Ciao Roberto, ho provato un tuo codice per la determinazione del massimo numero di operazioni al giorno che mi piace come è scritto, ma, a volte, dà dei risultati differenti (e penso sbagliati) rispetto ad un codice classico che uso (ma che mi piace di meno come è scritto) per ottenere lo stesso risultato.

Il tuo nuovo codice lo ho ripreso dal seguente link [rif: 191639]: https://www.prorealcode.com/topic/help-coding-breakout-strategy/

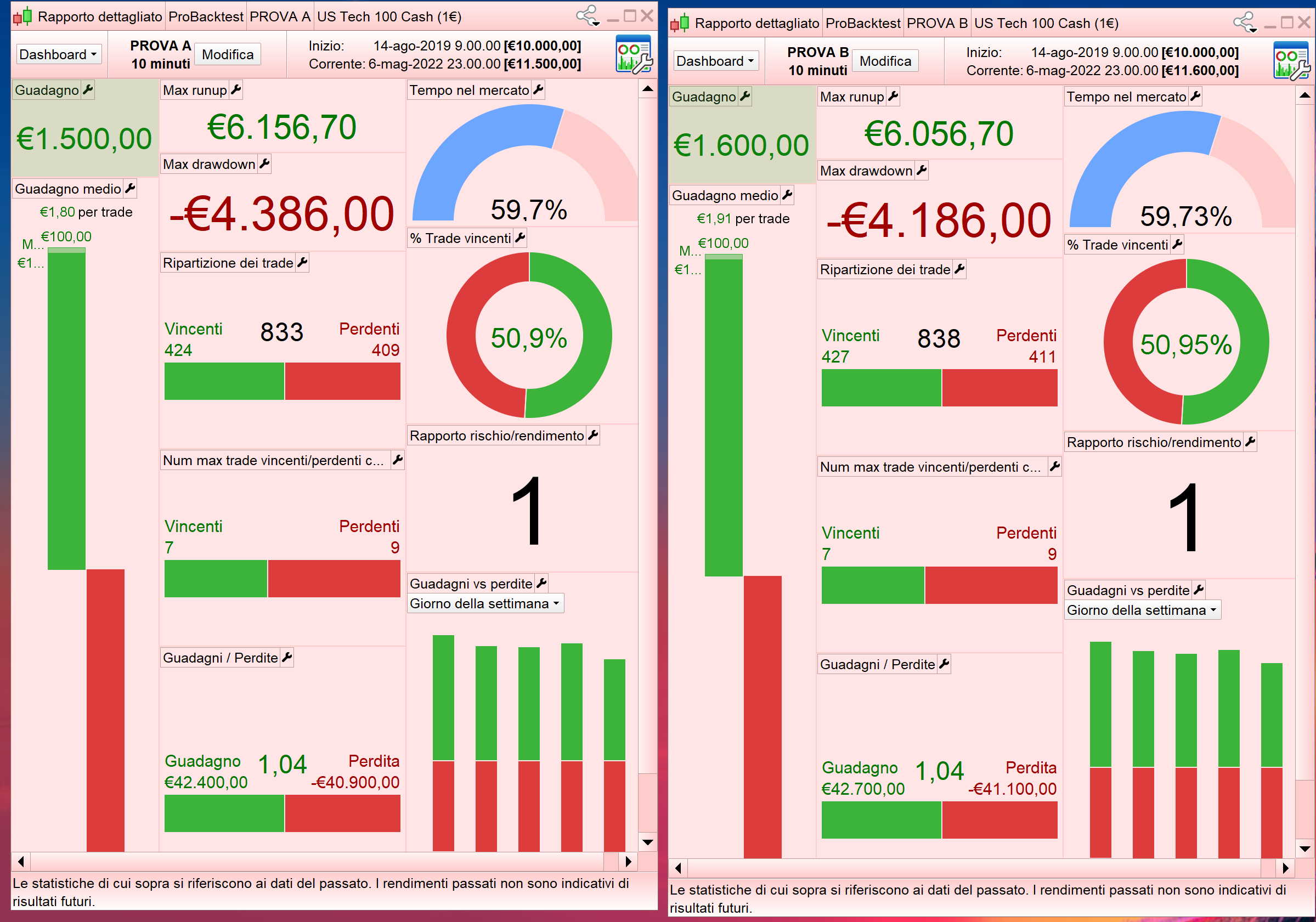

Provando entrambi i codici su un TS di prova danno risultato differenti [ test su Nasdaq cfd – 10 minuti – 100k]. Sai quale può essere il motivo?

Ecco i codici con il TS di base:

PROVA A

if intradayBarIndex=0 then

count=0

endif

if ( (not onMarket and onMarket[1] and not onMarket[2]) or (tradeIndex(1)=tradeIndex(2) and tradeIndex(1)=barIndex[1] and tradeIndex(1)>0) or (not onMarket and onMarket[1])) then

count = count+1

endif

//--------------------------------------------------------------

if close crosses over average[50,0](close) and not onMarket and count < 3 then

buy 1 contract at market

endif

set target pProfit 100

set stop pLoss 100

PROVA B (tuo nuovo codice)

once maxTrades = 3

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or (longOnMarket and shortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((not OnMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//--------------------------------------------------------------

if close crosses over average[50,0](close) and not onMarket and tally < maxTrades then

buy 1 contract at market

endif

set target pProfit 100

set stop pLoss 100

Ed ecco il test:

Verificando le date e gli orari d’apertura, magari esportando il risultato su eXcel, in quali candele ci sono le differenze?

Ciao Roberto, ho trovato alcune operazioni discordanti.

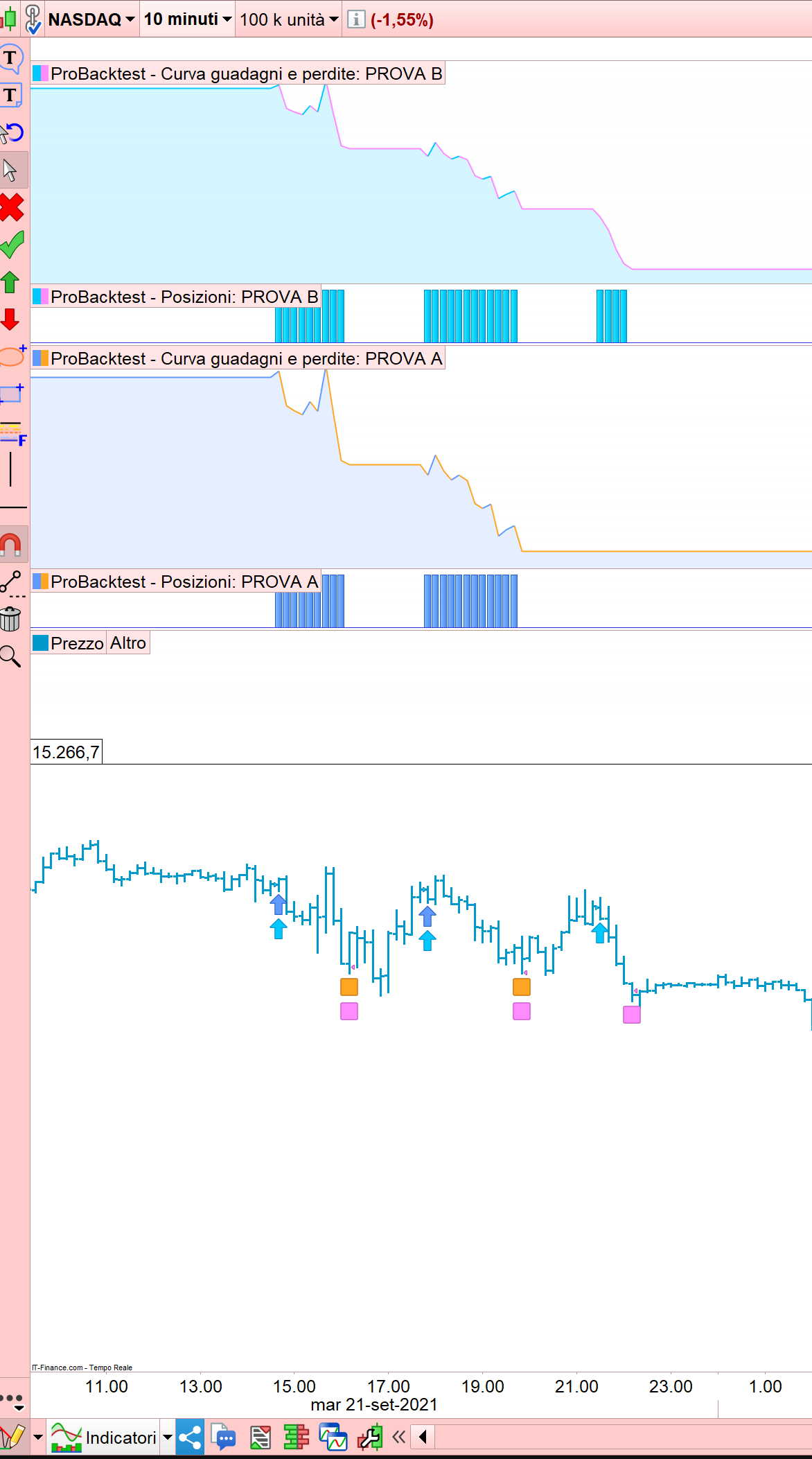

1) In tutti i casi è lo snippet classico (prova A) che salta un operazione senza che sia chiaro il motivo. Ti segnalo alcune operazioni cosi puoi controllare il motivo del malfunzionamento: 21 settembre 2021 – 28 gennaio 2022 – 19 aprile 2022 (vd immagine A ed A2)

2) [Il 28 gennaio 2022 ( vd immagine B) poi c’è un operazione visibile nel probacktest ed anche nell’indicatore delle posizioni, ma non segnalata da nessuno dei due codici (e non presente quindi nel listato delle operazioni)

In merito alla prova A:

- il 21/9/2021 mi sembra corretto, si chiudono 3 operazioni ed il conto è 3 (una si era aperta il giorno prima)

- il 28/1/2022 stessa identica cosa, 3 chiusi ed il conto è 3

- il 19/4/2022 ancora identica cosa, 3 chiusi ed il conto è 3.

