Hello, I have a coding request for the following strategy from Galen Woods. Can someone code that for me, please?

These are the rules for a long trade signal:

The 9-period EMA must be above the 30-period WMA

The two moving averages must be separated from each other

The first bar to close below the 9 EMA is used as the trigger bar for the buy setup

Place a buy limit order above the high of the trigger bar.

If you want to go short, follow this three step process:

The 9-period EMA must be below the 30-period WMA

The two moving averages must be separated from each other

The first bar to close above the 9 EMA is used as the trigger bar for the sales setup

Place a sell limit order below the low of the trigger bar

Trailing stop loss below / above the WMA30

For better reading of the trading rules I found this website:

https://tradingstrategyguides.com/9-30-trading- strategy / # When_to_use_the_930_Trading_Method

There you go:

// 9-30 Trading Method

//

//https://tradingstrategyguides.com/9-30-trading-strategy/

//

DEFPARAM CumulateOrders = false

//

ONCE Trigger = 0

ONCE EntryL = 0

ONCE EntryS = 0

ONCE SL = 0

//

TradeON = (OpenTime >= 090000) AND (OpenTime <= 190000)

//

Ema9 = average[9,1](close)

Wma30 = average[30,2](close)

L1 = Ema9 > Wma30

S1 = Ema9 < Wma30

MAgap = abs(Ema9 - Wma30)

Apart = MAgap > average[20,0](MAgap)

Trigger = (L1 AND (close < Ema9)) OR (S1 AND (close > Ema9))

IF OnMarket OR (L1 <> L1[1]) OR (S1 <> S1[1]) THEN

Trigger = 0

EntryL = 0

EntryS = 0

SL = 0

ENDIF

IF (Apart AND L1) AND Not Trigger THEN

EntryL = high + 1 * PipSize

EntryS = 0

//SL = low - 1 * PipSize

SL = Wma30 - 1 * PipSize

ELSIF (Apart AND S1) AND Not Trigger THEN

EntryS = low - 1 * PipSize

EntryL = 0

//SL = high + 1 * PipSize

SL = Wma30 + 1 * PipSize

ENDIF

//

IF TradeON THEN

IF EntryL AND Not LongOnMarket THEN

BUY 1 CONTRACT AT EntryL STOP

SELL AT SL STOP

ELSIF EntryS AND Not ShortOnMarket THEN

SELLSHORT 1 CONTRACT AT EntryS STOP

EXITSHORT AT SL STOP

ENDIF

ENDIF

IF LongOnMarket THEN

SL = max(SL,Wma30)

SELL AT SL STOP

ELSIF ShortOnMarket THEN

SL = min(SL,Wma30)

EXITSHORT AT SL STOP

ENDIF

//-----------------------

// debugging code

Entry = EntryL

IF Entry = 0 THEN

Entry = EntryS

ENDIF

IF Entry > 0 THEN

graphonprice Entry

ENDIF

IF SL > 0 THEN

graphonprice SL coloured(0,128,0,155)

ENDIF

I used the more conservative trailing stop based on WMA30, but I also commented out the more aggressive way. You can simply use either by swapping comment slashes (but I think it shouldn’t be rewarding).

