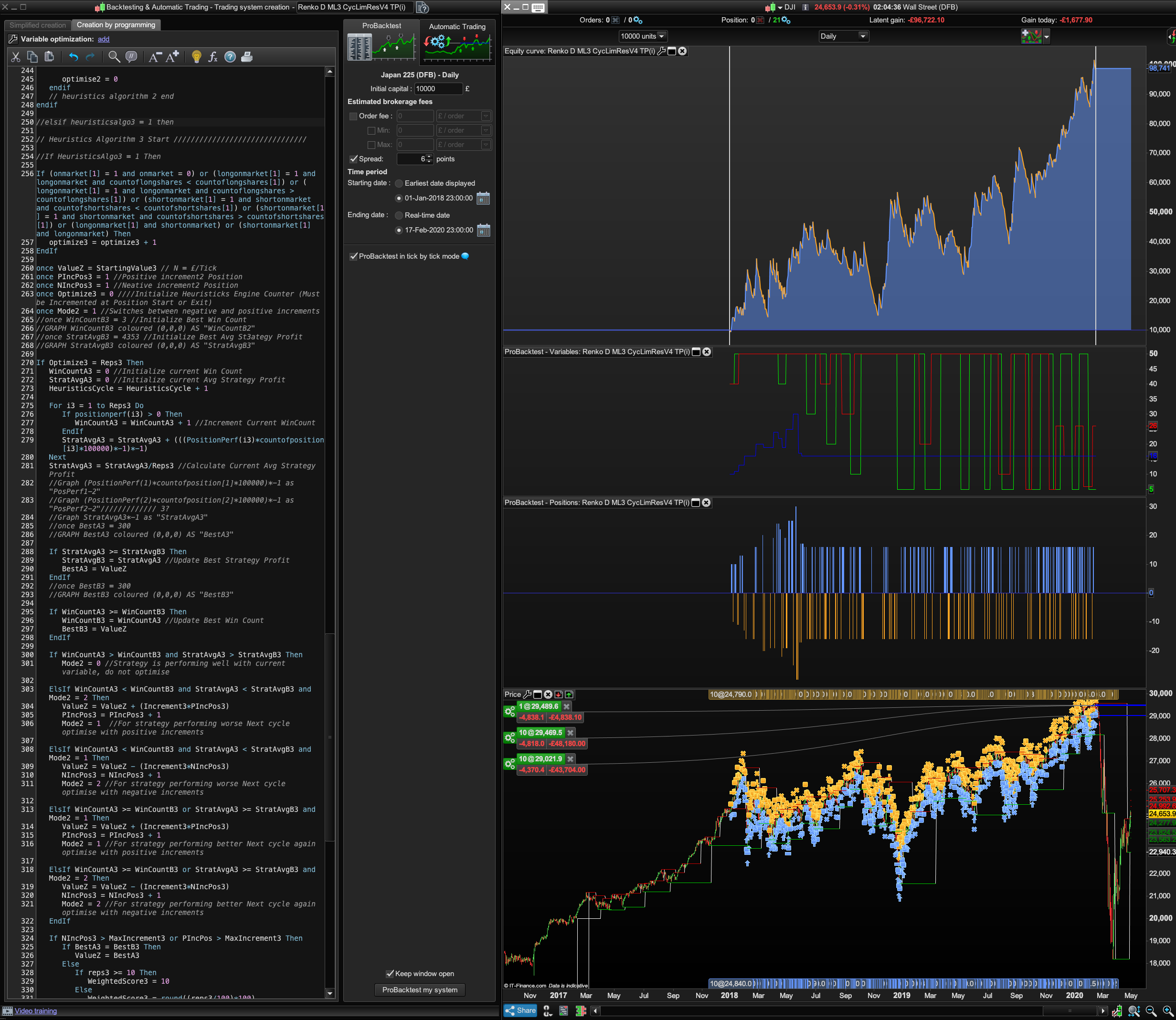

Do we want to try and “fix” the issue with trailing stops and tbt tests though? I’m seeing better results with the pLoss=50 and TP=500. Just inadvertently tried a ML3 v4 on a 4 hour timeframe when I was testing something else but the old equity backtest was up from last nights work using incomplete functioning ML3 code:

“ML3 kind of works but it’s not optimising with ML1 and ML2.”

optimise2 = 0

endif

// heuristics algorithm 2 end

endif

//elsif heuristicsalgo3 = 1 then

// Heuristics Algorithm 3 Start ///////////////////////////////

//If HeuristicsAlgo3 = 1 Then

If (onmarket[1] = 1 and onmarket = 0) etc etc

and look at the performance before the PRT engine finds issue with a candle and throws a “warning spanner into the works,” fortunately late into the test. I hit “close” instead of relaunch because it preserves the test up to the point of failure. The blue GraphZ (because ValueZ has replaced N in the Buy line) is working on its own. Independent of profit from the ML1 and ML2 performance comparisons. 17% Ddown.

I wonder what would happen with your great idea to have value 1 to 5 classifiers of the best box sizes? Maybe post you results? There is definitely and edge here

with position sizing ML algos.

have you seen a difference trying live with and without 2 ML engines?

No Paul because I can’t launch the ML systems on my Demo. Did you get this “can’t go live” warning with your v4 ts? (pls see image 2). How can I launch it on the Demo? It doesn’t like ValueX/Y?

Does that mean focussing a strategy on long specifically and another on short is better?

That would make sense! Run the two systems together… The number of permutations for this ML code is mind boggling! 😃