Bonjour fifi743,

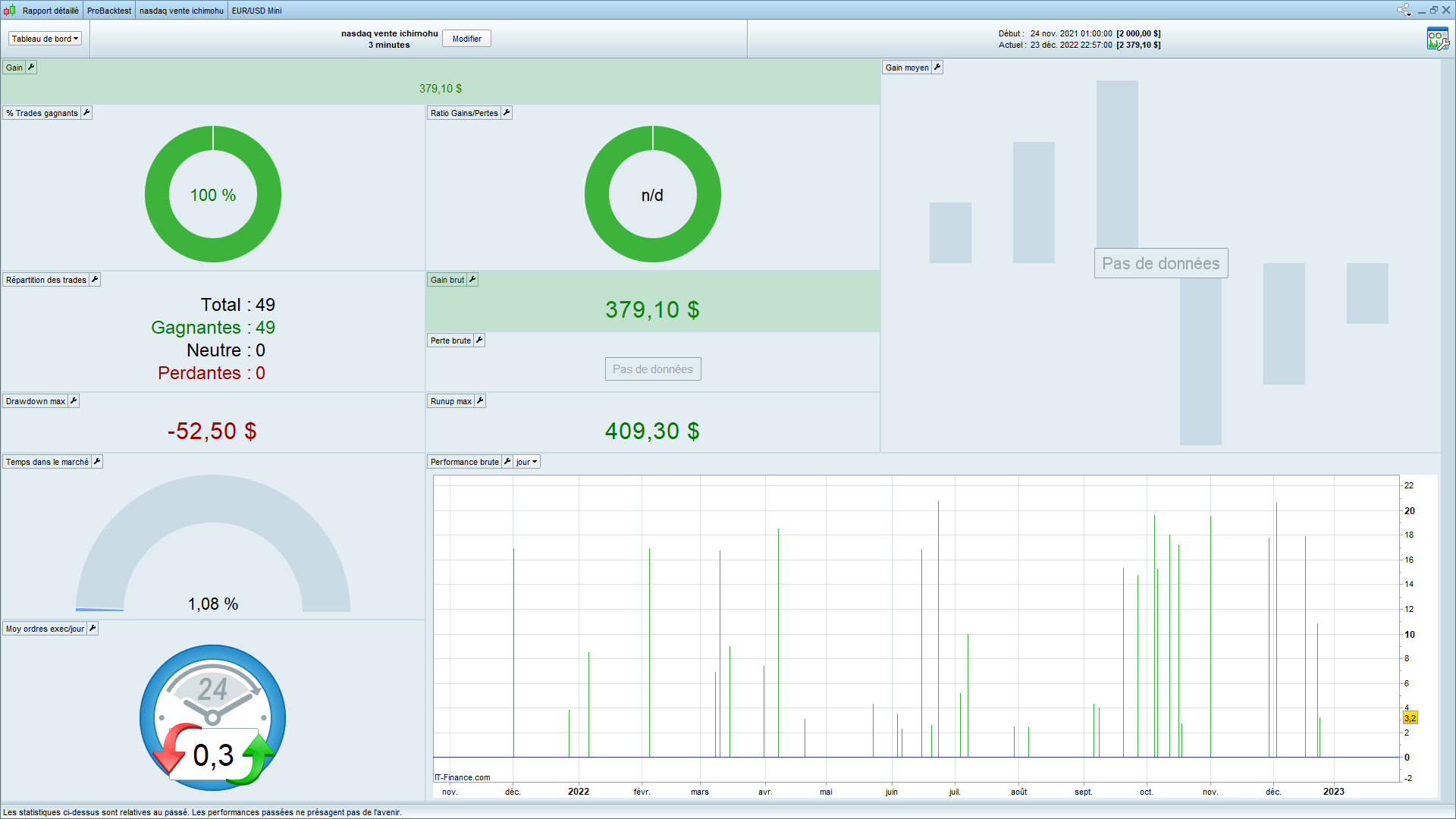

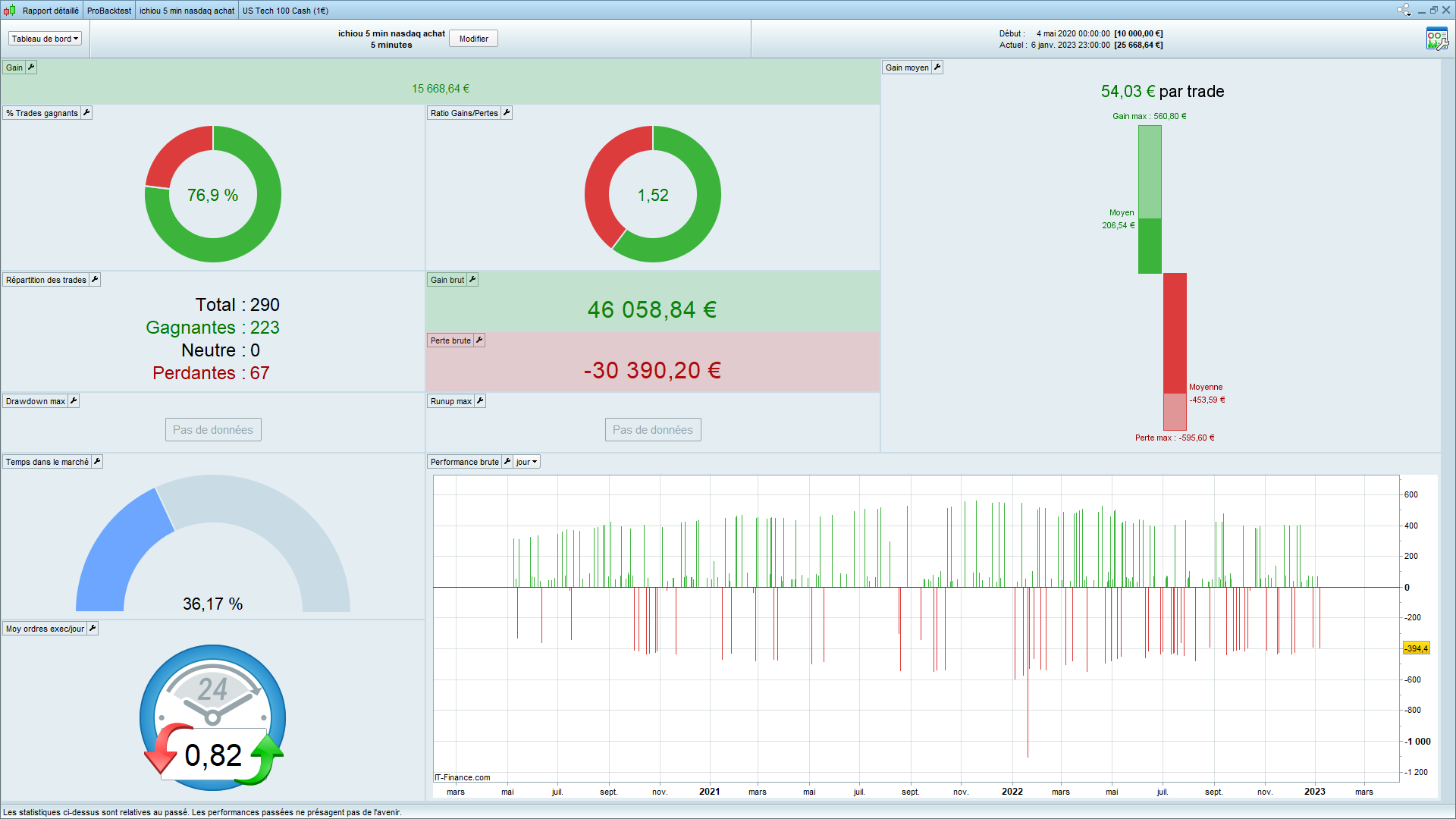

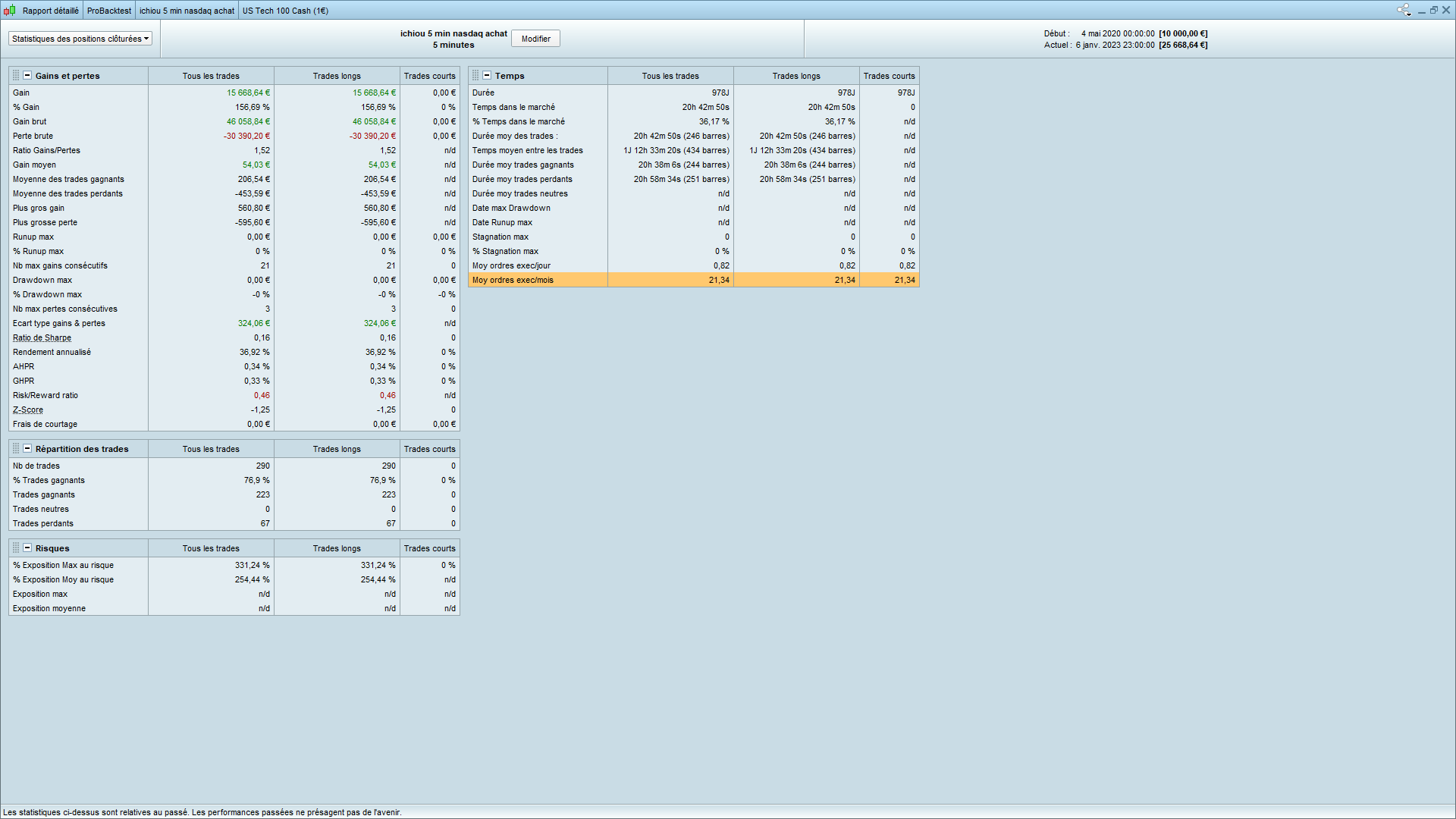

Voici mon petit algo sur le nasdaq 5 minutes basé que sur l’achat ( merci à nicolas et robertto au passage pour leur travail sur le breakeven).

Tu pourras voir il prend 2 contrats par trade, possibilité de l’améliorer .

Par exemple je ne comprend pas pourquoi je n’ai que des trades long.

Mais si tu veux y jeter un oeil et avec la communauté peut être que le résutat peut être meilleur.

