Paul

PaulParticipant

Master

and an trailingstop with percentage, but with 3 steps. Didn’t optimise. i.e.

default trailingstop 2% (it needs to reach a positionperformance of 2%, to close on 2% retracement)

if positionperformance > 3% then change trailingstop to 1%

if positionperformance > 4% then change trailingstop to 0.5%

Hi Nonetheless, thks for this nice code on post #126280 but I tried with no succes on live IG, rejected order something wrong !! Can you watch ?

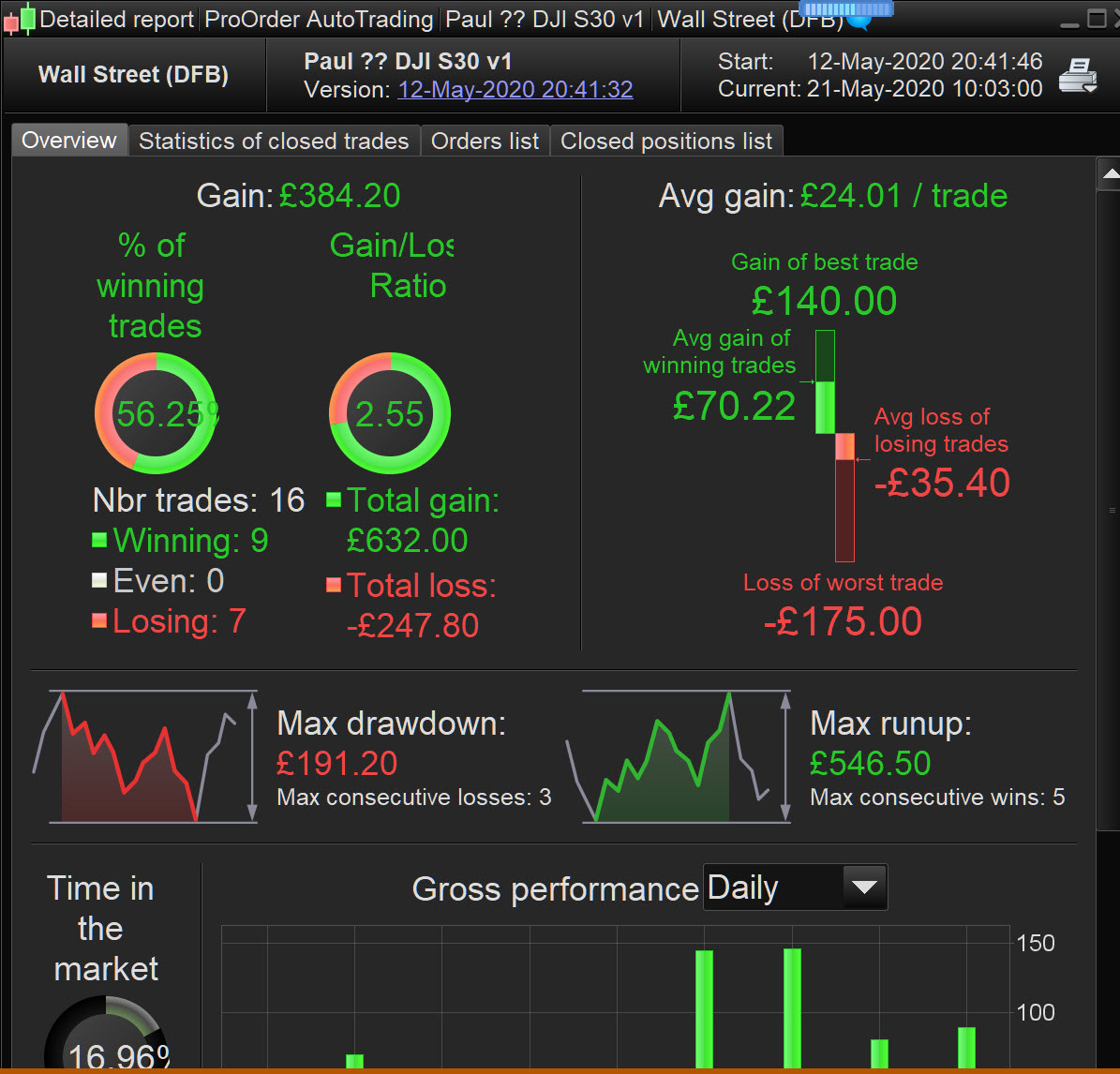

I’ve just set it going on Forward Test.

Seems to be doing well … results attached.

