Hi all. Ive been thinking that i would LOVE to see the live results from other coders here!

Im all for sharing bits and pieces of code, to work on ideas. At the same time i absolutely understand that ppl dosnt wanna share their most profitable and finished code, cus it takes a lot of work and its kind of ur own baby.

That being said, i would love to see some numbers for ur most profitable Out of sample results!

How is your algo working (trendfollowing/mean reverting) and for what market and timeframe?

And screenshot the results for out of sample period please!

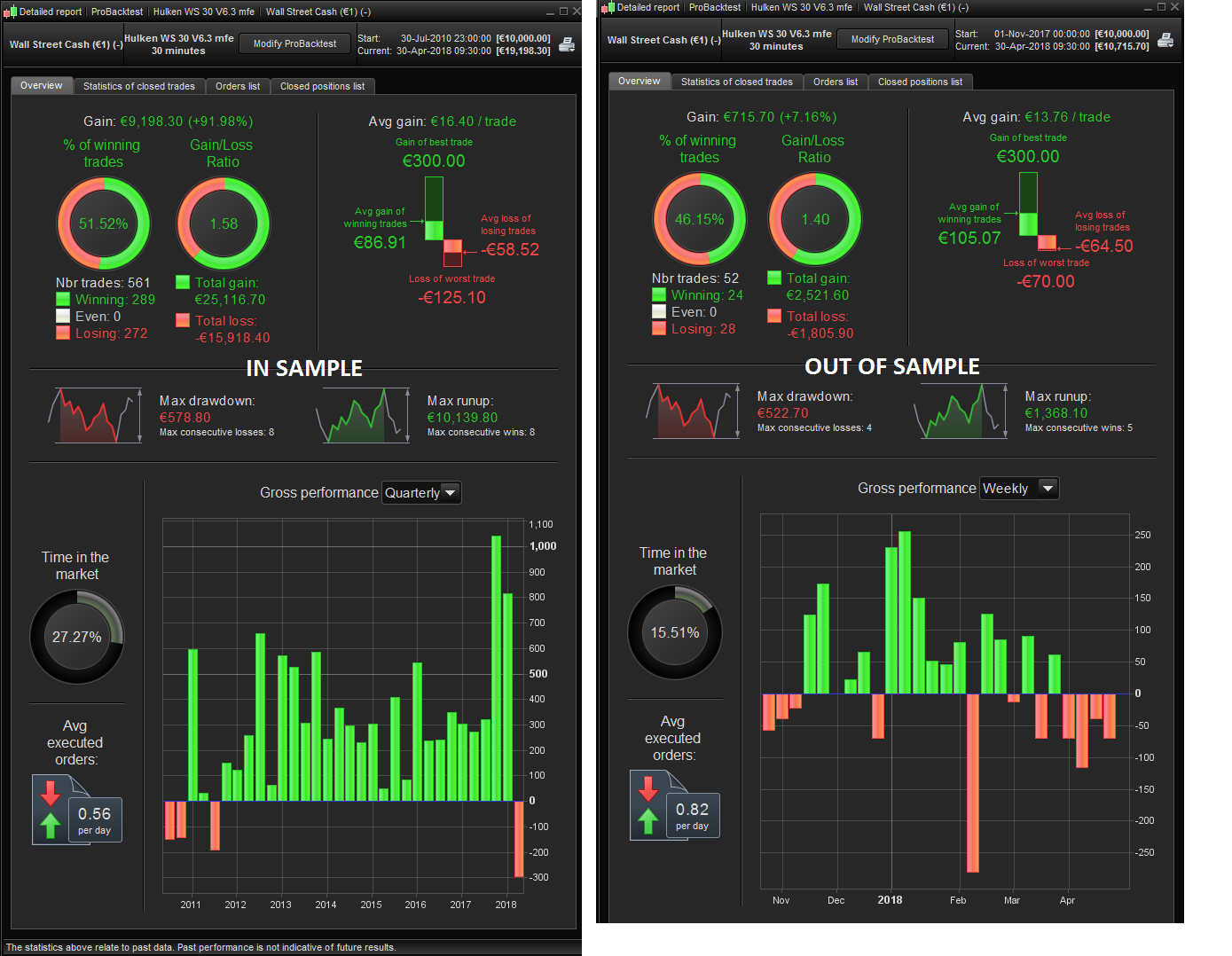

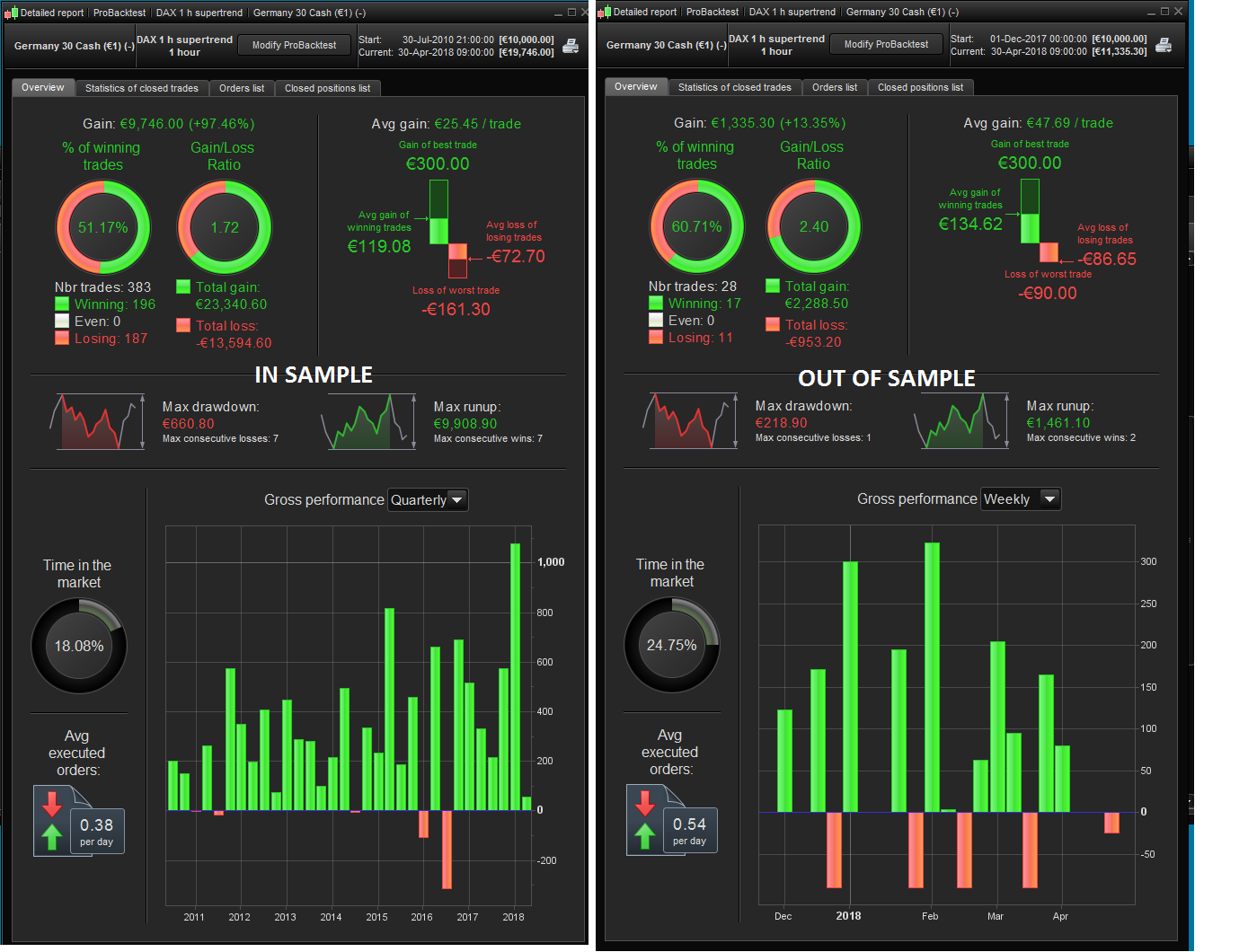

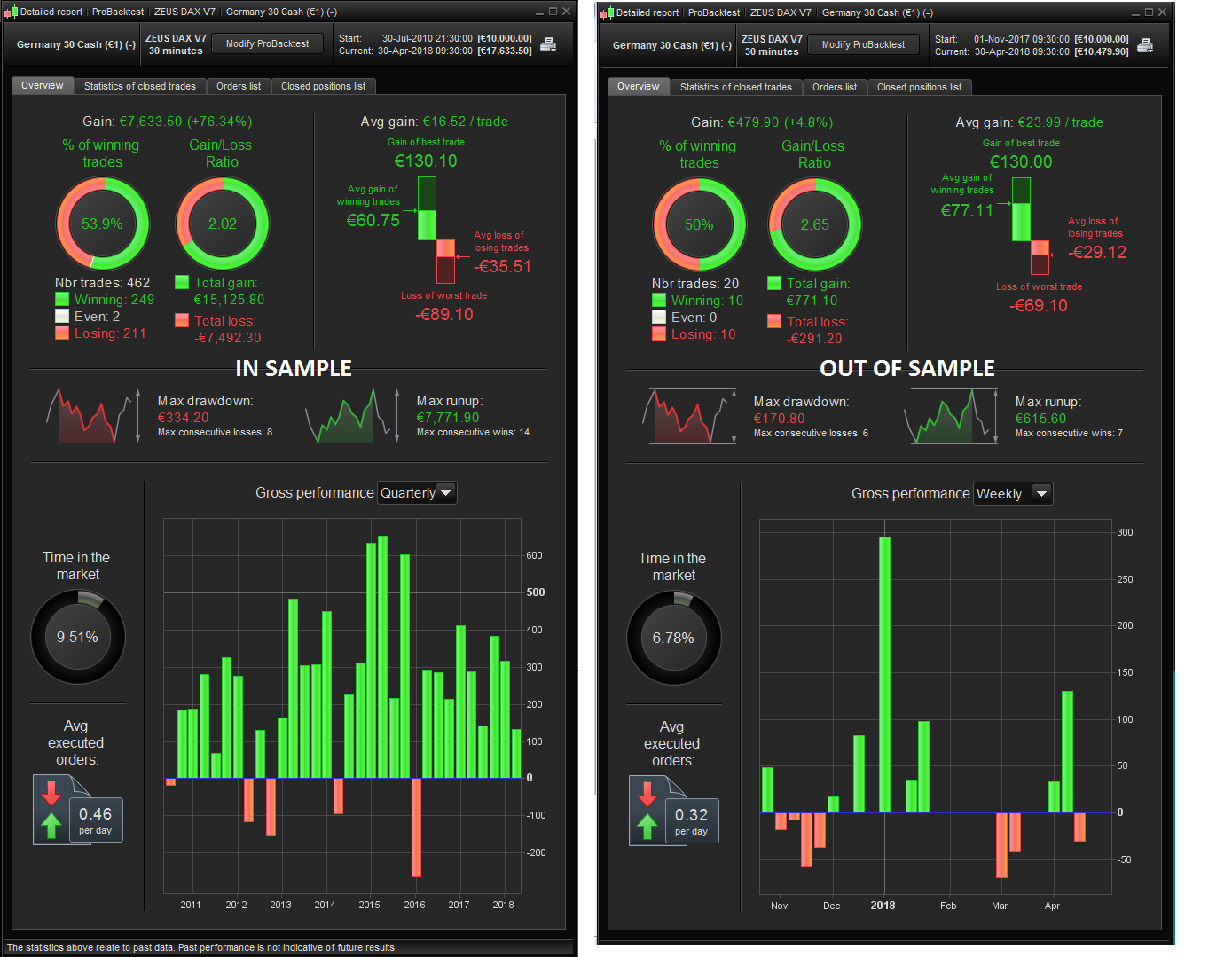

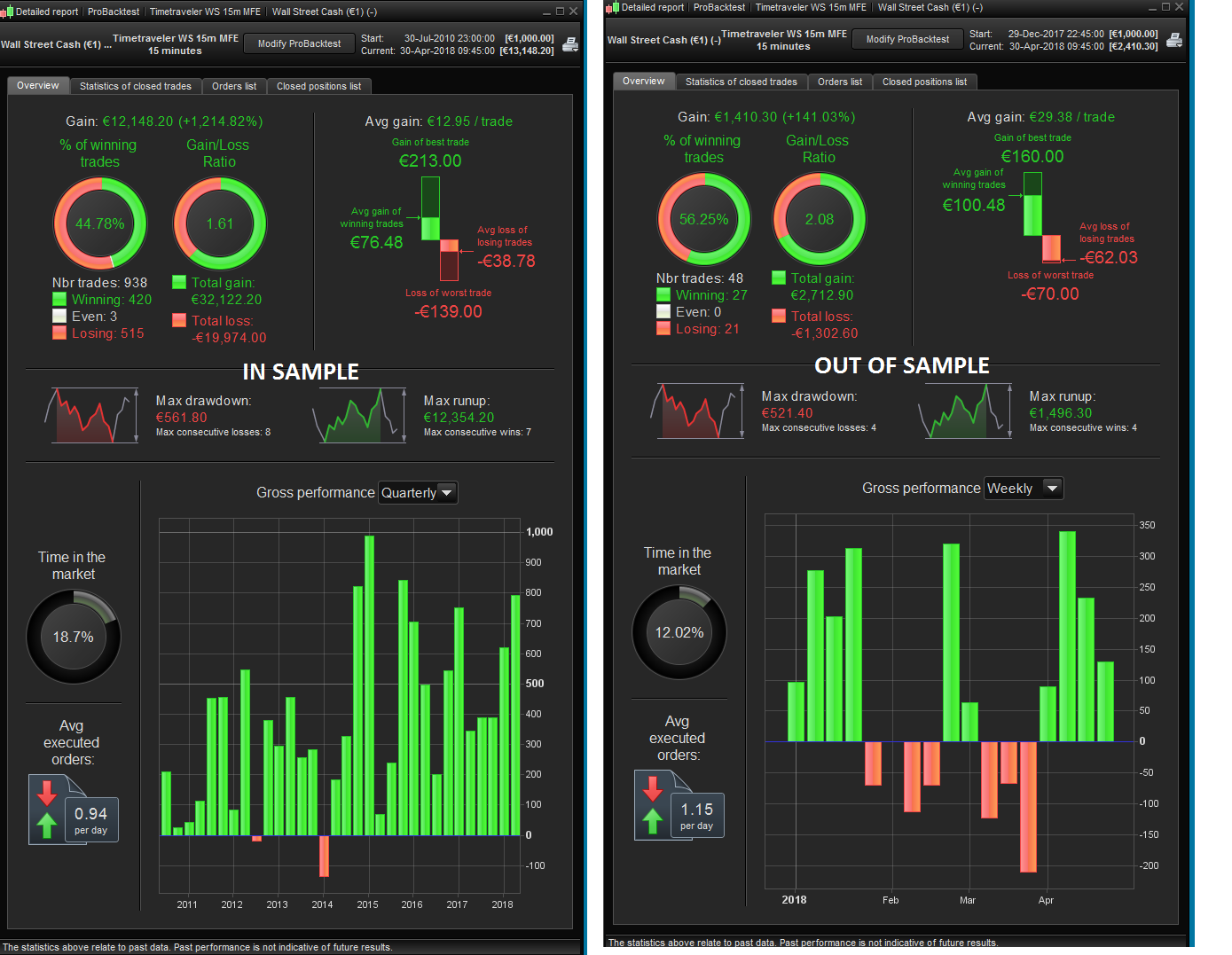

