Hi All

I know this is a big ask as it is a lot of code to wade through but hopefully someone might be able to spot the issue/provide some feedback as to what is wrong with my code below

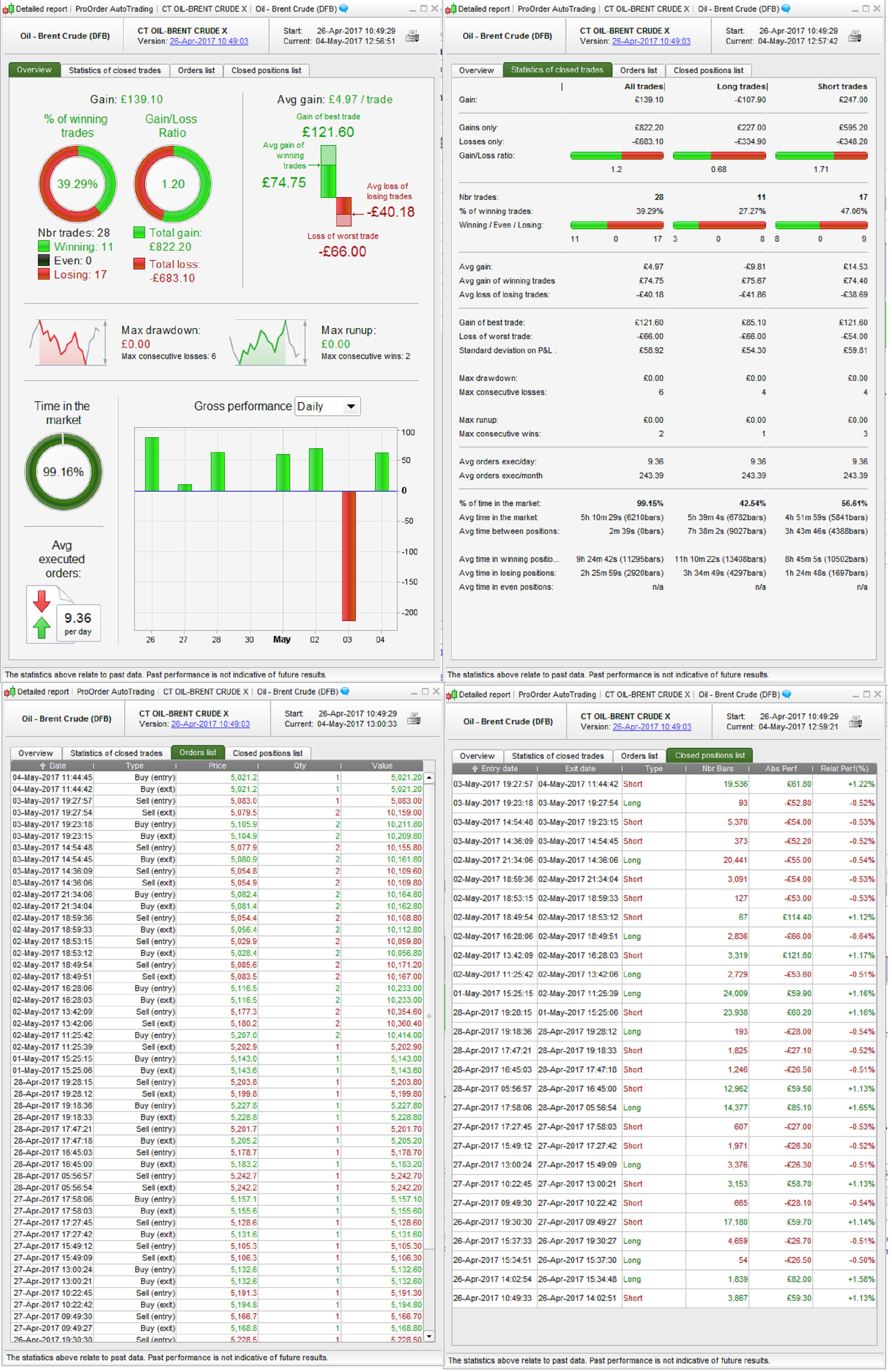

Basically I have all but given up on using any indicators/techniques for order entry and have decided instead to rely on the good old Coin Toss for order entry -> heads = buy tails = sell – then the majority of the strategy is how the trade is managed

Sounds daft I know but strategies both in demo and live have been performing better than average

The problem is that occasionally (after a week/couple weeks) and only some not all of the strategies will fail with the DEFPARAM/load more bars error and I cannot work out what is causing the problem – I’ve highlighted the part of code I ‘think’ is causing the problem but it is not using any indicators – it is only the random number generator that uses indicators and the ‘largest’ is the RSI[14] so 2000 bars is more than enough to load

Difficult to go into all the details of how strategy is working but if there is any interest/feedback just ask away and more than happy to try and explain 🙂

Cheers!