Le differenze sono dovute al fatto che il codice A fa una verifica diversa, quindi non tiene conto del fatto che un’operazione sia iniziata il giorno prima, mentre il codice B fa una verifica appena entrato a mercato, quindi se è del giorno precedente non influisce sul giorno successivo in quanto tu azzeri il conteggio con la prima barra del giorno dopo.

Per ottenere lo stesso risultato (non in senso finanziario, solo per il controllo delle operazioni fatte), aggiungi questa riga all’inizio:

defparam flatafter = 220000

Grazie, Roberto, penso di utilizzare il tuo codice B. Mi piace di più come è scritto e preferisco che il conteggio sia interno ad ogni giornata senza mischiare i giorni.

Ciao Roberto, ho provato il tuo codice sul massimo numero di operazioni aggiornato e le nuove istruzioni di Nicolas. Su questo TS molto semplice sono equivalenti.

once maxTrades = 3 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or (longOnMarket and shortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((not OnMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//--------------------------------------------------------------------------------

if close crosses over average[50,0](close) and not longOnMarket and tally < maxTrades then

buy 1 contract at market

endif

set target pProfit 100

set stop pLoss 100

once maxOrders = 3

if intradayBarIndex = 0 then //reset orders count

ordersCount = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCount = ordersCount + 1

endif

//--------------------------------------------------------------------------------

if close crosses over average[50,0](close) and not longOnMarket and ordersCount < maxOrders then

buy 1 contract at market

endif

set target pProfit 100

set stop pLoss 100

Devo dire grazie. Con un limite di ordini al giorno risolvi molti problemi nei mercati laterali.

Oltre al limite degli ordini, uso la massima perdita giornaliere e l’attesa tra un trade e l’altro.

Ho assemblato questi 3 snipper in uno complessivo che chiamo: cManagemente (da aggiungere alle tue condizioni di entrata).

Se ti interessa ecco un esempio (puoi chiaramente ottimizzare i parametri.

//----------------------------------------------------------------

maxDailyLoss = 200 //maxMonetaryDailyLoss

realPosition=positionPerf*positionPrice/pointSize*pointValue

once tradeAllowed = 1

if intradayBarIndex = 0 then

myProfit=strategyProfit

tradeAllowed = 1

endif

if (strategyProfit+realPosition) <= (myProfit-maxDailyLoss) then

tradeAllowed = 0

endif

//----------------------------------------------------------------------------------------------------------

once maxTrades = 5 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or ((not onMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or (longOnMarket and ShortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//-------------------------------------------------------------------------------------------------------

once barCount = 0 //barsToWaitAfterTrade

waitingBars = 10

once tradeCount = 1

newTrades = (onMarket and not onMarket[1]) or ((not onMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or (longOnMarket and ShortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tradeCount = 0

barCount = 0

endif

if not longOnMarket then

barCount = barCount + 1

endif

if barCount > waitingBars then

tradeCount = 1

endif

//**********************************************************************************************

cManagement = tradeAllowed and tally < maxTrades and barCount > waitingBars

//***********************************************************************************************

nella riga 35 meglio scrivere : if not onMarket then

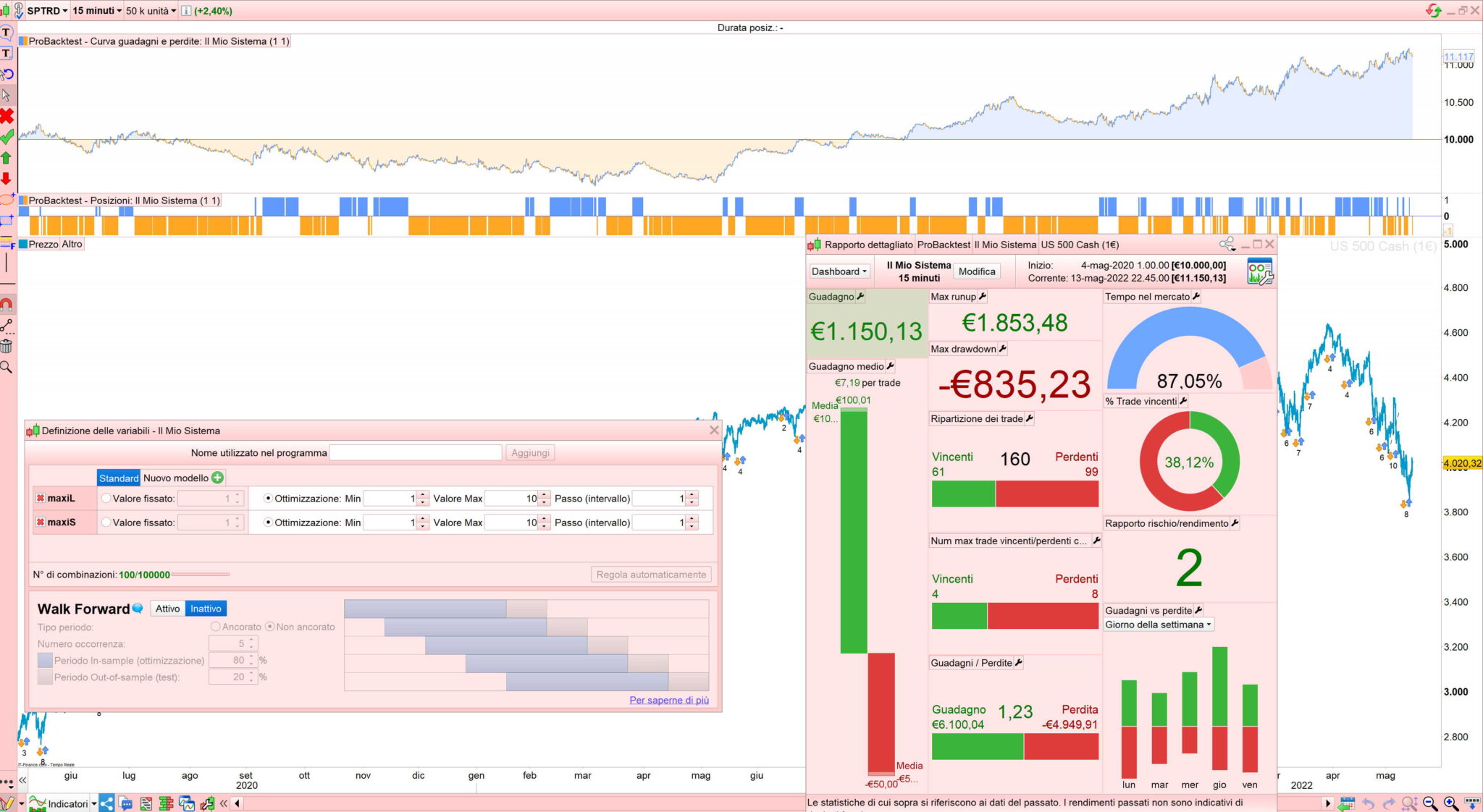

@Mauro

È possibile che questo codice genera uno per 0 errori? Ho aggiunto questa variante al mio codice … backtest völlig in ordine, ma quando si avvia il messaggio di errore viene che un indicatore mostra un valore negativo.

//Max-Orders per Day

once maxOrdersL = maxiL

once maxOrdersS = maxiS

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//

Lo ho testato in questo TS di prova e funziona.

//S&P 500 - 15m - test: 50k

//-------------------------------

//Max-Orders per Day

once maxOrdersL = maxiL

once maxOrdersS = maxiS

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//

//-------------------------------------------------------------------------

if close crosses over average[50,0](close) and not onMarket and ordersCountL < maxOrdersL then

buy 1 contract at market

endif

if close crosses under average[50,0](close) and not onMarket and ordersCountS < maxOrdersS then

sellShort 1 contract at market

endif

//-----------------------------------------------------------------------

set target pProfit 100

set stop pLoss 50

Ok, ho trovato l’errore. Un valore inutilizzato nell’ottimizzatore è stato impostato su “0”.

Scusa, errore mio.

Grazie mille per il tuo post mauro.

lo snippet è interessante.

Ciao, mauro

Torno da voi perché sto cercando di integrare il vostro codice qui allegato se non sbaglio