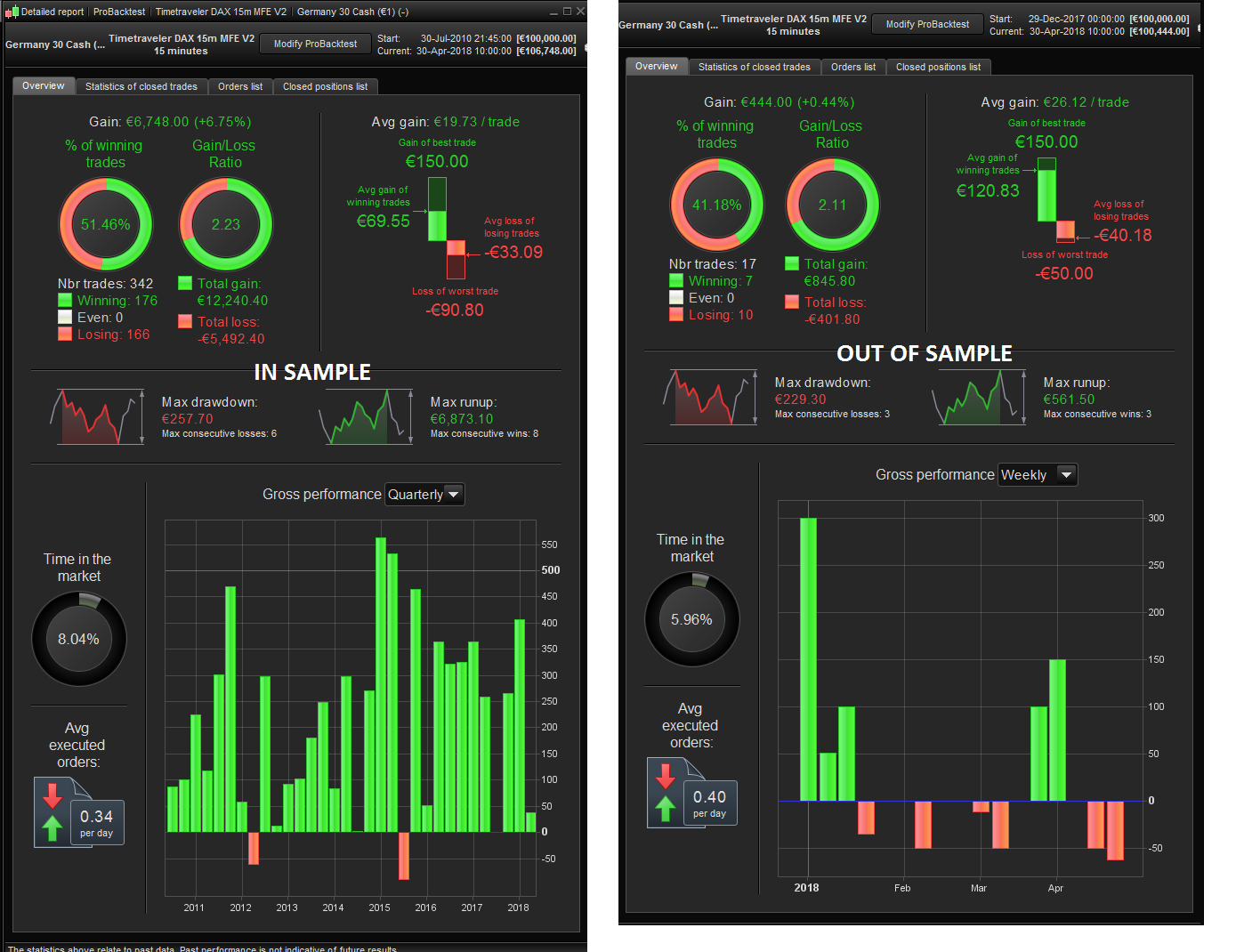

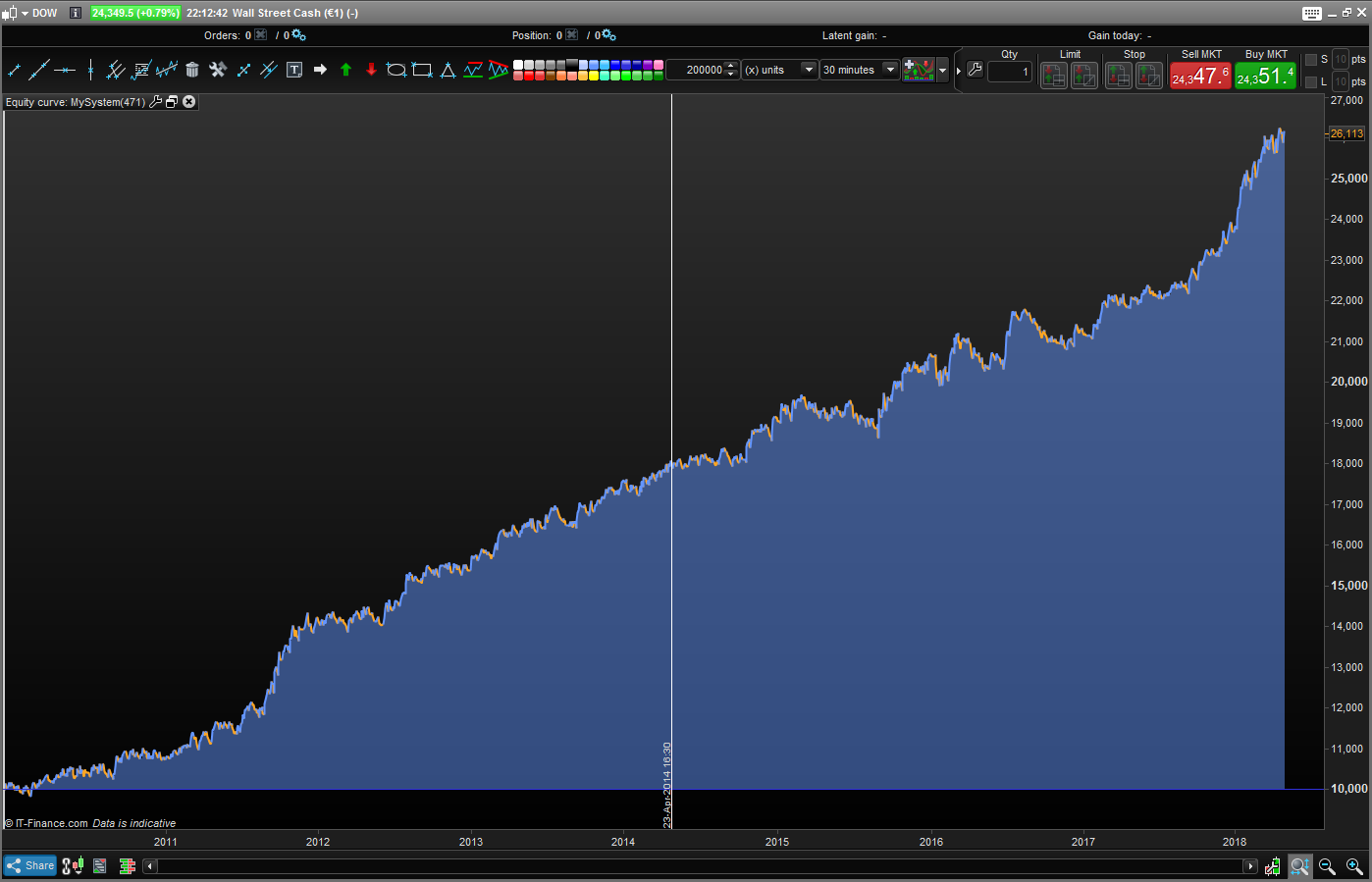

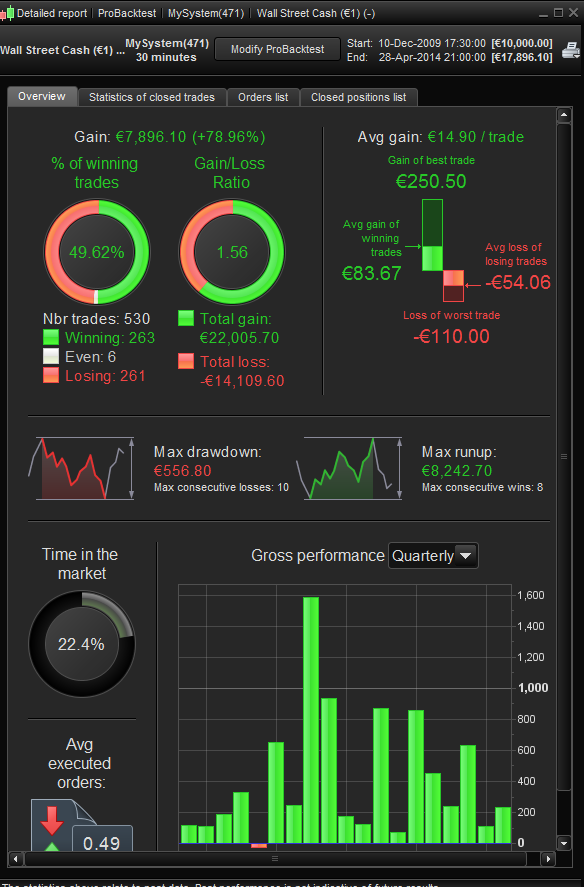

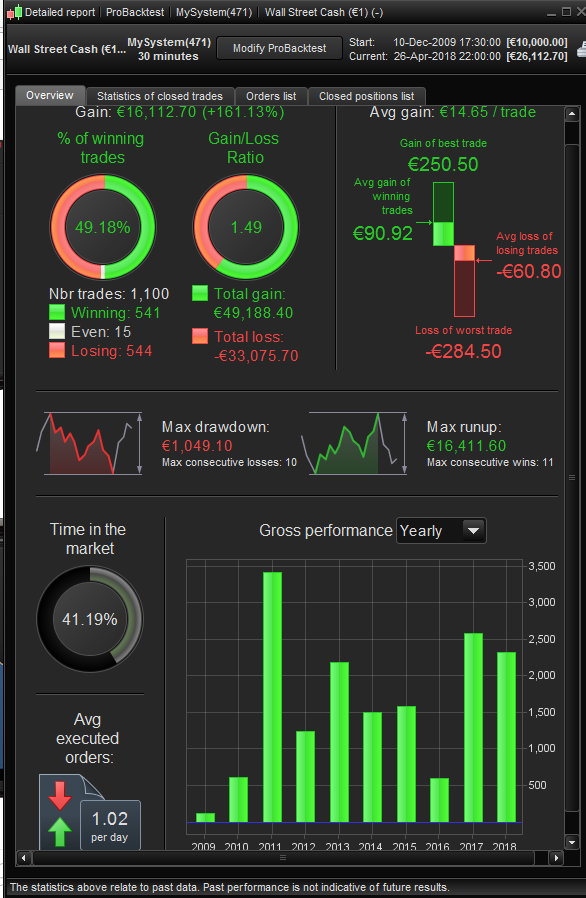

Im gonna add 5 / 8 of my profitable out of sample + in sample results! All pics are with 1* 1€ contract, and spread is added. All photos are tick by tick backtested.

(pls note that my “IN SAMPLE” photo has included the “out of sample period” (aka its just backtest from earliest possible date -> today. The out of sample pic is live results only.)

All my algos are Long only and trend following. Atm they are way too correlated.. im working on mean reverting and shorting algos but they are alot harder to code imo 😀

Ill answer questions as long as i dont think its too revealing 😉

Edit: i wish that 2018 wouldve been alot better but god damn the drop in february and volatility after has been rough 😀 Tho i am profitable in 7/8 of all my live strategies!

All the systems are running LIVE live…

but the screenshots are from backtest because i have started/stopped a few of them, also updated the stop loss / trailing stop here and there and therefore had to restart the code.

Edit: Just to be 100% clear: The “out of sample” screenshots here are from BACKTEST only, but i have been running them live more or less since the “out of sample date” shown in the photo. I can confirm that profits have been good and similar to backtest/out of sample photos 🙂

Edit2: Yes i could have used “in sample” photos without the “out of sample” time lol i didnt think about that until i posted the photos, but all of them have 400+ trades so u can imagine just taking out the last Quarter/few months and the results are pretty much the same numbers. If u rly want i can make a photo of just the in sample period.

Edit3: I feel like i dont have enough “out of sample” data just yet to really compare the 2 🙂 Would like about 100 trades / 1 year worth of data! But so far it looks promising, considering how the markets (ws/dax/nq) looks from february

Yes I was just thinking how – if go forward with this – we might need to have a standard test period between submissions … as you say, 3 months / 1 year / 100 trades / whatever?