Max

//================= PARAMETERS ================

//*********************************************

DEFPARAM PRELOADBARS = 2000

DEFPARAM CUMULATEORDERS = FALSE

//============== CONSTANTS ====================

//*********************************************

ONCE MINPOSITIONSIZE=1 //MINIMUM ORDER SIZE AS PER IG OR WHATEVER YOU CHOOSE - POSITION SIZE WILL ALSO INCREASE/DECREASE BY THIS FIGURE

ONCE MYNUMBER=CURRENTSECOND //INITIAL SEED FIGURE FOR RANDOM NUMBER GENERATOR

ONCE POSITIONMULTIPLIER=4 //BASICALLY 'HOW MANY WINS BEFORE POSITION SIZE INCREASES'

ONCE COUNT = 0 //USED TO HOLD OFF ATR CALCULATION UNTIL FIRST CHANGE OF HOUR HAS OCCURRED

ONCE HIGHESTHIGH = 0 //USED IN ATR CALCULATION

ONCE LOWESTLOW = LOW[1]*10000 //USED IN ATR CALCULATION

ONCE INITIALATR=21.706 //THIS IS TAKEN MANUALLY FROM A HIGHER TIMEFRAME CHART USING BASIC INDICATOR - ATR=AVERAGETRUERANGE[8](CLOSE) AVERAGEATR=AVERAGE[1000] - MOSTLY USE 1 OR 2 HOUR TIMEFRAME

ONCE FIRSTTRADE=0 //USED TO ALLOW MANUAL TRADE FOR FIRST TRADE

//========== SPREAD VARIATIONS ================

//*********************************************

IF Time >= 070000 AND Time < 080000 THEN

SPREAD=2

ELSIF Time >= 080000 AND Time < 163000 THEN

SPREAD=1

ELSIF Time >= 163000 AND Time < 210000 THEN

SPREAD=2

ELSE

SPREAD=5

ENDIF

//======== 'RANDOM' NUMBER GENERATOR ==========

//*********************************************

MYNUMBER=round(((((RSI[14]*RSI[8])*(HIGH[MYNUMBER]+MEDIANPRICE))*((INTRADAYBARINDEX/(TIME+1)))+DAYS+(DAYOFWEEK+1)*MONTH)-ROUND((((RSI[14]*RSI[8])*(HIGH[MYNUMBER]+MEDIANPRICE))*((INTRADAYBARINDEX/(TIME+1)))+DAYS+(DAYOFWEEK+1)*MONTH)/10-0.49)*10)-0.4)/10

RANDOM=ROUND(MYNUMBER[(MYNUMBER*10)])

//SLIGHTLY EDITED VERSION OF CODE FROM HERE - https://www.prorealcode.com/topic/random-value/ - THANK YOU @WING!

//================ STRATEGY ===================

//*********************************************

IF COUNT = 0 THEN

AVERAGEATR=INITIALATR //ALLOWS FOR IMMEDIATE ORDER ENTRY ON STRATEGY START

ENDIF

IF OPENHOUR<>OPENHOUR[1] THEN //1HRAVGATR - USED IF TAKING AVERAGEATR FROM 1 HOUR CHART

//IF (OPENHOUR[1] = 23 AND OPENHOUR = 0) OR (OPENHOUR[1]=1 AND OPENHOUR=2) OR (OPENHOUR[1]=3 AND OPENHOUR=4) OR (OPENHOUR[1]=5 AND OPENHOUR=6) OR (OPENHOUR[1]=7 AND OPENHOUR=8) OR (OPENHOUR[1]=9 AND OPENHOUR=10) OR (OPENHOUR[1]=11 AND OPENHOUR=12) OR (OPENHOUR[1]=13 AND OPENHOUR=14) OR (OPENHOUR[1]=15 AND OPENHOUR=16) OR (OPENHOUR[1]=17 AND OPENHOUR=18)OR (OPENHOUR[1]=19 AND OPENHOUR=20) OR (OPENHOUR[1]=21 AND OPENHOUR=22) THEN //2HRAVGATR - USED IF TAKING AVERAGEATR FROM 2 HOUR CHART