Dalla linea 32 del mio algo, ma senza la condizione di media 50, non succede nulla cambiando i miei take profit e stop che sono 11 e 34 e un’operazione al giorno.

Se puoi, puoi farmi una copia di come la inseriresti nel mio codice. Grazie.

Mi dispiace, sono ancora nelle prime fasi di creazione del codice.

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Annule tous les ordres en attente et ferme toutes les positions à l'heure "FLATAFTER"

DEFPARAM FLATAFTER = 173000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 153000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 173000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = RSI[14](close)

c1 = (indicator1 CROSSES OVER 30)

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

indicator2 = RSI[14](close)

c2 = (indicator2 CROSSES UNDER 70)

IF c2 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

once maxOrders = 1

if intradayBarIndex = 0 then //reset orders count

ordersCount = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCount = ordersCount + 1

endif

// Stops et objectifs

SET STOP pTRAILING 31

SET TARGET pPROFIT 11

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 5 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 10 //10 Pip chunks to increase Percentage

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.100 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 7 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Devi inserire l’istruzione anche nelle condizioni di acquisto e vendita.

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Annule tous les ordres en attente et ferme toutes les positions à l'heure "FLATAFTER"

DEFPARAM FLATAFTER = 173000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 153000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 173000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = RSI[14](close)

c1 = (indicator1 CROSSES OVER 30)

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and ordersCountL < maxOrdersL THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

indicator2 = RSI[14](close)

c2 = (indicator2 CROSSES UNDER 70)

IF c2 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and ordersCountS < maxOrdersS THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

//---------------------------------------------------------------------------------------------------------------

//Max-Orders per Day

once maxOrdersL = 1 //long

once maxOrdersS = 1 //short

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//------------------------------------------------------------------------------------------------------------------------

// Stops et objectifs

SET STOP pTRAILING 31

SET TARGET pPROFIT 11

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 5 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 10 //10 Pip chunks to increase Percentage

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.100 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 7 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF