Let’s start today on version 17, I try to control the gains and losses per day in order to compare them to my daily risk which in this example is 10€ with the following variable : MyJPYDayProfit

it is first transformed into euros in the variable MyEuroDayProfit and then used in the DayLostCondition on line 57

A very simple example:

If for example during the day I have lost 15 € then I compare with my variable MaxLostPerDay who is 10 € :

DayLostCondition = -15 >= -10€ = FALSE, So I can’t buy more

I get the StrategyProfit value of the last day in the variable MyLastDayProfit to compare it to the candlestick profit today,

My problem is : when I have been in a position for the last day so I can’t count today’s gains and profits only, without including last days gains

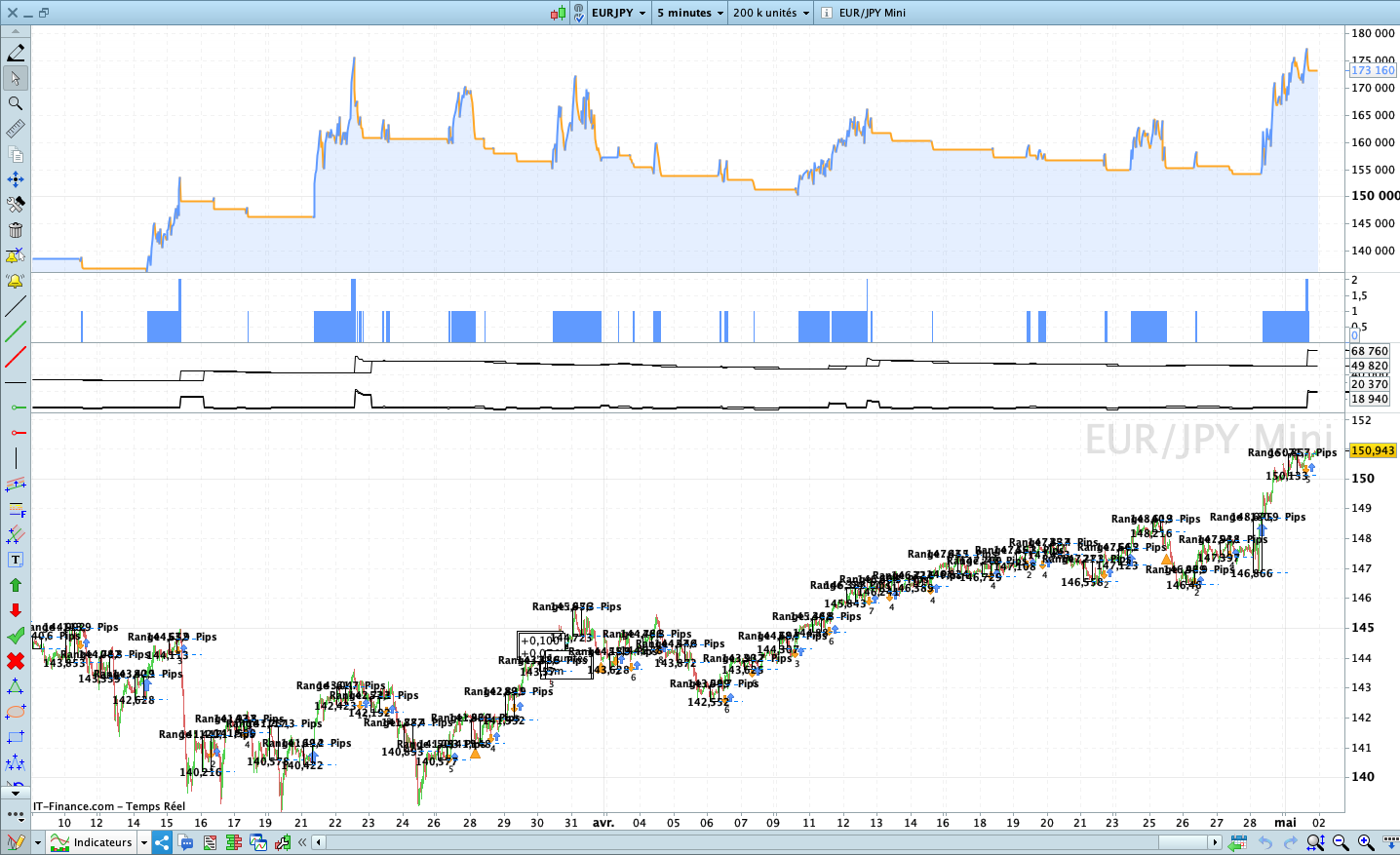

I have attached a picture and you can see that I have circled the first trade of the day, the variable MyJPYDayProfit should be losing but it is positive ( MyJPYDayProfit = 5130) because it takes into account the gains of the positions opened yesterday