Not this one, post #126280 is on TF 5 minutes. I just try to change stop loss condition (if..) to classic SL code (I have an IG account with SL guaranteed) but same results…

/ Definition of code parameters

DEFPARAM CumulateOrders = FALSE // Cumulating positions deactivated

DEFPARAM preloadbars = 500

//Money Management DOW

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = 1

ONCE factor = 50 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE factor2 = 60 // tier 2 factor

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor2*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor2*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

//once enableSL = 1 // stop loss

once enablePT = 1 // profit target

once enableTS = 1 // trailing stop

once enableBE = 1 // breakeven stop

//once displaySL = 1 // stop loss

//once displayPT = 1 // profit target

//once displayTS = 1 // trailing stop

//once displayBE = 1 // breakeven stop

SL = 1.7//1.9 // % stop loss

PT = 2.4//2.3 // % profit target

TS = 0.4//0.35//0.26 // % trailing stop

BESG = 0.5//0.35//0.25 // % break even stop gain

BESL = 0.2//0.40//0.00 // % break even stop level

// underlaying security / index / forex

// profittargets and stoploss have to match the lines

// 0.01 FOREX [i.e. GBPUSD=0.01]

// 1.00 SECURITIES [i.e. aapl=1 ;

// 100.00 INDEXES [i.e. dax=100]

// 100=XAUUSD

// 100=CL US Crude

// DAX=100

underlaying=50//100

// reset at start

//if intradaybarindex=0 then

//longtradecounter=0

//shorttradecounter=0

//endif

//pclong = longtradecounter<1

//pcshort = shorttradecounter<1

TIMEFRAME(120 MINUTES,updateonclose)

Period= 495

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[8,6]

c3 = (close > indicator1)

c4 = (close < indicator1)

ma = average[60,3](close)

c11 = ma > ma[1]

c12 = ma < ma[1]

//Stochastic RSI | indicator

lengthRSI = 15 //RSI period

lengthStoch = 9 //Stochastic period

smoothK = 10 //Smooth signal of stochastic RSI

smoothD = 5 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c13 = K>D

c14 = K<D

TIMEFRAME(30 minutes,updateonclose)

indicator5 = Average[2](typicalPrice)

indicator6 = Average[7](typicalPrice)

c15 = (indicator5 > indicator6)

c16 = (indicator5 < indicator6)

TIMEFRAME(15 minutes,updateonclose)

indicator2 = Average[4](typicalPrice)

indicator3 = Average[8](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

ma2 = average[25,1](close)

c17 = ma2 > ma2[1]

c18 = ma2 < ma2[1]

Periodc= 23

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(10 minutes)

indicator1a = SuperTrend[2,7]

c19 = (close > indicator1a)

c20 = (close < indicator1a)

TIMEFRAME (5 minutes)//(default)

//Stochastic RSI | indicator

lengthRSIa = 3 //RSI period

lengthStocha = 6 //Stochastic period

smoothKa = 9 //Smooth signal of stochastic RSI

smoothDa = 3 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ma3 = average[15,3](close)

c21 = ma3 > ma3[1]

c22 = ma3 < ma3[1]

Periodb= 15

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

// Conditions to enter long positions

IF c1 AND C3 AND C5 and c7 and c9 and c11 and c13 and c15 and c17 and c19 and c21 and c23 THEN

BUY positionsize CONTRACT AT MARKET

set stop %loss SL

//longtradecounter=longtradecounter+1

ENDIF

// Conditions to enter short positions

IF c2 AND C4 AND C6 and c8 and c10 and c12 and c14 and c16 and c18 and c20 and c22 and c24 THEN

SELLSHORT positionsize CONTRACT AT MARKET

set stop %loss SL

//shorttradecounter=shorttradecounter+1

ENDIF

//================== exit in profit

if longonmarket and C6 and c8 and close>positionprice then

sell at market

endif

If shortonmarket and C5 and c7 and close<positionprice then

exitshort at market

endif

//==============exit at loss

if longonmarket AND c2 and c6 and close<positionprice then

sell at market

endif

If shortonmarket and c1 and c5 and close>positionprice then

exitshort at market

endif

// to set & display stoploss

//if enableSL then

//set stop %loss SL

//if displaysl then

//if not onmarket then

//sloss=0

//elsif ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

//sloss=0

//endif

//if onmarket then

//if longonmarket then

//sloss=tradeprice(1)-((tradeprice(1)*SL)/underlaying)*pointsize

//endif

//if shortonmarket then

//sloss=tradeprice(1)+((tradeprice(1)*SL)/underlaying)*pointsize

//endif

//endif

//graphonprice sloss coloured(255,0,0,255) as “stoploss”

//sloss=sloss

//endif

//endif

// to set & display profittarget

if enablePT then

set target %profit PT

//if displaypt then

//if not onmarket then

//ptarget=0

//elsif ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

//ptarget=0

//endif

//if onmarket then

//if longonmarket then

//ptarget=tradeprice(1)+((tradeprice(1)*PT)/underlaying)*pointsize

//endif

//if shortonmarket then

//ptarget=tradeprice(1)-((tradeprice(1)*PT)/underlaying)*pointsize

//endif

//endif

//graphonprice ptarget coloured(121,141,35,255) as “profittarget”

//ptarget=ptarget

//endif

endif

// trailing stop

if enableTS then

trailingstop = (tradeprice/100)*TS

if not onmarket then

maxprice=0

minprice=close

priceexit=0

endif

if ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice=0

minprice=close

priceexit=0

endif

if longonmarket then

maxprice=max(maxprice,close)

if maxprice-tradeprice(1)>=(trailingstop) then

priceexit=maxprice-(trailingstop/(underlaying/100))*pointsize

endif

endif

if shortonmarket then

minprice=min(minprice,close)

if tradeprice(1)-minprice>=(trailingstop) then

priceexit=minprice+(trailingstop/(underlaying/100))*pointsize

endif

endif

if longonmarket and priceexit>0 then

sell at priceexit stop

endif

if shortonmarket and priceexit>0 then

exitshort at priceexit stop

endif

//if displayTS then

//priceexit=priceexit

//graphonprice priceexit coloured(0,0,255,255) as “trailingstop”

//endif

endif

// break even stop

if enableBE then

if not onmarket then

newsl=0

endif

if ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl=0

endif

if longonmarket then

if close-tradeprice(1)>=(((tradeprice(1)/100)*BESG)/(underlaying/100))*pointsize then

newsl=tradeprice(1)+(((tradeprice(1)/100)*BESL)/(underlaying/100))*pointsize

endif

endif

if shortonmarket then

if tradeprice(1)-close>=(((tradeprice(1)/100)*BESG)/(underlaying/100))*pointsize then

newsl=tradeprice(1)-(((tradeprice(1)/100)*BESL)/(underlaying/100))*pointsize

endif

endif

if longonmarket and newsl>0 then

sell at newsl stop

endif

if shortonmarket and newsl>0 then

exitshort at newsl stop

endif

//if displayBE then

//newsl=newsl

//graphonprice newsl coloured(244,102,27,255) as “breakevenstop”

//endif

endif

//graph (positionperf*100)coloured(0,0,0,255) as “positionperformance”

this code works fine on backtest on Dow 5TF but noting on live. If somebody can help me ?

This part doesn’t look right – “underlaying=50//100”

@auvergnat

below you have certainly read some of the rules required by this forum.

One of them reads “Always use the ‘Insert PRT Code’ button when putting code in your posts to make it easier for others to read.”. Please stick to it. Thank you 🙂

with 100 same result in live = reject

I restart from scratch and it would seem it is ok if I put after buy and sellshort orders :

set stop %loss 1.7

set target %profit 2.4

instead of :

if enableSL then

set stop %loss SL

….

Hi @Paul

Thanks for your nice work !

Have you try to compare a strategy with and without breakeven, in a backtest on in Sample and Walk Forward In/OOS ?

Because in my experience it is often less interesting to be stop/lose frequentely on Breakeven than to have a bigger stop to let the trade breathe. May be to be at your Breakeven at x ATR could help instead a “classic” Breakeven at x Pips ?

Have a nice day

PaulParticipant

Master

Hi zilliq

Have you try to compare a strategy with and without breakeven, in a backtest on in Sample and Walk Forward In/OOS ?

no, because i’am in general not a fan of such approach. Again additional choices, how many reputations, which %, linked or not and if you found something and take the last parameters next question is when to run again? It’s very time consuming.

May be to be at your Breakeven at x ATR could help instead a “classic” Breakeven at x Pips

yeah could very well help. Something to test!

Take care

Hi @auvergnat, the code I posted in #1260280 was an unfinished test. The latest working version of that is here: #125210

Seems to be doing well

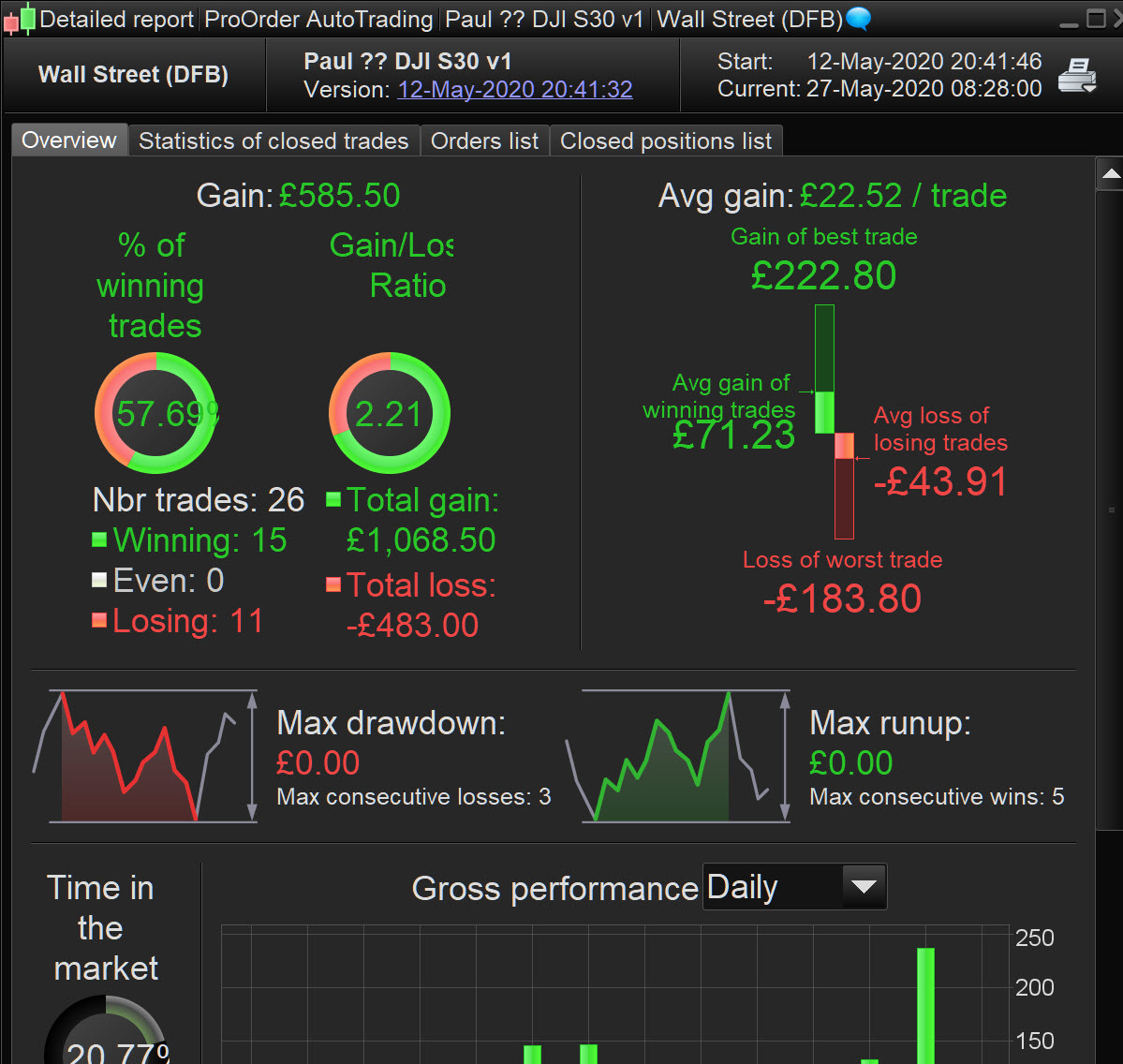

30 sec TF still looking good … 14 days Forward Test attached.

PaulParticipant

Master

wasn’t this a test version? It takes 2 signals, 1 long and 1 short after 0h at the most expensive time and let the last one run. Didn’t expect it would have any success.

Thanks for the post!

Hi @GraHal, every time I say ‘no more’ to sub-1m TFs I seem to get drawn back in. It’s all your fault.

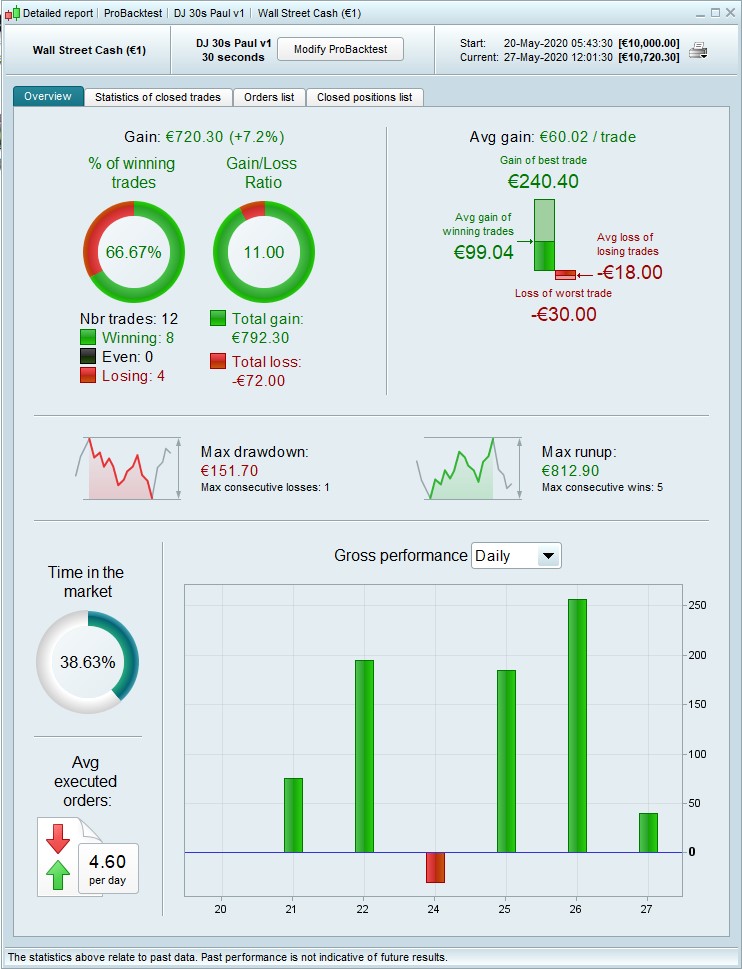

Anyway, I did a quick and dirty optimisation and you might want to try the following values:

SL = 0.75 // % stop loss

PT = 1.50 // % profit target

TS = .3 // % trailing stop

BESG = .15 // % break even stop gain

BESL = 0.00 // % break even stop level

sm = 20

lm = 40

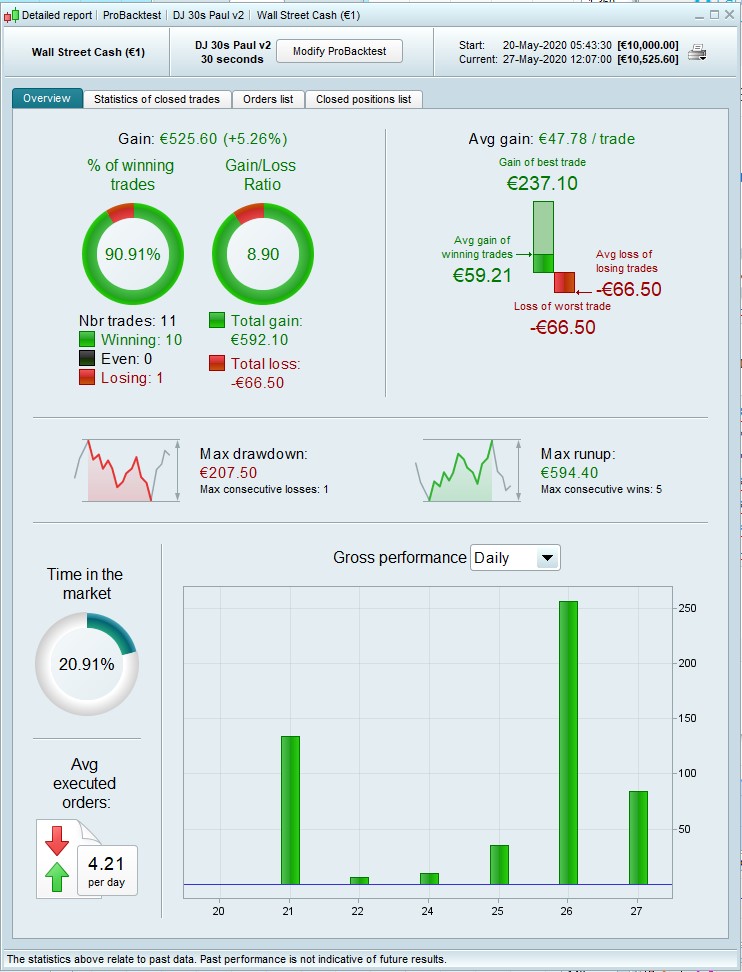

Or for a higher win rate, v2

SL = 0.75 // % stop loss

PT = 1.50 // % profit target

TS = .2 // % trailing stop

BESG = .15 // % break even stop gain

BESL = 0.00 // % break even stop level

sm = 20

lm = 30

For it not to have blown up in 14 days of forward testing is good going – maybe it’s a cash cow?