Just a few thoughts

GraHal

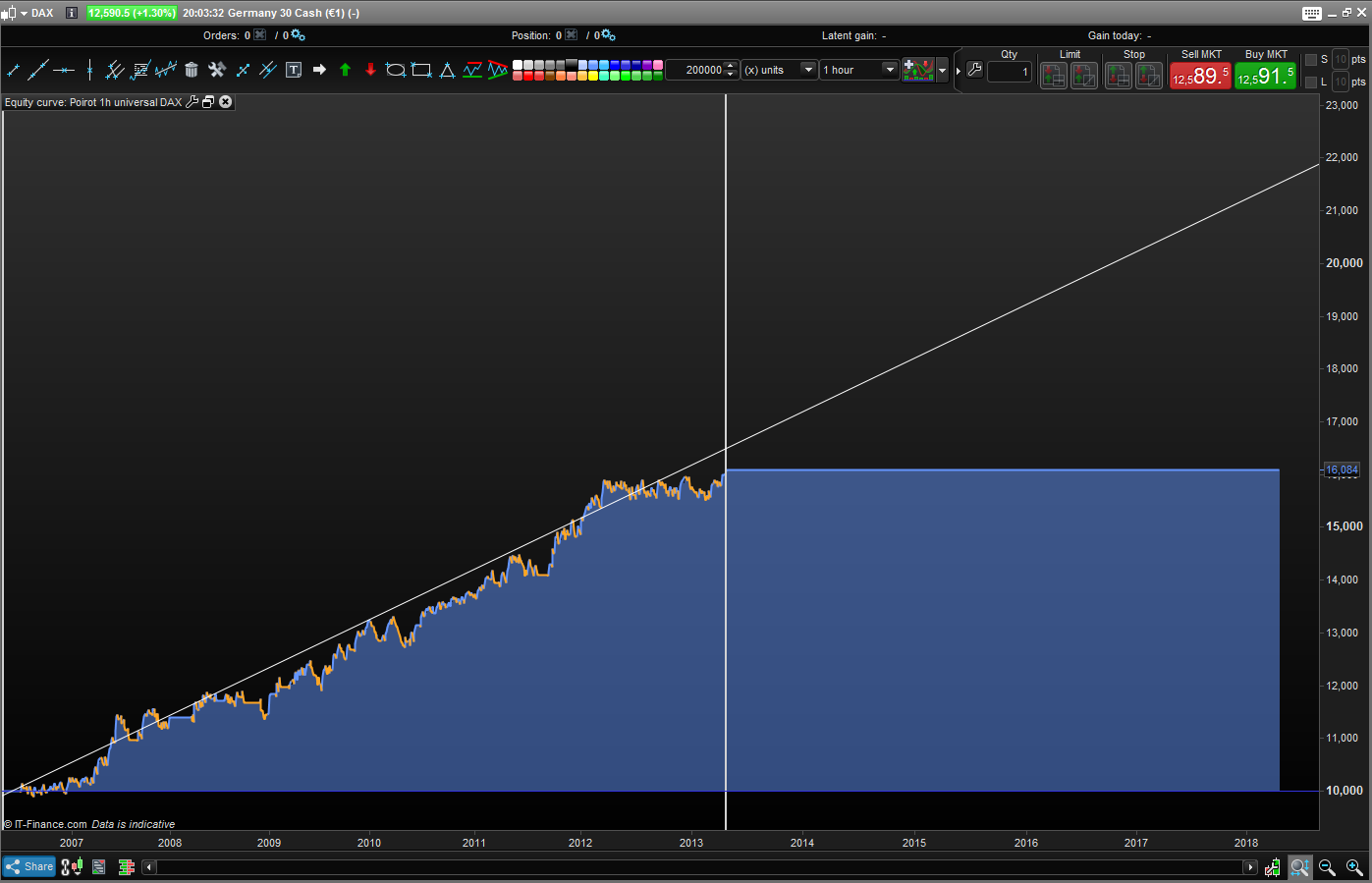

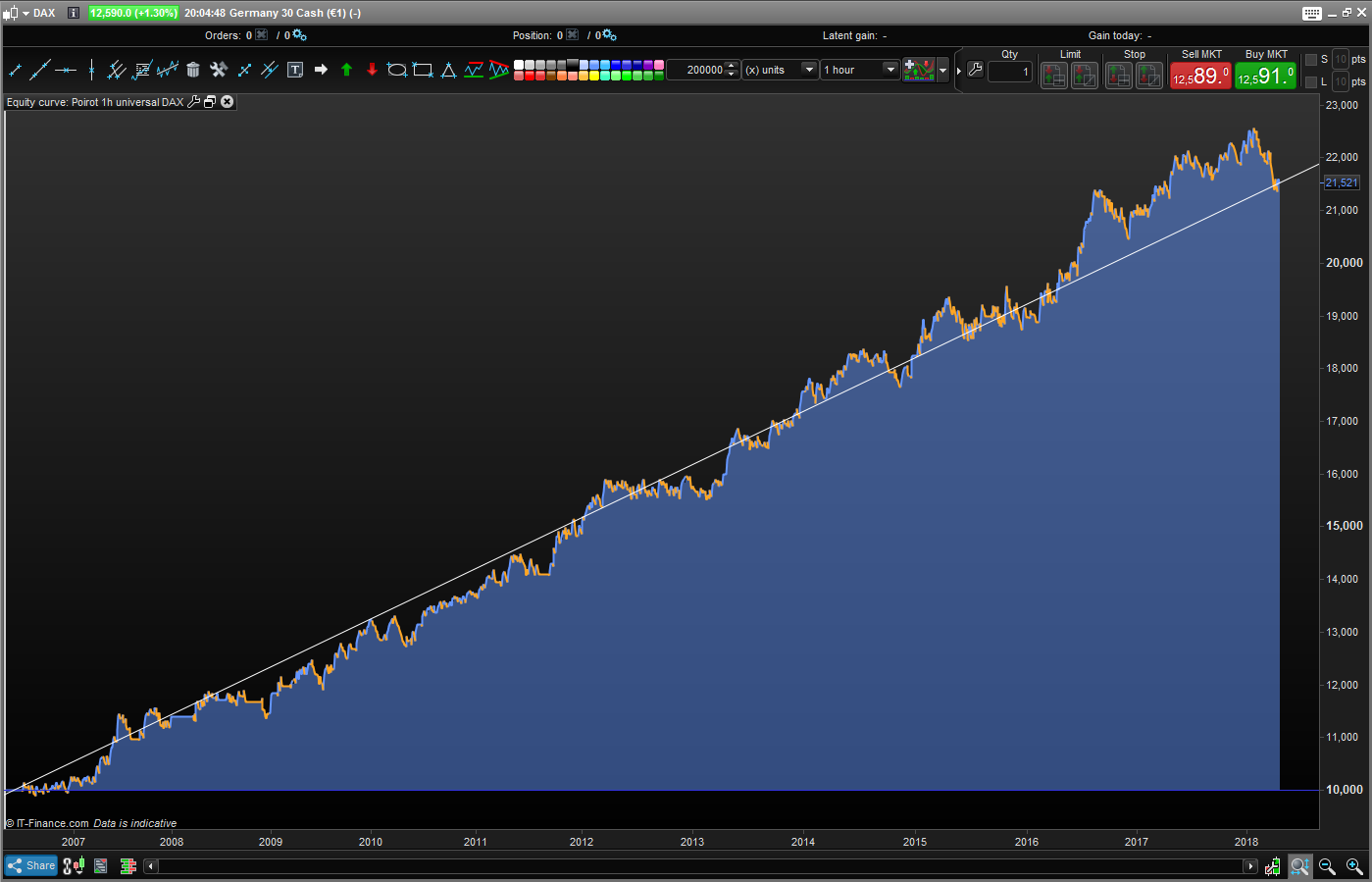

Btw just to show an example of how i work/create algos.

Following is 2 photos, 1 where i have chosen the first 50% of the data and started optimizing, then the second image is the same algo but backtested over the 100% of all the data after i have optimized on the first 50%..

In other posts i have gone thru my way of creating systems, simply put its:

1. Make ur algo on 100% of the data (dont change 1 single variable at all. If your idea is “Buy when price crosses over supertrend and sell when crosses under supertrend” then this is your entire algo with no optimization.)

2. use only 30-50% of the data for optimizing the algo, optimize everything from stops/targets/trailing stops/variables..

3. go back to 100% of the data to check for overfitting.

As u can see from the Poirot pictures included, the first half is a lot smoother and not as choppy as the second half. This is because the first half is optimized, so my variables have been tuned to fit it “as perfect as possible” while the other half just have the same variables to go after and of course is less smooth then because the “same data” will obviously not occur in the future, but SIMILAR data might come..

Edit: @GraHal The more data the better it is imo 🙂

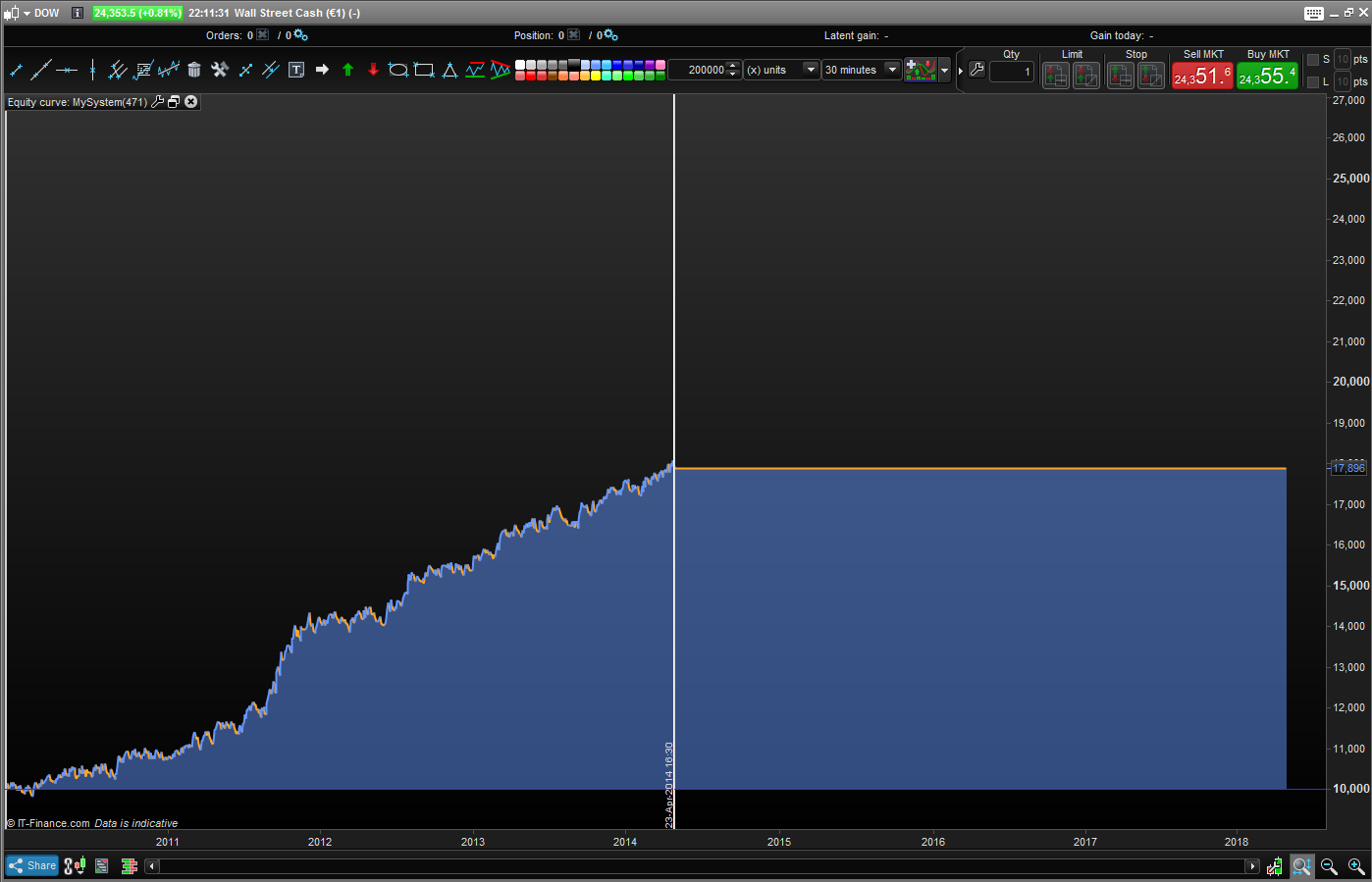

Edit2: Ill add another strategy thats currently in demo, same thinking here, optimized on 50% of the data, then backtested on 100% of the data on picture 2, notice the difference in smoothness of the EQ curve, but all in all “similar results”. Added photos of the results also (not sure if spread is added in this one tbh.)

Sorry for double posting but missed chance to edit in this: Notice on the last “Stats half + stats full” photo that OUT OF SAMPLE 50% of the last data includes a drawdown x2 that of the “in sample”

This is obviously not “crazy” or “shouldnt be happening” this is exactly whats GOING to happen sooner or later when a model/system/algo meets new and fresh data it has never seen and never been optimized for!

Edit: @GraHal The more data the better it is imo

Yeah, maybe I meant to say … as a minimum 3 months / 1 year / 100 trades / whatever?