// Strategy Name : END OF DAY - YEN // Version : 17.0

// Stroks : USD/JPY Mini // indicator associate : Tokyo Box v2

// Time Zone / TF : Paris-France (GTM+2) / M5 // Pip Value : 1 Pip = 100 JPY

// Tokyo Session : 9Am - 3Pm (UTC+9) //

// Spread : 2 //

// Information :

//#******************************************************************#

//# VariableS #

//#******************************************************************#

Once Capital = 100000

Once Equity = Capital

Once TrailinStop = 0 //1 on - 0 off // Needs to be improved

Once BreakEaven = 1 //1 on - 0 off

Once BreakRange = 1 //1 on - 0 off

Once MFE = 0 //1 on - 0 off // Needs to be improved

Once DrawDownQuit = 0 //1 on - 0 off // Needs to be improved

Once MaxBuyPerDay = 15 // Maximum shares we can buy per day // Z2

Once MaxLostPerDay = 10 // We can buy until we don't lost 10€ per Day // Unit : €

Once MaxBuyShare = 10 // Maximum of shares we can buy (Marging math)

Once PercentOfBoxSL = 10 // Percent of Tokyo Box for Initialization the First Stop Loss

Once N = 1 // Buy N Shares

Once Spread = 2 // Spread fees x 2

FranceDstTime = Month=4 OR Month=5 OR Month=6 OR Month=7 OR Month=8 OR Month=9 OR (Month=9 AND Day < 24) // Z5

FranceWinterTime = Month=11 OR Month=12 OR Month=1 OR Month=2 OR (Month=3 AND Day < 24) // Z5

//#******************************************************************#

//# FonctionS #

//#******************************************************************#

IF FranceDstTime THEN // Cc

IntraDayBarIndexStart = 98

IntraDayBarIndexEnd = 23

ELSIF FranceWinterTime THEN

IntraDayBarIndexStart = 86

IntraDayBarIndexEnd = 11

ENDIF

IF IntraDayBarIndex = IntraDayBarIndexStart THEN // Ac & Cc

x2 = BarIndex[0]

x1 = BarIndex[74]

yH = Highest[72](High[2])

yL = Lowest [72](Low[2])

DayRange = (yH - yL) / pipsize

ENDIF

IF NOT OnMarket THEN // Dc

FirstSL = 0

ENDIF

IF IntraDayBarIndex = 24 THEN // Ec

CountOfPurchase = 0 // Z3

MyLastDayProfit = StrategyProfit // Unit : JPY

LastDayCountOfPosition = CountOfPosition // Kc

ENDIF

MyJPYDayProfit = StrategyProfit - MyLastDayProfit // Unit : JPY

MyEuroDayProfit = MyJPYDayProfit / Medianprice // Unit : €

DayLostCondition = MyEuroDayProfit > MaxLostPerDay*(-1) // Jc & Z7

// Ex : (-300JPY/143) > 10€ x -1 ==> -2,10€ > -10€ => Boolen = True / -15€ > -10€ => False

TimeCondition = (Time > 081000 AND Time < 200000 AND DayOfWeek < 5) OR (Time > 081000 AND Time < 170000 AND DayOfWeek = 5) // Tc

LongSignal = TimeCondition AND Close Crosses Over yH // Lc

IF LongSignal Then // Lc

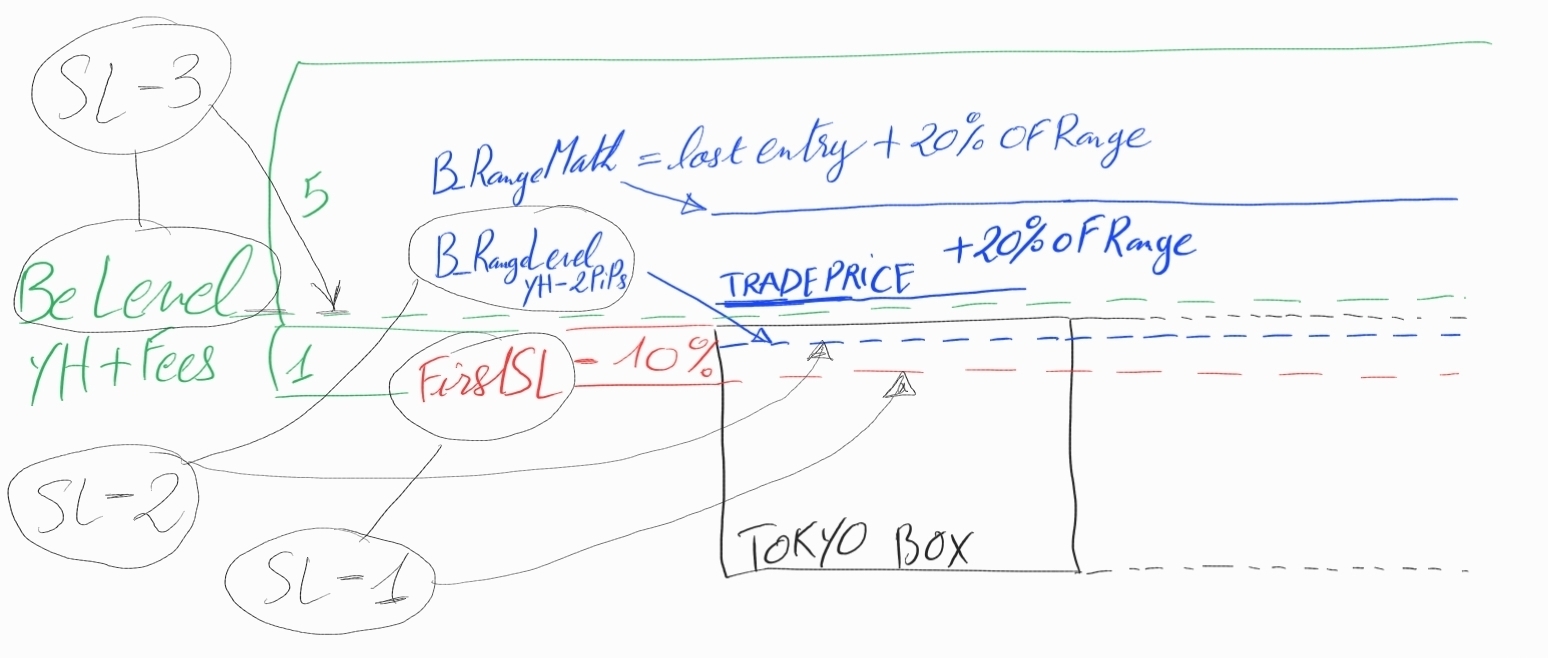

FirstSL = yH - (((yH-yL)/100)*PercentOfBoxSL) // Hc

OldFirstSL = FirstSL

ENDIF

IF TimeCondition AND Not OnMarket THEN

LastDayCountOfPosition = 0

ENDIF

if TimeCondition then // Tc

LongSignalAllCondition = LongSignal AND CountOfPurchase < MaxBuyPerDay AND CountOfLongShares < MaxBuyShare AND DayLostCondition AND (CountOfPosition <= LastDayCountOfPosition) AND ((((Close - FirstSL)*100) / pipsize) / MedianPrice < MaxLostPerDay)

IF LongSignalAllCondition THEN

Buy N Contract AT Market

SET STOP PRICE FirstSL

ENDIF

endif

IF (OnMarket AND Not OnMarket[1]) OR (ABS(CountOfPosition) > ABS(CountOfPosition[1])) THEN

CountOfPurchase = CountOfPurchase + 1

ENDIF

//#******************************************************************#

//# Trailing & BreakEven & Range Stop Loss & MFE #

//#******************************************************************#

Once trailingstart = 140 // Trailing start after X pips profit

Once trailingstep = 10 // Trailing step to move the "stoploss"

Once StartBERatio = 5 // BE Start for the hole position when the RR(FirstSL) = 5

Once StartBreakRangePercent = 20 // Close > Last entry + 20% of the Tokyo Box

Once PointsToKeep = 2*Spread // Spread to add to BE price

Once TRAILINGMFE = 20 // Trailing stop with the Max Favorable Excursion

// Trailing

if TrailinStop > 0 then // Needs to be improved

IF NOT ONMARKET THEN

NewSL=0

ENDIF

IF LONGONMARKET THEN

// Trailing Start

IF NewSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

NewSL = tradeprice(1)+trailingstep*pipsize

ENDIF

// Trailing Step Move

IF NewSL>0 AND close-NewSL>=trailingstep*pipsize THEN

NewSL = NewSL+trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF NewSL>0 THEN

SELL AT NewSL STOP

ENDIF

endif

// Range Stop Loss

if BreakRange > 0 then // Fc

IF Not OnMarket THEN

BreakRangeLevel = 0

ENDIF

IF LongOnMarket THEN

BreakRangeMath = TradePrice + (((yH-yL)/100)*StartBreakRangePercent)

ENDIF

IF LongOnMarket AND Close Crosses Over BreakRangeMath THEN // Z1

BreakRangeLevel = yH - 2*Pipsize // Gc

//FirstSL = 0

ENDIF

IF BreakRangeLevel > 0 THEN //Z8

SELL AT BreakRangeLevel STOP

ENDIF

endif

// BreakEven Stop Loss

if BreakEaven>0 then

IF Not OnMarket THEN

BreakEvenLevel = 0

ENDIF

yHplusFirstSL = yH + (StartBERatio*(yH-OldFirstSL))

IF LongOnMarket AND Close Crosses Over yHplusFirstSL THEN

BreakEvenLevel = TradePrice + PointsToKeep*pipsize

ENDIF

IF BreakEvenLevel > 0 THEN

SELL AT BreakEvenLevel STOP

ENDIF

endif

if MFE > 0 then // Needs to be improved

if not onmarket then

MAXPRICEMFE = 0

MINPRICEMFE = close

priceexitMFE = 0

endif

if longonmarket then

MAXPRICEMFE = MAX(MAXPRICEMFE,close) //saving the MFE of the current trade

if MAXPRICEMFE-tradeprice(1)>=TRAILINGMFE*pointsize then //if the MFE is higher than the trailingstop then

priceexitMFE = MAXPRICEMFE-TRAILINGMFE*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

if onmarket and priceexitMFE>0 then

SELL AT priceexitMFE STOP

endif

endif

//#******************************************************************#

//# Graph #

//#******************************************************************#

// Blue Azur (0, 127, 255) & Maya (115, 194, 251)

// Green Sinople (20, 148, 20) &

IF 0 THEN

yHplusFirstSL = yH + (5*(yH-OldFirstSL))

GraphOnPrice BreakEvenLevel AS "BreakEvenLevel" Coloured (20, 148, 20)

GraphOnPrice yHplusFirstSL AS "yHplusFirstSL"Coloured (20, 148, 20)

GraphOnPrice BreakRangeMath AS "BreakRangeMath" Coloured (115, 194, 251)

GraphOnPrice BreakRangeLevel AS "BreakRangeLevel" Coloured (115, 194, 251)

GraphOnPrice FirstSL AS "FirstSL" Coloured (233, 56, 63)

//GraphOnPrice OldFirstSL AS "OldFirstSL"

ENDIF

IF 1 THEN

LosingPerTrade = (((Close - FirstSL)*100) / pipsize) / MedianPrice

//Graph LosingPerTrade AS "Calculeeee"

//Graph 10+MyEuroDayProfit AS "Mes 10€"

//Graph LongSignalAllCondition AS "LongSignalAllCondition"

//Graph LongSignal AS "LongSignal"

//Graph yH AS "yH"

//Graph TimeCondition AS "TimeCondition"

Graph MyJPYDayProfit AS "MyJPYDayProfit"

Graph MyLastDayProfit AS "MyLastDayProfit"

Graph StrategyProfit AS "StrategyProfit"

//Graph MyEuroDayProfit AS "My Euro Day Profit"

//Graph DayLostCondition AS "DayLostCondition"

//Graph MaxLostPerDay*(-1) AS "MaxLostPerDay"

ENDIF

//#******************************************************************#

//# Stop Strategy #

//#******************************************************************#

IF DrawDownQuit Then // Needs to be improved

MaxDrawDownPercentage = 10 // Max DrawDown of x%

Equity = Capital + StrategyProfit

HighestEquity = Max (HighestEquity,Equity) // Save the Maximum Equity we got

MaxDrawdown = HighestEquity * (MaxDrawDownPercentage/100)

ExitFromMarketCond = Equity <= HighestEquity - MaxDrawdown

IF ExitFromMarketCond Then

Quit

ENDIF

ENDIF

//#******************************************************************#

//# Hello ToTo #

//#******************************************************************#

// _ _ _ _ _______ _______

// | | | | | | | |__ __|__ __|

// | |__| | ___| | | ___ | | ___ | | ___

// | __ |/ _ \ | |/ _ \ | |/ _ \| |/ _ \

// | | | | __/ | | (_) | | | (_) | | (_) |

// |_| |_|\___|_|_|\___/ |_|\___/|_|\___/

// GMT : 00H ================== 6H / UTC

// Tokyo : 09H ================== 15H / UTC + 9 / JST (Japan Standard Time)