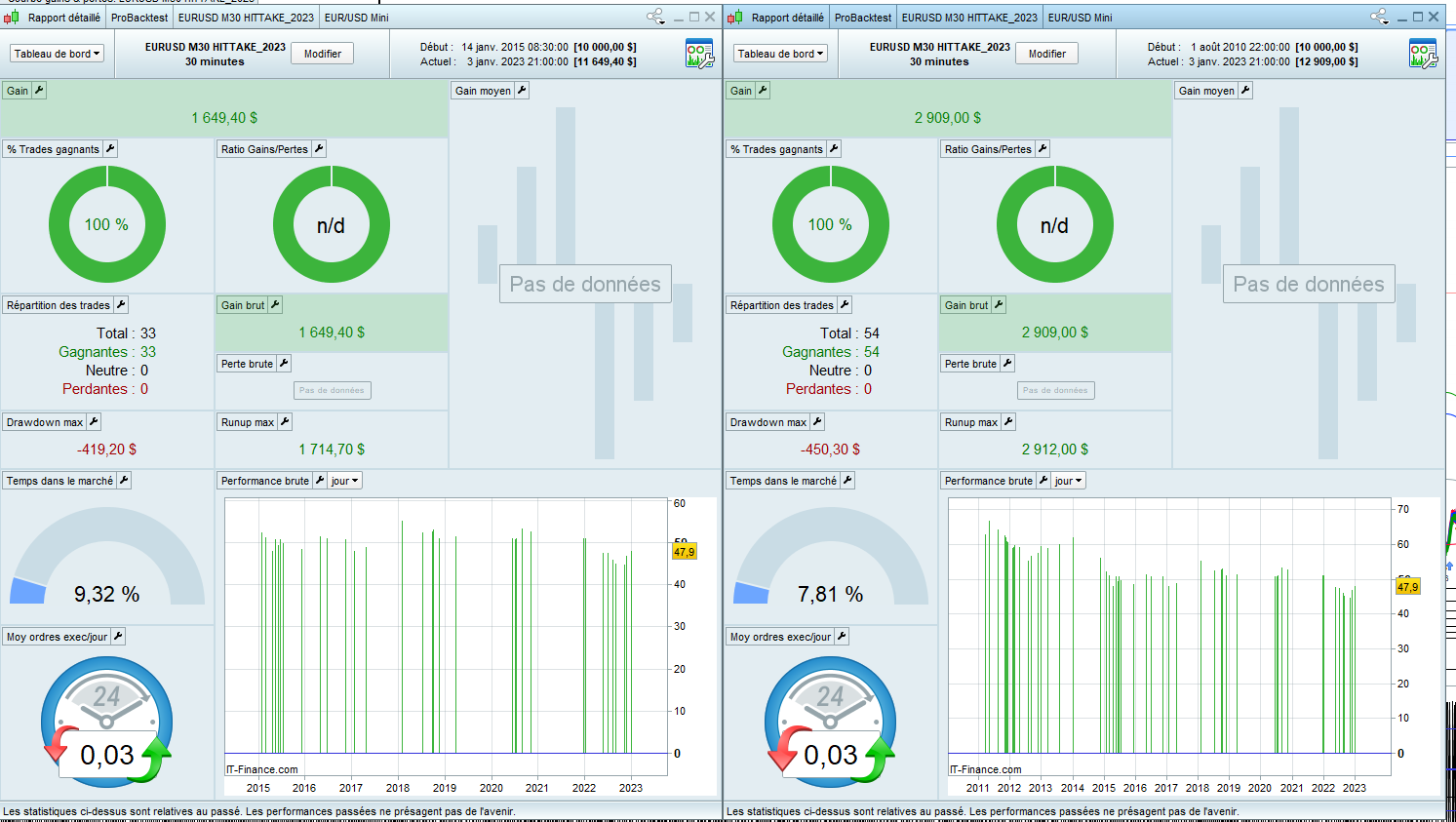

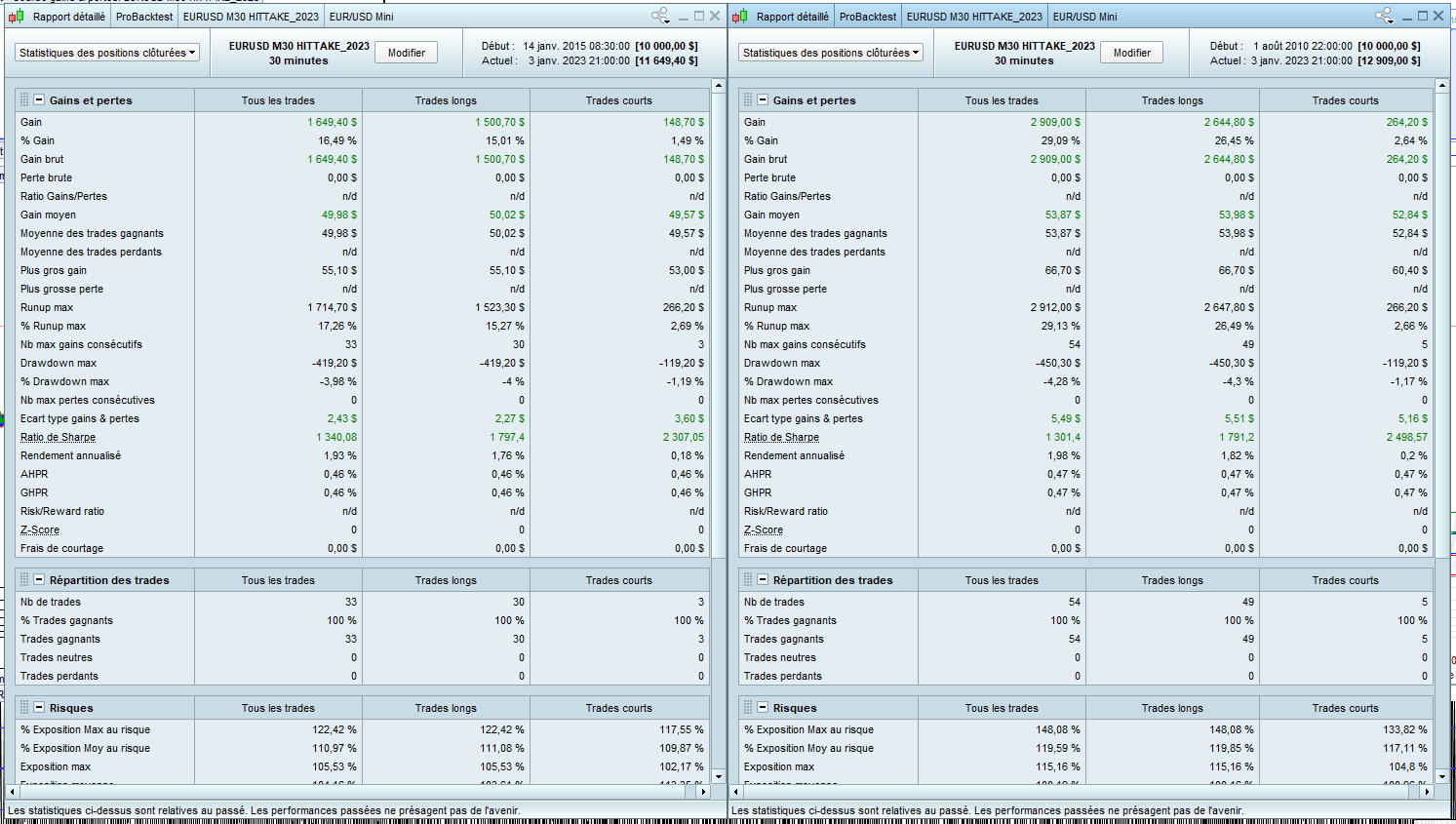

Au niveau des conditions tu peux mettre C3 ou ne pas le mettre les résultat sont différents mis intéressants.

Il y a une année pas terrible l’annee 2022.

Je te joint aussi avec la C3.

// Définition des paramètres du code

DEFPARAM CumulateOrders = false // pas de cumul de positions

DEFPARAM Preloadbars = 1000000

capital= 50000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 150000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 223000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = SenkouSpanA[9,26,52]

c1 = (close CROSSES OVER indicator1)

indicator2 = SenkouSpanB[9,26,52]

c2 = (close CROSSES OVER indicator2)

c3 = (close > DOpen(0)[1])

IF (c1 AND c2 ) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 2 CONTRACT AT MARKET

partial=0

ENDIF

// sortie partielle

if longonmarket and positionperf>1.7/100 and partial=0 then

sell countofposition/9.7 contract at market

partial = 1

endif

if summation[1800](longonmarket)=1800 then

sell at market

endif

if summation[1000](shortonmarket)=1000 then

exitshort at market

endif

// Stops et objectifs

set stop %loss 1.8

set target %profit 1.73

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 65 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF