Dear PRT users

I have adapted a code from this website to suit my needs. The strategy I intend to trade is that I would like to trade the breakout of a range during the first 5 minutes of the Dow Jones session (153500h GMT +1 time). The range is determined by the 15 minutes preceding the session. Stop loss is the range+2 pts and target is the range*5.7. This strategy has given satisfying results when traded manually since September 2020 and automatically until July 2021. I have thus started playing around with the time allowed to open a position by increasing it from 153500 GMT+1 to 154500h and the results look much more stable. However, now I am unsure if the strategy is curve fitted. In PRT I used the maximum amount of data (15k units) in the 15 minute time frame. Walk forward testing shows various efficiency levels.

If someone who is more proficient in walk forward testing and optimizing could give their comments and thoughts, it would be really helpful.

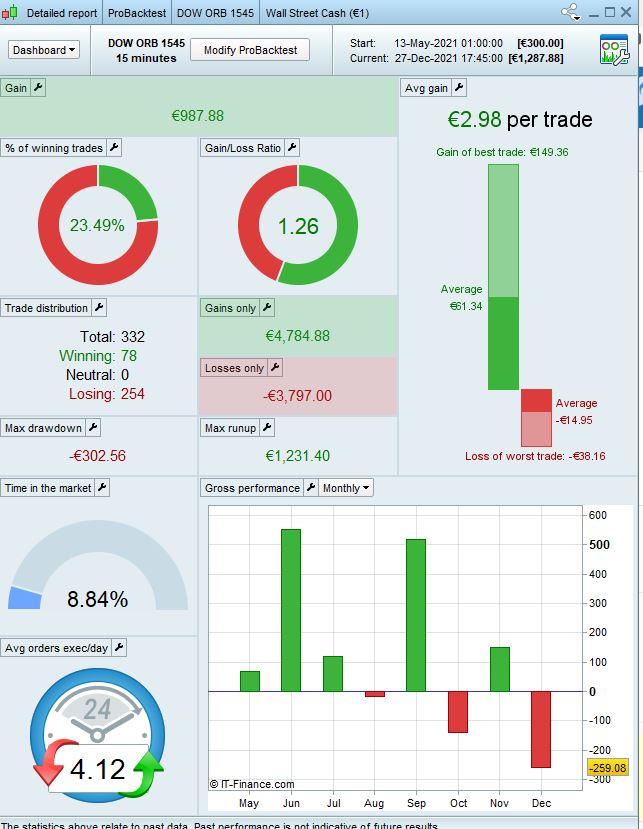

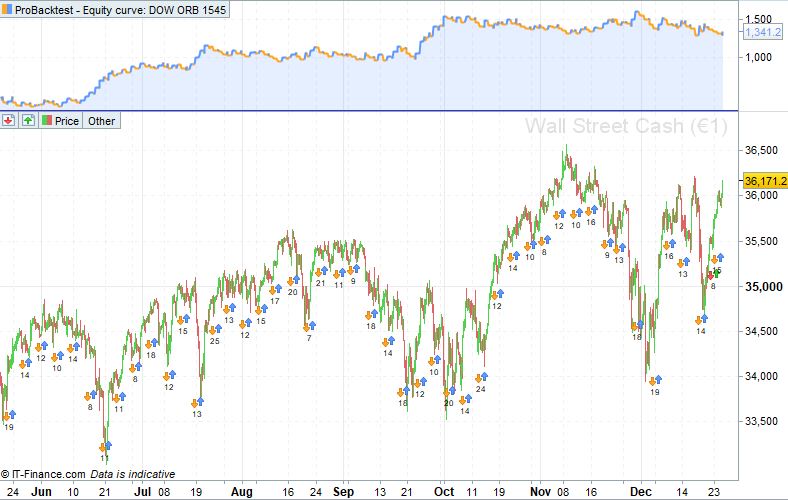

As you can see in the two attached images, the equity curve is very even, which is why I suspect it to be overfit. In the report you may see the starting and ending equity as per backtest.

//-------------------------------------------------------------------------

// Main code : DOW ORB 1545

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// DOW simple breakout during first 15 minutes of open market and all day open

//-------------------------------------------------------------------------

Defparam cumulateorders = false

Defparam flatafter = 210000

n = 0.4

IF Time = 153000 THEN

top = highest[1](high)

bottom = lowest[1](low)

amplitude = top - bottom

buytime = 0

selltime = 0

ENDIF

if Time > 151500 AND Time <= 154500 THEN

IF buytime = 0 THEN

buy n share at top stop

ENDIF

IF selltime = 0 THEN

sellshort n share at bottom stop

ENDIF

ENDIF

If longonmarket THEN

buytime = 1

ENDIF

IF shortonmarket THEN

selltime = 1

ENDIF

set stop ploss amplitude+2

set target pprofit amplitude*5.7