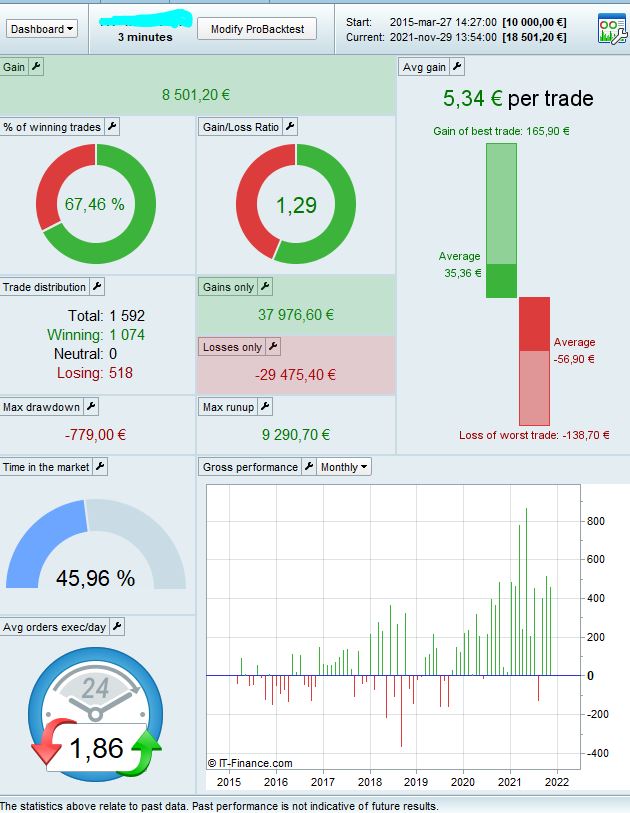

So weit bin ich heute nicht. Ich denke, M3 auch, oder M2 würde auch funktionieren. Gleicher Zeithorizont, nur schneller. Die Langversion von M3 funktioniert am besten an der Nasdaq. M1 auf SP500 und Dax. Ich habe Dow Jones noch nicht ausprobiert.

I’m not that far today. I think M3 too, or M2 would work too. Same time horizon, only faster. The long version of M3 works best on the Nasdaq. M1 on SP500 and Dax. I haven’t tried Dow Jones yet.

@nonethless: Sorry, I misspelled you.

I Combined Phonetzs code and made a long/short-version

How to make i better?

//Break-H4 Nasdaq M3

//================================================

DEFPARAM CUMULATEORDERS = false

defparam preloadbars = 5000

//Risk Management

PositionSize=1

timeframe(4hour, updateonclose)

barCount = barIndex

c1 = high

D1 = low

c2 = (Close > Open) //green

c3 = (Close < Open) //red

c4 = (high < high[1])//lowerhigh

c5 = (high > high[1])//higherhigh

//MACDLiniex = MACDline[12,26,9](close) > 0

MA5xx = Average[3,1](typicalprice) //close

MA10xx = Average[10,1](typicalprice) //close

MA15xx = Average[15,1](typicalprice) //15,1 close

mylongx = MA15xx > MA15xx[1] //and MA5xx > MA15xx// and MA10xx > MA15xx

MA5xxs = Average[19,1](typicalprice) //close

//MA10xx = Average[m2,1](typicalprice)

MA15xxs = Average[20,1](typicalprice) //15,1...40,6 close

//MA100xx = Average[m3,1](typicalprice) //close

myshortx = MA15xxs < MA15xxs[1] and MA5xxs < MA15xxs //and MA10xx < MA15xx

//mylongx2 = MA100xx > MA100xx[1]

shortcond = myshortx

timeframe(default)

once tradeOn = 1

if intradayBarIndex = 0 then

tradeOn = 1

endif

tradeBar = barCount

if not onMarket and tradeBar<>tradeBar[1] then

tradeOn = 1

endif

//Volaititätfilter

AvgRange = average[20,0](range)

TradeOFF = range > (AvgRange * 3) //no trading if the current range > twice its average //3

//myshort = MA < MA[1]

// trading window

ONCE BuyTime = 080000

ONCE SellTime = 215500

// position management

IF Time >= BuyTime AND Time <= SellTime THEN

If not onmarket and close crosses over c1 and mylongx and c3 and tradeOn Then //and not c5

Buy PositionSize CONTRACTS AT MARKET

SET STOP %LOSS 0.9 //100

SET TARGET %PROFIT 1 //125

tradeOn = 0

ENDIF

If not onmarket and close crosses over c1 and mylongx and c2 and tradeOn Then //and not TradeOFF and c3 close crosses over c1

Buy PositionSize CONTRACTS AT MARKET

SET STOP %LOSS 0.8 //100

SET TARGET %PROFIT 1 //125

tradeOn = 0

ENDIF

If not onmarket and close crosses under D1 and shortcond and tradeOn Then

sellshort PositionSize CONTRACTS AT MARKET

SET STOP %LOSS 0.7 //0.8

SET TARGET %PROFIT 0.8 //1

tradeOn = 0

ENDIF

endif

if time = 220000 and dayofweek=5 and (PositionPerf * PositionPrice / PipSize) >= 5 then //

sell at market

exitshort at market

endif

////////////////////////////////////////

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

trailingpercentlong = 0.32 // %

trailingpercentshort = 0.55 // %

once acceleratorlong = 0.015 // typically tst*0.1

once acceleratorshort= 0.025 // typically tss*0.1

ts2sensitivity = 2 // [1] close [2] high/low [3] low/high [4] typicalprice

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=(typicalprice)

ts2sensitivityshort=(typicalprice)

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong then

newsl = positionprice+trailingsteplong + 0.2

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong then

newsl = newsl+trailingsteplong

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort then

newsl = positionprice-trailingstepshort

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort then

newsl = newsl-trailingstepshort

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

if (shortonmarket and newsl > 0) or (longonmarket and newsl>0) then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

endif

if shortonmarket then

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

//////////////////////////////////////////////////////////////

Mein Plan wäre, beide Versionen, lang und kurz, einzeln laufen zu lassen. Ohne eine Vollversion daraus zu machen.

My plan would be to run both versions, long and short, individually. Without making a full version out of it.

@phoentzs

Only post in the language of the forum that you are posting in. For example English only in the English speaking forums and French only in the French speaking forums.

Thank you 🙂

Maybe one more question for the great masters … Nicolas? Robertogozzi? If you manage entries from large time units with a trailing stop … which TF is best used for this? M1… 5? Is more data history better or faster reaction to a trailing stop?

I usually use 5-minute or 10-minute TFs for the trailing stop, mainly because they grants more data history, compared to smaller TFs.

I made a quick attempt to add short to this but it didn’t seem worth it, I’ll have another try when I get time.

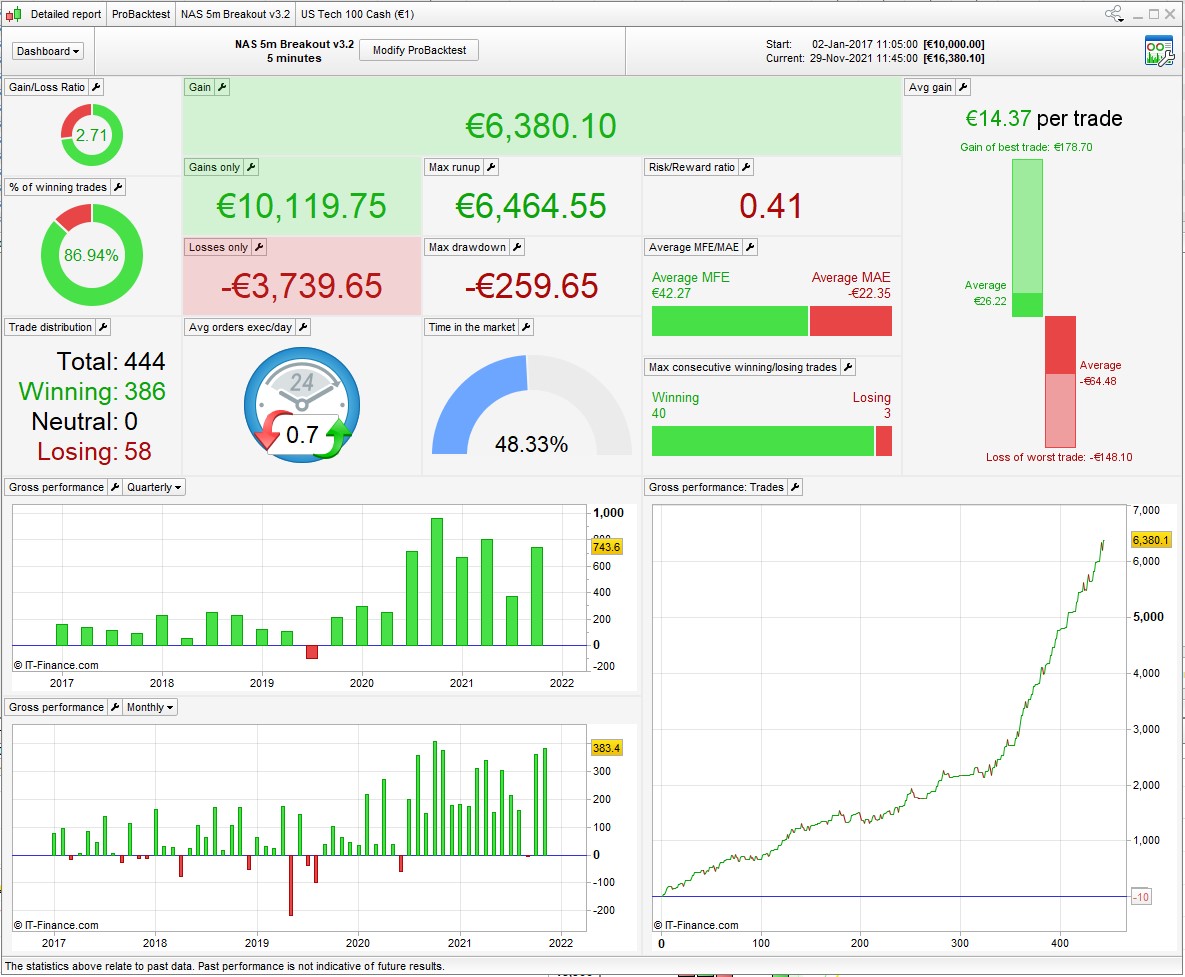

This is a minor revision to my long version, trying to get the DD as low as poss (positionsize = 0.5)

These are the key changes:

timeframe(4 hour, updateonclose)

H4 = high

MA = Average[p,t](close)

cb1 = MA > MA[1]

timeframe(15 minutes)

mb = average[p1,t1](typicalprice)

cb4 = mb > mb[1]

timeframe(default)

ST = SuperTrend[m,n]

STa = SAR[q,w,e]

cb2 = (close > ST) or (close > STa)

cb3 = close crosses over H4

an impressive piece of work, nonetheless.

What if it would be possible to make a long/short version of this algo 🙂

You can have a go if you have time to crunch the numbers. The core of it would look like this:

timeframe(4 hour, updateonclose)

H4 = high

L4 = Low

MA = Average[p,t](close)

cb1 = MA > MA[1]

MAs = Average[p2,t2](close)

cs1 = MAs < MAs[1]

timeframe(15 minutes)

mb = average[p3,t3](typicalprice)

cb2 = mb > mb[1]

mbs = average[p4,t4](typicalprice)

cs2 = mbs < mbs[1]

timeframe(default)

ST = SuperTrend[m,n]

STa = SAR[q,w,e]

cb3 = (close > ST) or (close > STa)

cs3 = (close < ST) or (close < STa)

cb4 = close crosses over H4

cs4 = close crosses under L4

If you haven’t used this syntax before

Average[p,t]

the ‘t’ represents the type of MA, can be 0 – 8

‘p’ I usually optimize from 5 – 50 in steps of 5

(apologies if you know this already 😁)

Thanks alot for the input nonetheless. I made an attempt for long/short-version.

Do u guys see any improvements? nonetheless, robertogozzi, phoentzs?

I want to get rid of the big drawdown in december 2021.

Backtest with Size 0.5

CUMULATEORDERS = false

In the itf both the % trail and ATR trail are active, which one did you want to use?

Using both gets better results then just one when i backtested

I am not sure if the idea is a good one. Isn’t that what affects each other? Unfortunately, due to the sudden drop in the Nasdaq over the last few days, the SL had to take action. That’s why the last few days lost in long mode. I personally help myself with this by splitting the risk over several systems. In that case I use half a position in TF M3 and a half position in TF M1. M1 made a profit from the faster trailing stop, M3 a loss.

that sounds weird to me, I think there will be conflicts in the code, I’ll have a closer look at it later.