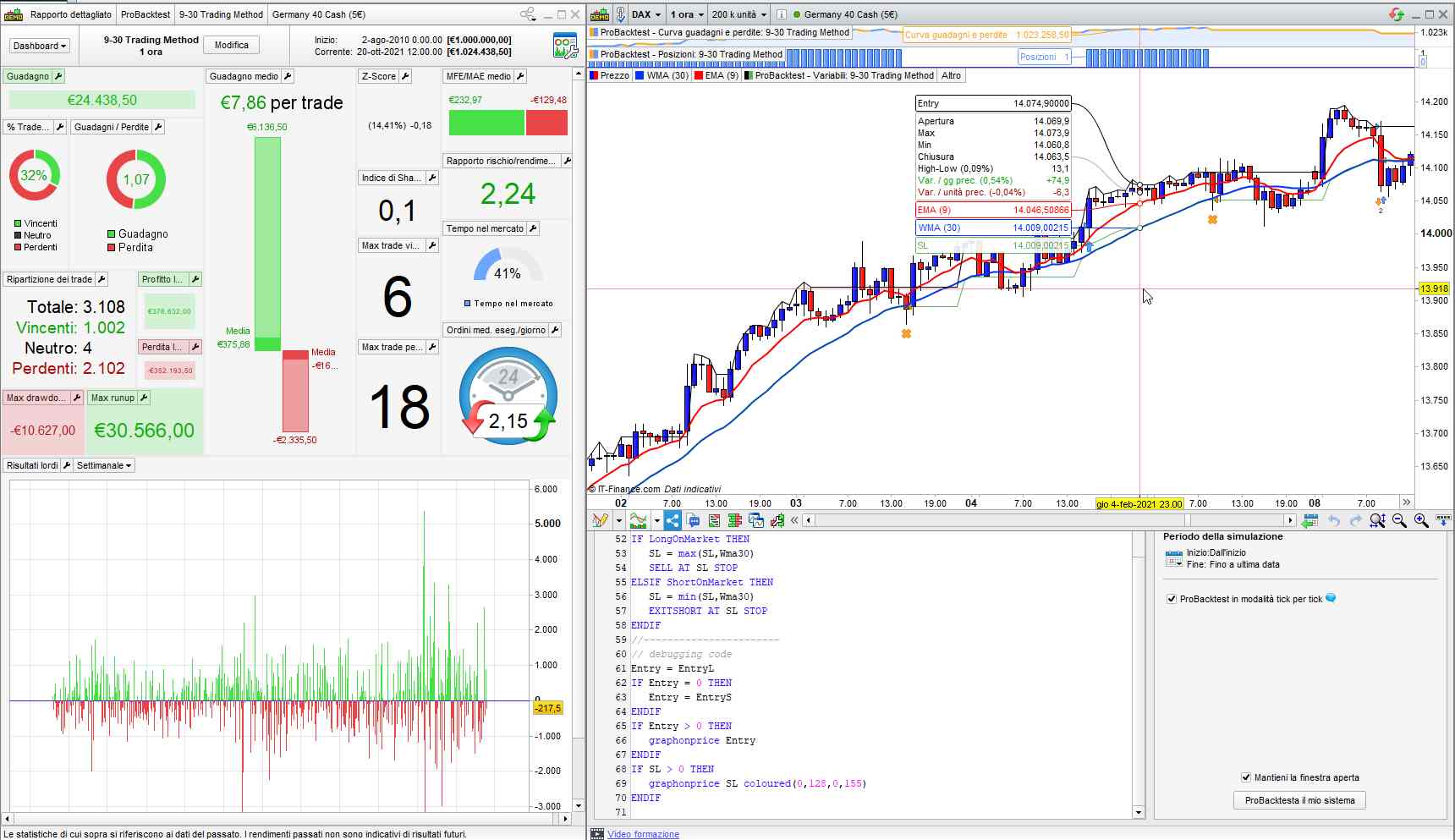

I tested it on DAX € 5, 1h TF, 200K units.

Thank you very much Roberto, the strategy looks good. The way it should work. I think the results are better on Nasdaq or SP500.

Can you please explain the function of lines 18 and 19 to me? In words?

Can you add a take profit? In relation to the SL, 1: 1 or 1: 1.5?

That’s to make sure the two averages have some gap in between them. I use GAP (difference) to calculate their distance, then I set variable APART only when that gap is greater than the its average over a given period.

Replace lines 27-37 by these ones (I couldn’t test them, though):

IF (Apart AND L1) AND Not Trigger THEN

EntryL = high + 1 * PipSize

EntryS = 0

//SL = low - 1 * PipSize

SL = Wma30 - 1 * PipSize

TP = abs(EntryL - SL) * 1.5

SET TARGET PROFIT TP

ELSIF (Apart AND S1) AND Not Trigger THEN

EntryS = low - 1 * PipSize

EntryL = 0

//SL = high + 1 * PipSize

SL = Wma30 + 1 * PipSize

TP = abs(EntryS - SL) * 1.5

SET TARGET PROFIT TP

ENDIF

replace 1.5 with any multiplier of your choice.

Thank you Roberto. I will test it in peace.