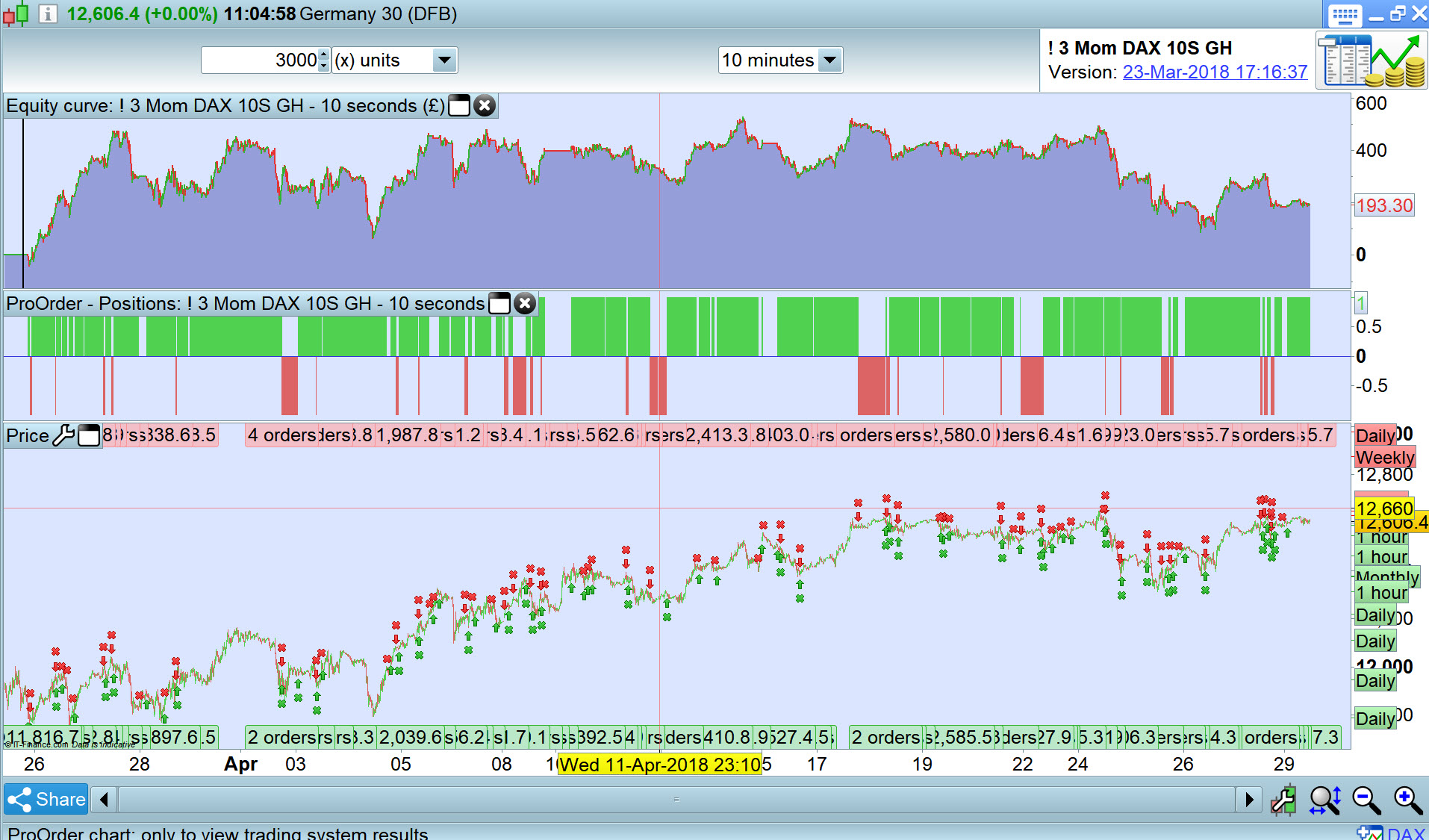

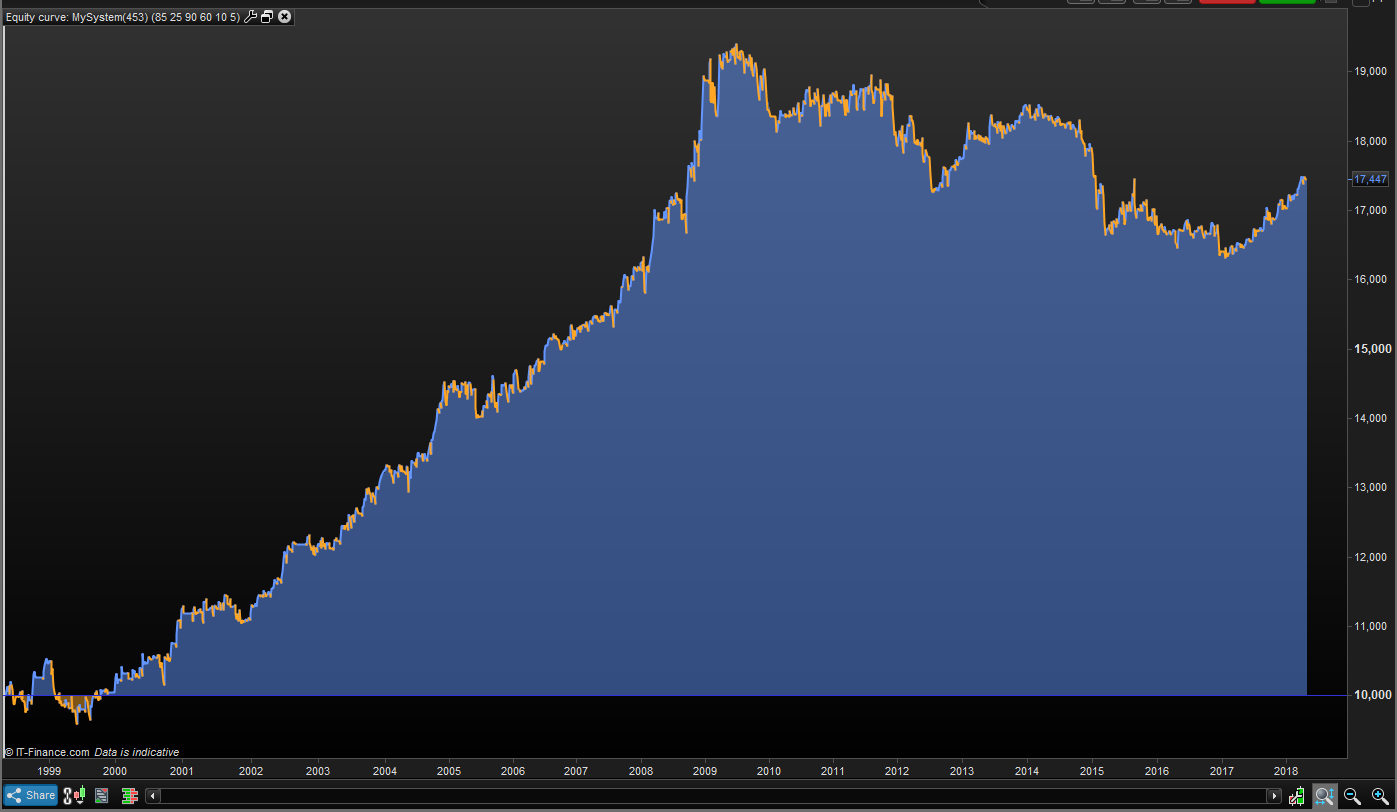

Attached a 10 second TF which has been running Live on Demo since 23 March with 101 trades completed.

The equity curve is shown on a 10 min TF to get all the equity curve in a single screen shot.

Happy to share if anybody fancies improving etc?

GraHal

Good post! And what creative names you have for your algos. 😉

I work similarly although I do not develop the algo first on all data and then optimize on only a part. I develop completely on say 50-70% of the data and when I’m all done then I test the remaining data OOS. I think using all data to build does introduce look-ahead bias even if you don’t change any variable.

Good post! And what creative names you have for your algos.

I work similarly although I do not develop the algo first on all data and then optimize on only a part. I develop completely on say 50-70% of the data and when I’m all done then I test the remaining data OOS. I think using all data to build does introduce look-ahead bias even if you don’t change any variable.

Haha thanks Despair!

I understand what u mean about the “look ahead bias” – But honestly it wouldnt matter if i started with 50% or 100%, if i where to use the exact same strategy with the exact same values, if its profitable for 50% and 100%, it dosnt matter, as long as i dont start optimizing/changing values on 100% of the data.

i Could have used ONLY the 30%/50% data and not “checked the 100%” to see how/if its profitable on 100% of the data, before optimizing. But it wouldnt matter if i checked it or not, because the results wouldve been the same.

Please correct me if im wrong!! 🙂

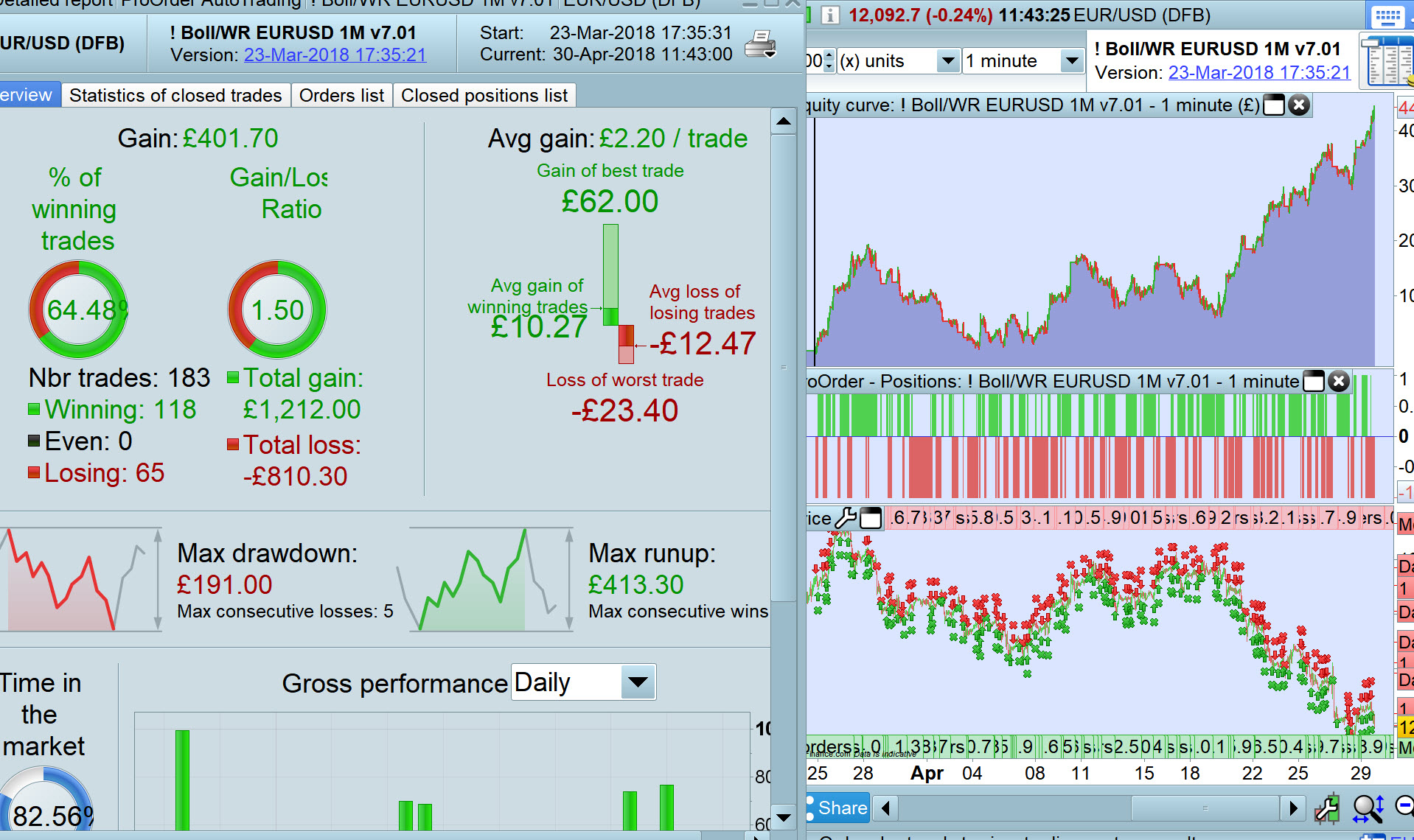

Here’s another on Live Demo on 1 min TF with 183 trades.

Interesting Grahal! 183 trades in 1 month?! Thats crazy! How long have u been doing this and how many live strategies to u have?

How long do u guys run things in demo b4 going live? My algos are so “simple” that if i see that its doing what its suppose to do for 1-2 months, i run it live.

Edit: Honestly, if i had the capital i would just push shit right into live.. I would have made alot more money then i wouldve lost, so far..

Edit2: I wouldve run it thru a week or 2 just to spot errors in code or something disturbing.. But my algos are all pretty much “if thers alot of good momentum coming in, go into trade and pray to god” 🙂 Nothing fancy and no 200 lines of code..

Please correct me if im wrong!!

I think you are correct as you are (presumably) building your System using all default values for the variables?

But what about any parameter levels (correct term?) … how do you decide what value to use when building System on 100% of data?

Please correct me if im wrong!!

I think you are correct as you are (presumably) building your System using all default values for the variables?

But what about any parameter levels (correct term?) … how do you decide what value to use when building System on 100% of data?

Okay so lets say i want to make a simple strategy, using moving averages and bollinger cus why not..

I would use standard 2 std and 20period bollinger + the moving average i think would be best. From just looking at the chart i would decide on the values that i would like to use for my theory/strategy. Let say moving average 20 and moving average 40.

I would use those to create my strategy, and if i like what i see i start using 30-50% of the data (Maybe data from the middle part, or the end, or the start..) and i optimize on that data only. Then i just check the 100% data again and if its curvefitted (happened MANY times ofc..) the strategy would just go to shits when looking at anything outside the curve-fitted data… Ill include a picture of a strategy i curvefitted, in case someone would like to see what im talking bout.

Edit: i always leave the last years as out of sample.. whole 2016+2017+2018 is usually always left out.

Edit2: After i check my strategy and i start optimizing on 30-50% i NEVER EVER change the strategy. I will optimize the variable, but i will never add indicators/other stuff to the code (only exceptions are “what time to trade” or “sell on fridays” or trailing stop loss) but i will never add like “average true range > XX” or something like that. If its not in the code when i start optimizing, its a completely new code.

Edit3: If the strategy looks like the one in the picture, i throw it away 10/10 times. I will never start to re-optimize or add stuff to make it better… When i optimize its do or die-. Either its good and i run it in demo then live, or its shit and i discard it.

Honestly, if i had the capital i would just push shit right into live.. I would have made alot more money then i wouldve lost, so far..

Yeah I do push shit right into live (well not shit, but Systems that backtest good!) but I did then monitor every trade closely (NOT, what is it – press play and go away? 🙂 ).

I have gone through a bad patch (on manual trading) and so I have re-evaluated my whole way of working, tidied up my Platform (and my wife’s! 🙂 ) and I plan to go forward using Auto-Systems … with hopefully no manual trades … through the summer at least! 🙂

A big part of my major review is I have been too intense on it all for over 2 years and the rest of my life has largely stood still! I feel like I’m doing drug at times 🙂 and I can’t stop, but I am weaning myself off it all slowly!

I have a penchant for short TFs (hence the 10 sec and 1 min results above) I guess as that is how I trade manual on PRT.

GraHal

Honestly, if i had the capital i would just push shit right into live.. I would have made alot more money then i wouldve lost, so far..

Yeah I do push shit right into live (well not shit, but Systems that backtest good!) but I did then monitor every trade closely (NOT, what is it – press play and go away? ).

I have gone through a bad patch (on manual trading) and so I have re-evaluated my whole way of working, tidied up my Platform (and my wife’s! ) and I plan to go forward using Auto-Systems … with hopefully no manual trades … through the summer at least!

A big part of my major review is I have been too intense on it all for over 2 years and the rest of my life has largely stood still! I feel like I’m doing drug at times and I can’t stop, but I am weaning myself off it all slowly!

I have a penchant for short TFs (hence the 10 sec and 1 min results above) I guess as that is how I trade manual on PRT.

GraHal

Hehe im sure u remember my “Thoughts on profitable trading” or what i called that “post for noobs”.. I couldnt trade manually cus i was/am a horrible trader 😀 I dont have the calmness to do manual trades.. its horrible but my stomach twists and turns on every trade. and somehow i 9/10 times buy at the top and sell at the bottom manually 😀 And ive manually stopped systems from trading on just the WORST possible timings 😀 Honestly ive managed to stop a system at the bottom of a drawdown, watched it “paper-trade” lots of profits, started the system again just in time for another drawdown 😀 Suddenly im looking at 2x drawdowns with no profits in between lol

press play and stay away is now my daily motto lol. If i ever think about stopping systems again i just think about all the profits ive missed out on cus of it.

Edit: From all the books ive read and podcasts ive listened to ive realised 3 major things:

1. There is no 1 holy grail system/timeframe/market. Diversification is key.

2. If you dont have a rigid, robust system that you follow 100% of the time, ur gonna fuck urself more then u shouldve in the long run. Because every time u press “buy/sell” manually, ur gonna have feelings regarding that trade, regardless of how the setup is. Your gonna be very hyped and stoked, or very scared when taking the trade, and thats gonna fuck u up sooner or later (unless ur a trader-god lol) So if u start algo-trading then u remove all of those feelings. The only feeling u should have when doing this (in my opinion) is Confidence – that is gonna help u “press play and stay away” and thats gonna help you make money in the long run and follow ur systems no matter what. Compared to what MIGHT happen if u started to do manual trades.

3. The only way to be confident in your systems is by creating them in a very robust matter, doing everything u can do to reduce the chance of overfitting.