//IF (OPENHOUR[1] = 23 AND OPENHOUR = 0) OR (OPENHOUR[1]=2 AND OPENHOUR=3) OR (OPENHOUR[1]=5 AND OPENHOUR=6) OR (OPENHOUR[1]=8 AND OPENHOUR=9) OR (OPENHOUR[1]=11 AND OPENHOUR=12) OR (OPENHOUR[1]=14 AND OPENHOUR=15) OR (OPENHOUR[1]=17 AND OPENHOUR=18) OR (OPENHOUR[1]=20 AND OPENHOUR=21) THEN //3HRAVGATR - USED IF TAKING AVERAGEATR FROM 3 HOUR CHART

//IF (OPENHOUR[1] = 23 AND OPENHOUR = 0) OR (OPENHOUR[1]=3 AND OPENHOUR=4) OR (OPENHOUR[1]=7 AND OPENHOUR=8) OR (OPENHOUR[1]=11 AND OPENHOUR=12) OR (OPENHOUR[1]=15 AND OPENHOUR=16) OR (OPENHOUR[1]=19 AND OPENHOUR=20) THEN //4HRAVGATR - USED IF TAKING AVERAGEATR FROM 4 HOUR CHART

//ONGOING ATR CALCULATION BEGIN (THIS IS WHERE I THINK THE PROBLEM IS...)

IF COUNT = 1 THEN

AVERAGEATR=((INITIALATR*999)+TR0)/1000

IF HIGHESTHIGH>PREVIOUSBLOCKHIGH AND LOWESTLOW<PREVIOUSBLOCKLOW THEN

TR0 = HIGHESTHIGH-LOWESTLOW

ELSIF PREVIOUSBLOCKCLOSE>HIGHESTHIGH OR PREVIOUSBLOCKCLOSE<LOWESTLOW THEN

B1 = ABS(HIGHESTHIGH-PREVIOUSBLOCKCLOSE)

B2 = ABS(LOWESTLOW-PREVIOUSBLOCKCLOSE)

TR0 = MAX(B1,B2)

ELSE

C1 = HIGHESTHIGH-LOWESTLOW

C2 = ABS(HIGHESTHIGH-PREVIOUSBLOCKCLOSE)

C3 = ABS(LOWESTLOW-PREVIOUSBLOCKCLOSE)

C4 = MAX(C1,C2)

TR0 = MAX(C3,C4)

ENDIF

ENDIF

IF COUNT = 2 THEN

AVERAGEATR = ((AVERAGEATR*999)+TR0)/1000

IF HIGHESTHIGH>PREVIOUSBLOCKHIGH AND LOWESTLOW<PREVIOUSBLOCKLOW THEN

TR0 = HIGHESTHIGH-LOWESTLOW

ELSIF PREVIOUSBLOCKCLOSE>HIGHESTHIGH OR PREVIOUSBLOCKCLOSE<LOWESTLOW THEN

B1 = ABS(HIGHESTHIGH-PREVIOUSBLOCKCLOSE)

B2 = ABS(LOWESTLOW-PREVIOUSBLOCKCLOSE)

TR0 = MAX(B1,B2)

ELSE

C1 = HIGHESTHIGH-LOWESTLOW

C2 = ABS(HIGHESTHIGH-PREVIOUSBLOCKCLOSE)

C3 = ABS(LOWESTLOW-PREVIOUSBLOCKCLOSE)

C4 = MAX(C1,C2)

TR0 = MAX(C3,C4)

ENDIF

ENDIF

HIGHESTHIGH = HIGH

LOWESTLOW = LOW

PREVIOUSBLOCKHIGH = HIGHESTHIGH[1]

PREVIOUSBLOCKLOW = LOWESTLOW[1]

PREVIOUSBLOCKCLOSE = CLOSE[1]

IF COUNT < 2 THEN

COUNT=COUNT+1

ENDIF

ELSE

HIGHESTHIGH = MAX(HIGHESTHIGH,HIGH)