Hi Phoentz,

Thanks for digging on other sites to get new ideas ^^

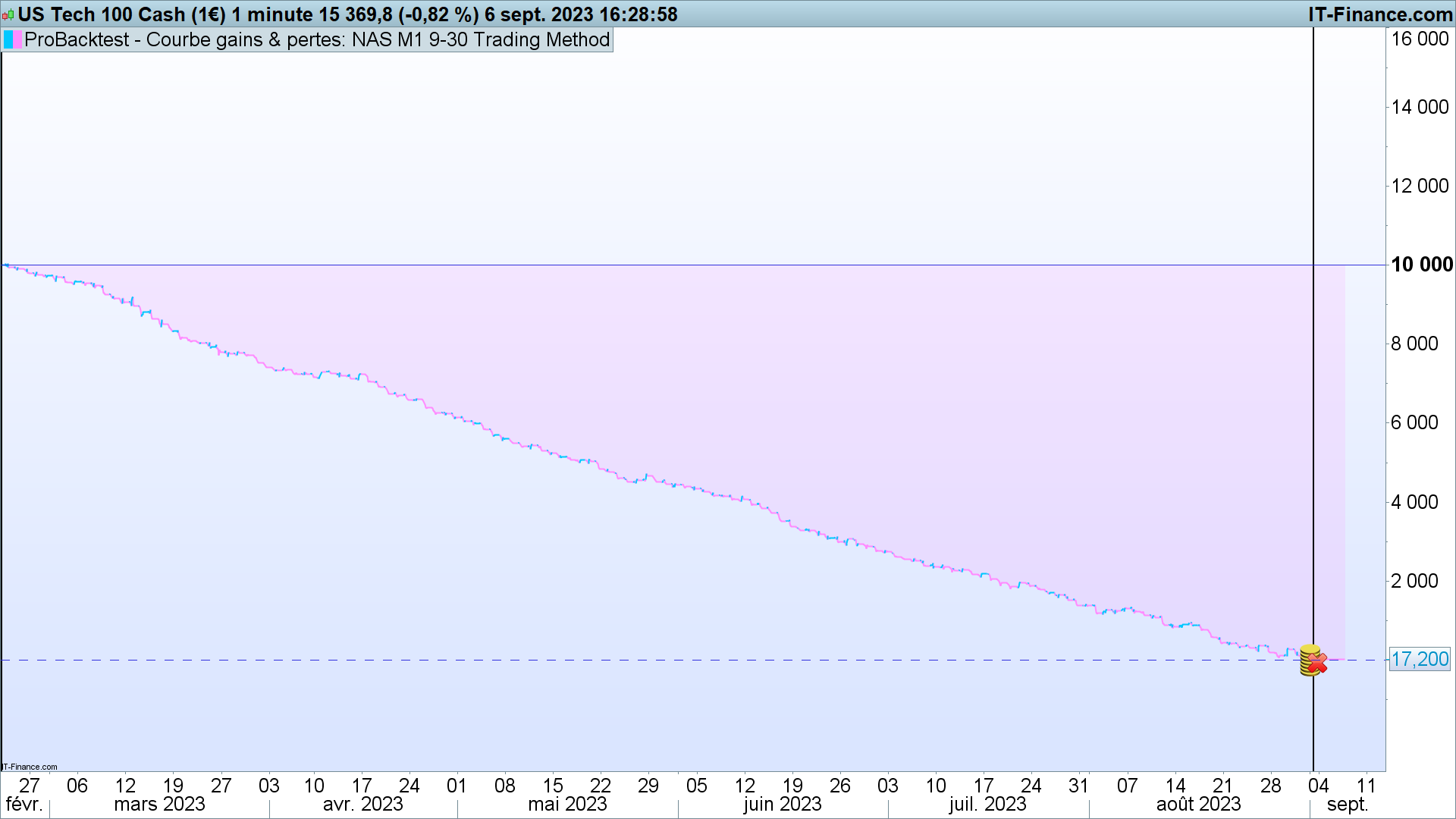

did you get a good backtest on this one and on which asset ? Mine are negative before 2021 on NAS H1;

best

The strategy is intended intraday… I got it to work quite adequately with changed values in the TF M1 on Nasdaq. It’s been a while. But I had the feeling that it wasn’t stable. But I’m a little smarter now than I was then. It’s possible that I didn’t have much of a clue as to how the system worked.

Ah ok I was updating the backtest of Roberto that was in “1 ora”

Coding request for EMA9 / WMA30 strategy

here is the backtest ;

Maybe inverting the conditions can make it a winner 😉

Thanks anyway,

Chris