// Paris : 02H ================== 8H / UTC + 2 / DST (Daylight Saving Time)

// Paris : 01H ================== 7H / UTC + 1 / Winter

// London : 01H ================== 7H / UTC + 1 / DST (Daylight Saving Time)

// London : 00H ================== 6H / UTC + 0 / Winter

// for Paris with Time Frame M5 :

// When is DST : IntraDayBarIndex of 8:10H = 98

// When Winter : IntraDayBarIndex of 7:10H = 86

// https://www.timeanddate.com/time/europe/

//#******************************************************************#

//# Rules : Xc = X-Condition #

//#******************************************************************#

// Ac : Tokyo Box : 9Am to 3Pm Local time (JST) = 00 to 6Am GMT

// Bc : Our Trading it's from 3Pm at Tokoy so from 8:10Am in Paris when DST / 7:10Am when Winter

// Cc : Tokyo Box based on IntraDayBarIndex with DST and Winter Time

// Dc : IF Not On Market, I reset the First Stop Loss to 0

// Ec : We reset the Count of some variable we need to use at 2Am = IntraDayBarIndex = 24,

// So in the first candle of Tokyo Box.

// And we store some variable that we will need the day after.

// Fc : Initialise the StartBreakRange with a dynmic value and not static one,

// the math is the Range value + StartBreakRangePercent%,

// Exmeple :

// Range (yH-yL) = 60Pips & yH = 142,219 & StartBreakRangePercent = 20%

// means we set the NewSL below the Highest - 2 pips (yH -2)

// 142,219 + (60Pips x 20%) = 142,219 + 12Pips = 142,339 JPY

// Gc : the idea is to put a First Stop Loss 2 pips down then the highest value of the range

// before the BreakEven level

// Hc : Initialization of the First Stop Loss, We assume that the box will be broken

// and that the break is real, so in this case we put a stop loss at 10%

// below the highest of the Tokyo Box

// Jc : if we lost more then MaxLostPerDay € (exemple 10€) per day, we Can Not buy more,

// fees not include

// Kc : We memorise the last count to position to compair to the one of today

// Mc : we set the SL to BE level + Fees (I have to chek fees for all position) when the price

// reach a RR of 5, we let the trade breath

// Tc : Time Conditions, we bay only after Tokyo Box (A) and before 8Pm for all the day of week

// exept the Day 5 = Friday we stop at 5Pm

// Lc : Long signal if we Close > the Tokyo Box and we are in TimeCondition (Tc)

//#******************************************************************#

//# Idea to be developed and questions #

//#******************************************************************#

// Z1 : I have to find a better solutoion the the Close option

// Z2 : better to control the value of this variable : MaxBuyPerDay by the money

// we can lose in 1 days, So I have to count my Profit per day

// Z3 : I noticed when the Buy and Sell order is in the same candle so the CountOfPurchase

// still the same and it's not incremented with +1

// Z5 : I have to finish this DST and Winter works

// Z6 : I add this code : "Sell CountOfPosition Shares AT FirstSL STOP" for exeit from position

// when my countofposition is more the 1, I noticed the code : "SET STOP PRICE FirstSL" not

// working is my position is more then 1 but the same code working with

// the : "SET STOP PRICE BreakRangeMath"

// Z6 : I submit this line (as in but interrogations on the execution of the SL)

// that this line does not expect the Close to be off the SL to get me out, but it

// is a tick by tick execution

// Z7 : if last day we win some money, we can allocate part of these gains to future trades,

// which will allow us to take more positions for example (N > 1)

// Z8 : I have to do a check of the orders executed before each other, Like only one Line of

// code like : SEll AT SL STOP and try to manage the value of SL

//#******************************************************************#

//# Explanation of the code #

//#******************************************************************#

// Code : (CountOfPosition = LastDayCountOfPosition OR Not OnMarket)

// - IF I'm on market I have to compare LastDayCountOfPosition like that I can't

// buy more if my Long condition = 1

// - IF my LastDayCountOfPosition so I can't compare, that is why I use OR Not OnMarket

//

// Code : ((((Close - FirstSL)*100) / pipsize) / MedianPrice < MaxLostPerDay)

// We Calculate the distance between the Close and the FirstSL,

// and This amount should be smaller than what you are willing to lose per day, exemple :

// Close-FirstSL = 18Pips but we can lost maximum 10€/Day => 10€ = 14,3 Pips

//#******************************************************************#

//# Last programming where I stopped at #

//#******************************************************************#

//