LOWESTLOW = MIN(LOWESTLOW,LOW)

IF COUNT>=1 THEN

IF HIGHESTHIGH>PREVIOUSBLOCKHIGH AND LOWESTLOW<PREVIOUSBLOCKLOW THEN

A1 = HIGHESTHIGH-LOWESTLOW

TR0 = MAX(TR0,A1)

ELSIF PREVIOUSBLOCKCLOSE>HIGHESTHIGH OR PREVIOUSBLOCKCLOSE<LOWESTLOW THEN

B1 = ABS(HIGHESTHIGH-PREVIOUSBLOCKCLOSE)

B2 = ABS(LOWESTLOW-PREVIOUSBLOCKCLOSE)

B3 = MAX(B1,B2)

TR0 = MAX(TR0,B3)

ELSE

C1 = HIGHESTHIGH-LOWESTLOW

C2 = ABS(HIGHESTHIGH-PREVIOUSBLOCKCLOSE)

C3 = ABS(LOWESTLOW-PREVIOUSBLOCKCLOSE)

C4 = MAX(C1,C2)

C5 = MAX(C3,C4)

TR0 = MAX(TR0,C5)

ENDIF

ENDIF

ENDIF

//ONGOING ATR CALCULATION END

//*******************************************

//================TRADING====================

//*******************************************

//ORDER ENTRY BEGIN

IF NOT ONMARKET THEN

IF STRATEGYPROFIT<-(2*MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER) THEN //'FAILSAFE' OVERALL STOPLOSS

QUIT

ENDIF

//TRADING BOUNDARIES CALCULATION BEGIN

IF POSCOUNT=0 THEN

POSITIONSIZE=MINPOSITIONSIZE

POSBOUNDARY=(POSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER)

PREVIOUSPOSBOUNDARY=-POSBOUNDARY

TARGETPOSBOUNDARY=POSBOUNDARY+((POSITIONSIZE+MINPOSITIONSIZE)*AVERAGEATR*POSITIONMULTIPLIER)

ENDIF

IF STRATEGYPROFIT > TARGETPOSBOUNDARY THEN

PREVIOUSPOSBOUNDARY=POSBOUNDARY

POSBOUNDARY=POSBOUNDARY+((POSITIONSIZE+MINPOSITIONSIZE)*AVERAGEATR*POSITIONMULTIPLIER)

POSITIONSIZE=POSITIONSIZE+MINPOSITIONSIZE

TARGETPOSBOUNDARY=POSBOUNDARY+((POSITIONSIZE+MINPOSITIONSIZE)*AVERAGEATR*POSITIONMULTIPLIER)

POSCOUNT=1

ENDIF

IF STRATEGYPROFIT < PREVIOUSPOSBOUNDARY THEN

TARGETPOSBOUNDARY=POSBOUNDARY

IF TARGETPOSBOUNDARY<=(MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER)+(2*MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER) THEN

TARGETPOSBOUNDARY=(MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER)+(2*MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER)

ENDIF

POSBOUNDARY=PREVIOUSPOSBOUNDARY

IF POSBOUNDARY<=(MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER) THEN

POSBOUNDARY=(MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER)

ENDIF

PREVIOUSPOSBOUNDARY=POSBOUNDARY-((POSITIONSIZE-MINPOSITIONSIZE)*AVERAGEATR*POSITIONMULTIPLIER)

IF PREVIOUSPOSBOUNDARY<=0 OR PREVIOUSPOSBOUNDARY=POSBOUNDARY THEN

PREVIOUSPOSBOUNDARY=-(MINPOSITIONSIZE*AVERAGEATR*POSITIONMULTIPLIER)

ENDIF

POSITIONSIZE=MAX(MINPOSITIONSIZE, POSITIONSIZE-MINPOSITIONSIZE)

ENDIF

//TRADING BOUNDARIES CALCULATION END

//POSITION SIZE 'STOPLOSS' BEGIN

IF N=1 THEN

IF POSITIONSIZE<=HIGHESTPOSITIONSIZE-(2*MINPOSITIONSIZE) THEN

QUIT

ENDIF

ENDIF

IF POSITIONSIZE>5*MINPOSITIONSIZE AND POSITIONSIZE<=10*MINPOSITIONSIZE THEN

HIGHESTPOSITIONSIZE = MAX(HIGHESTPOSITIONSIZE, POSITIONSIZE)

N=1

ENDIF

IF N=2 THEN

IF POSITIONSIZE<=HIGHESTPOSITIONSIZE-MINPOSITIONSIZE THEN

QUIT

ENDIF

ENDIF

IF POSITIONSIZE>10*MINPOSITIONSIZE THEN

HIGHESTPOSITIONSIZE = MAX(HIGHESTPOSITIONSIZE, POSITIONSIZE)

N=2

ENDIF

//POSITION SIZE 'STOPLOSS' END

//ORDER ENTRY BEGIN

IF FIRSTTRADE=0 THEN

SELLSHORT POSITIONSIZE CONTRACT AT MARKET

CONTINUATION=1

LADDERCOUNT=1

ELSIF FIRSTTRADE=1 THEN

IF RANDOM=1 THEN

BUY POSITIONSIZE CONTRACTS AT MARKET

CONTINUATION=1

LADDERCOUNT=1

ENDIF

IF RANDOM=0 THEN

SELLSHORT POSITIONSIZE CONTRACT AT MARKET

CONTINUATION =1

LADDERCOUNT=1

ENDIF

ENDIF

//ORDER ENTRY END

ENDIF

//ORDER MANAGEMENT BEGIN

IF LONGONMARKET THEN

STOPLOSS=AVERAGEATR+SPREAD

STOPPRICE = TRADEPRICE(1)-STOPLOSS

IF CLOSE>TRADEPRICE(1) THEN

PRICEDIFFERENCE = CLOSE-TRADEPRICE(1)

STOPLADDER = ROUND(PRICEDIFFERENCE/STOPLOSS)

IF STOPLADDER<3 THEN

STOPLADDER=0

ENDIF

CONTINUATION = SUMMATION[LADDERCOUNT](STOPLADDER>=STOPLADDER[1])=LADDERCOUNT

LADDERCOUNT=LADDERCOUNT+1

ENDIF

ENDIF

IF LONGONMARKET AND CLOSE<=STOPPRICE OR CONTINUATION=0 THEN

SELL AT MARKET

STOPLADDER=0

LADDERCOUNT=1

FIRSTTRADE=1

ENDIF

IF SHORTONMARKET THEN

STOPLOSS=AVERAGEATR+SPREAD

STOPPRICE = TRADEPRICE(1)+STOPLOSS

IF CLOSE<TRADEPRICE(1) THEN

PRICEDIFFERENCE = TRADEPRICE(1)-CLOSE

STOPLADDER = ROUND(PRICEDIFFERENCE/STOPLOSS)

IF STOPLADDER<3 THEN

STOPLADDER=0

ENDIF

CONTINUATION = SUMMATION[LADDERCOUNT](STOPLADDER>=STOPLADDER[1])=LADDERCOUNT

LADDERCOUNT=LADDERCOUNT+1

ENDIF

ENDIF

IF SHORTONMARKET AND CLOSE>=STOPPRICE OR CONTINUATION=0 THEN

EXITSHORT AT MARKET

STOPLADDER=0

LADDERCOUNT=1

FIRSTTRADE=1

ENDIF

//ORDER MANAGEMENT END

//**********************************************************************************************

//GRAPH POSBOUNDARY coloured(255,0,255)

//GRAPH PREVIOUSPOSBOUNDARY coloured(255,0,255)

//GRAPH TARGETPOSBOUNDARY coloured(0,0,255)

//GRAPH POSITIONSIZE COLOURED(0,0,0,25)

//GRAPH STRATEGYPROFIT coloured(0,128,0)

//GRAPH AVERAGEATR

//GRAPH POSCOUNT

//GRAPH STOPLOSS

//GRAPH RANDOM

//GRAPH STOPLADDER

//GRAPH ATR

//GRAPH STOPPRICE

//GRAPH HIGH

//GRAPH LOW

//GRAPH HIGHESTHIGH

//GRAPH LOWESTLOW

//GRAPH PREVIOUSBLOCKCLOSE

//GRAPH PREVIOUSBLOCKLOW

//GRAPH PREVIOUSBLOCKHIGH

//GRAPH PREVIOUSBLOCKCLOSE