Bonjour,

Voici ma nouvelle stratégie pour le CAC40 (FRANCE40 chez IG) sur 1 minute et étudiée sur 10 000 bougies car je ne souhaite pas intégrer la période du COVID car la volatilité était forte. Je pense qu’il faut réactuliser les variables gains et stoploss tous les 10 000 bougies. Mon but est de faire beaucoup de trades avec des gains raisonnables et des pertes raisonnables. J’ai utilisé la supertrend intégrée à prorealtime en multiframe, peut-être faudrait-il la remplacer par la formule de calcul de l’angle et de la pente ?? Si il y a des passionnés de programmation qui peuvent améliorer ma stratégie, ce serait sympa. Je suis dispo pour toute question.

REM PARAMETRES

defparam cumulateorders=false

//defparam flatbefore=082900

defparam preloadbars=10000

Defparam flatafter=215900

timeframe(1 minute)

n=3

IF time<083000 or time>211000 then

journee=0

else

journee=1

endif

REM GAINS

gain=highest[32]-lowest[27]

gain2=highest[1]-lowest[1]

IF time>163000 or time<070000 then

gain2=10

gain=15

endif

REM PERTES

if time>163000 OR TIME<083000 then

set stop loss 20

else

set stop loss 36

endif

REM TENDANCES EN 12 MINUTES CROISEE AVEC 1 MINUTE

timeframe (12 minute)

if Supertrend[2,1]<close or supertrend[4,1]>close or close[100]<close[53] then

mont2=1

else

mont2=0

endif

if shortonmarket and (tradeprice-close)<0 then

mont2=0

endif

if Supertrend[1,1]>close or supertrend[2,1]>close or close[15]>close then

desc2=1

else

desc2=0

endif

timeframe (1 minute)

if Supertrend[4,7]<close or supertrend[19,2]<close or ((close[120]-close)>80) then

mont=1

else

mont=0

endif

if shortonmarket and (tradeprice-close)<0 then

mont=0

endif

if Supertrend[19,2]>close or supertrend[16,3]>close or ((close-close[380])>145) then

desc=1

else

desc=0

endif

REM STOCHASTIQUE TIME SERIES

p=20

q=2

plusHaut = HIGHEST[p](HIGH)

plusBas = LOWEST[p](LOW)

oscillateur = (CLOSE - plusBas) / (plusHaut - plusBas) * 100

K = AVERAGE[q,6](oscillateur)

REM CALCUL NB BOUGIES MEME COULEUR

u=9

w=8

descente=0

for z=1 to u do

if open[z]>close[z] then

descente=descente+1

endif

next

if descente>=w then

stopvente=0

else

stopvente=1

endif

t=11

v=10

montee=0

for y=1 to T do

if open[y]<close[y] then

montee=montee+1

endif

next

if montee>=V then

stopachat=0

else

stopachat=1

endif

REM CALCUL DE LA CLOTURE

ecartclot=(time+63000)/166.66

cloturehier=close[ecartclot]

rem INTERDICTIONS MATHEMATIQUES

IF K[1]<-10 or stopvente=0 or (close[720]-close)>60 or (close[85]-close)>28 or (Average[15](close)-close[2]>8) or close<(dopen(0)-69) or close<(cloturehier-36) then

stopv=1

else

stopv=0

endif

if (close-lowest[40])>80 OR K[1]>95 or stopachat=0 OR (close-close[720])>168 or (close-close[77])>52 or (close[3]-Average[18](close)>6) or close>(dlow(0)+80) or close>(cloturehier+81) then

stopa=1

else

stopa=0

endif

REM INTERDICTIONS TEMPORELLES

if (time>073000 and time<082000) or (time>112000 and time<123000) or (time>150000 and time<153000) or (time>162500 and time<180000) then

stoptimea=1

else

stoptimea=0

endif

if (time>100000 and time<110000) or (time>121500 and time<131500) or (time>153000 and time<163000) or (time>083500 and time<091500) or (dayofweek=1 and time<120000) OR TIME<083000 OR time>200000 then

stoptimev=1

else

stoptimev=0

endif

REM ACHAT

IF open[2]<close[2] and mont=1 and mont2=1 and JOURNEE=1 and stopa=0 and stoptimea=0 and acha=1 then

buy n share at market

set target profit gain

lastorder=0

endif

REM VENTE

if not onmarket and open[2]>close[2] and open[1]>close[1] and desc=1 and journee=1 and vent=1 and desc2=1 and stopv=0 and stoptimev=0 then

sellshort n share at market

set target profit gain2

lastorder=1

endif

REM CLOTURE SI CHANGEMENT DE TENDANCE

if longonmarket and desc=1 and journee=1 and stopv=0 and stoptimev=0 and vent=1 and desc2=1 and (barindex-tradeindex)>1 and (close-tradeprice)>0 then

sell at market

lastorder=1

endif

if shortonmarket and mont=1 and mont2=1 and stopa=0 and journee=1 and stoptimea=0 and acha=1 and (barindex-tradeindex)>1 and (tradeprice-close)>0 then

exitshort at market

lastorder=0

endif

if mont=1 and mont2=1 and journee=1 and stopa=0 and shortonmarket and (tradeprice-close)>1 then

exitshort at market

lastorder=0

endif

if desc=1 and desc2=1 and longonmarket and (close-tradeprice)>1 then

sell at market

endif

REM CLOTURE POUR GAIN RAPIDE

if longonmarket and (barindex-tradeindex)<3 and (close-tradeprice)>8 then

sell at market

endif

if shortonmarket and (barindex-tradeindex)<3 and (tradeprice-close)>8 then

exitshort at market

endif

IF longonmarket and (barindex-tradeindex)>146 and (close-tradeprice)>0 then

sell at market

endif

if shortonmarket and (barindex-tradeindex)>80 and (tradeprice-close)>0 then

exitshort at market

endif

REM INTERDICTION DU MEME ORDRE SI TROP ELOIGNE

if (close-tradeprice)>34 and lastorder=0 then

acha=0

else

acha=1

endif

if (tradeprice-close)>7 and lastorder=1 then

vent=0

else

vent=1

endif

REM CLOTURE ANTICIPEE

if longonmarket and (close-tradeprice)>6 and (barindex-tradeindex)<4 then

sell at market

endif

if shortonmarket and (tradeprice-close)>4 and (barindex-tradeindex)<=1 then

exitshort at market

endif

if shortonmarket and (tradeprice-close)>13 and (barindex-tradeindex)>46 then

exitshort at market

endif

if longonmarket and (close-tradeprice)>1 and (barindex-tradeindex)>138 then

sell at market

endif

if longonmarket and (close-tradeprice)>-1 and (barindex-tradeindex)>92 then

sell at market

endif

if shortonmarket and (tradeprice-close)>-5 and (barindex-tradeindex)>80 then

exitshort at market

endif

Je précise que le résultat obtenu est avec :

-1- un créneau horaire d’Angleterre à H+1 (actuellement H+2 en France), donc 16h30 dans mon code veut dire 17h30 en France

Il faut donc soit que vous rajoutiez 1 heure au code soit que vous mettiez votre plateforme en heure britannique

-2- 1000€ de capital suffisent car je ne joue que 3 mini contrats ne demandant que 750 € de couverture environ

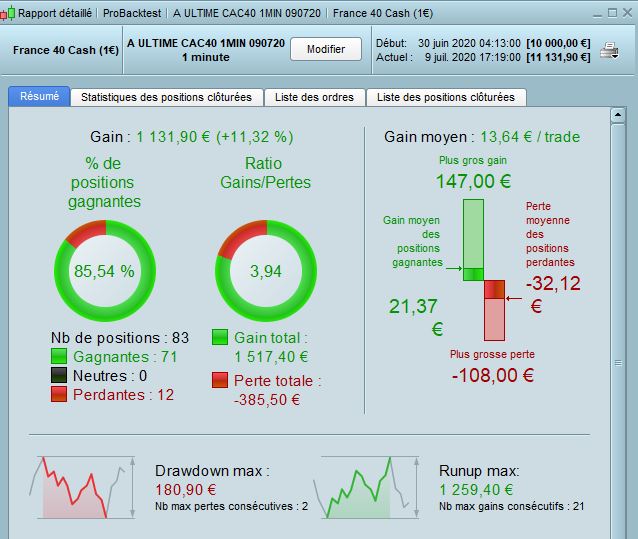

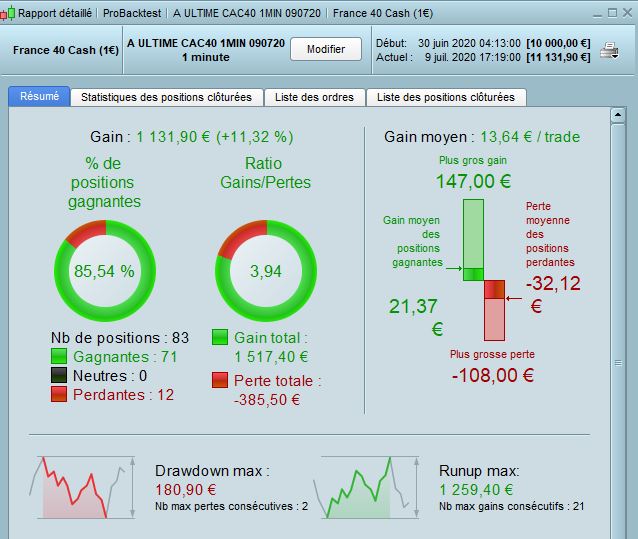

Ci-joint performance du jour au 10/07/2020 avec 1000 € de capital en début de backtest

Il est possible d’ajouter des filtres de volatilité pour éviter les trades durant une période comme celle du corona.

Tu pourras avoir une stratégie testable sur une horizon plus longue et plus représentatives du marché.

Surtout qu’en ce moment les marchés sont encore bien différent de la période pérenne de fin 2019/début 2020.

Peut on utiliser cette stratégie pour trader le gold ?

Bonjour, non c’est une stratégie de trader sur le cac 40, qui suit un peu le Dow Jones mais je ne pense pas que l’or ou les matières premières suivent le cours du Dow Jones