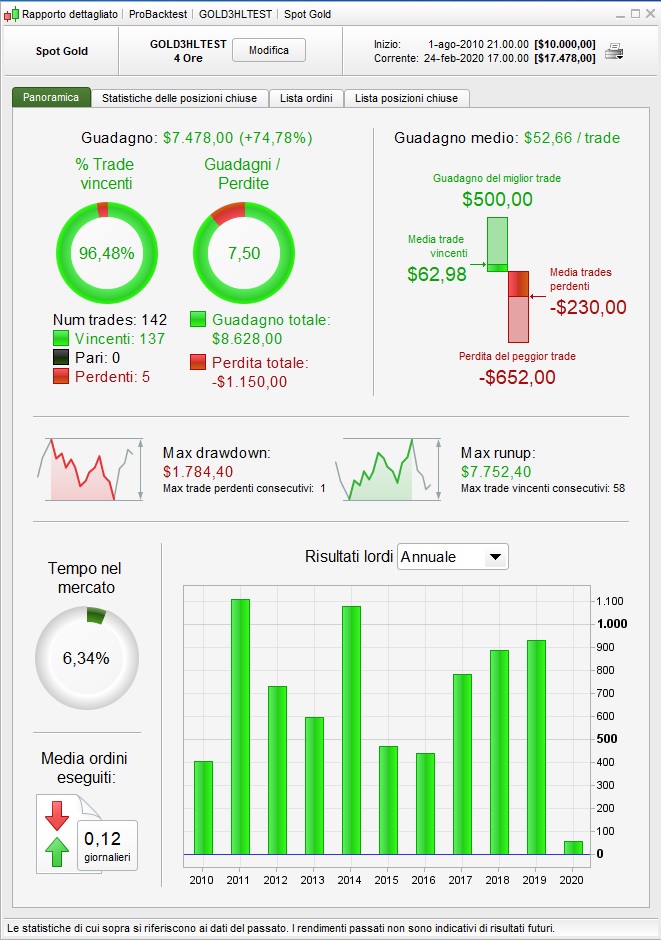

Noticed that there are no systems on Gold, so i tryed to develop one by myself.

Here’s what i got, simple and effective

Based on a simple moving average and a Breakeven function, with a limit to the operative time.

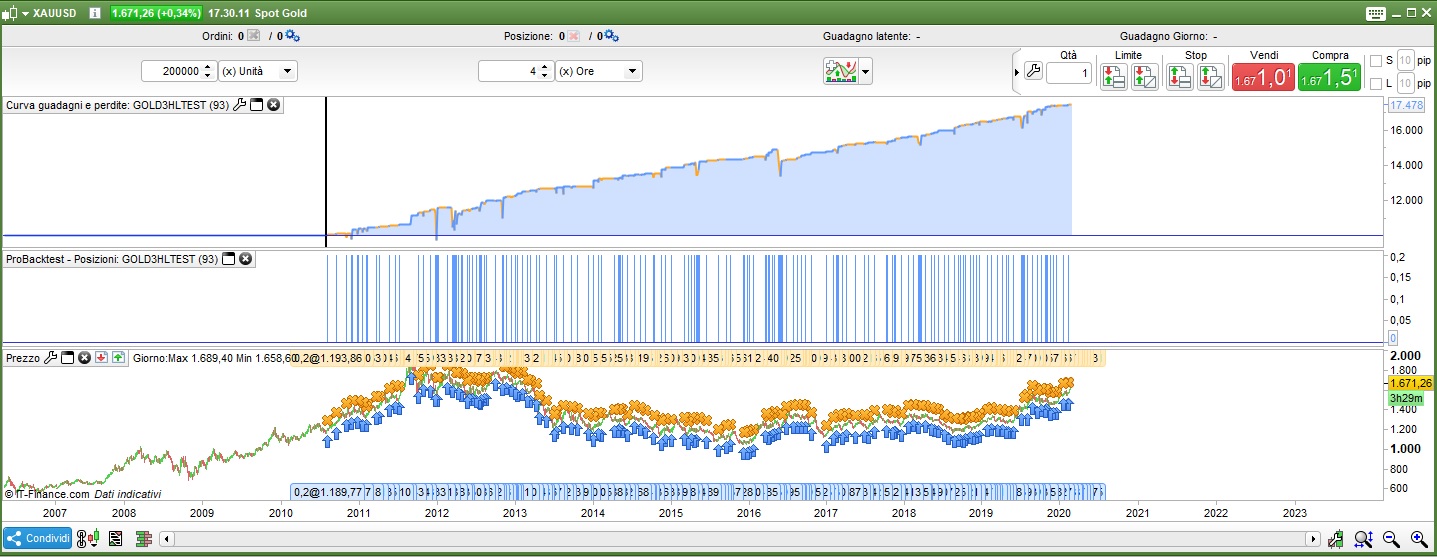

Works on 4H.

You should also post the whole code so that some interested may take a look at it without having to import it.

Thank you. 🙂

Usually didn’t seen anyone doing that, but here it is 😉

defparam cumulateorders = false

// Long

If average[20] CROSSES OVER average[55] THEN

BUY 0.2 CONTRACTS AT MARKET

ENDIF

// Stop and target

SET STOP pLOSS 0

SET TARGET pPROFIT 25

IF OnMarket AND (BarIndex - TradeIndex) >=93 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

StartBreakeven = 0 // How much pips/points in gain to activate the Breakeven function?

PointsToKeep = 20 // How much pips/points to keep in profit above of below our entry price when the Breakeven is activated (beware of spread)

// Reset the BreakevenLevel when no trade are on market

IF NOT ONMARKET THEN

BreakevenLevel=0

ENDIF

// Test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

// Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

SELL AT BreakevenLevel STOP

ENDIF

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

EXITSHORT AT BreakevenLevel STOP

ENDIF

You may have noticed code is usually not posted on large topics because people already know know what’s it all about and posting code everytime would make the topic difficult to read, but the first time it’s better to let the reader decide whether it is worthwhile or not (for him) importing it.

Thank you.

I was talking about first posts of new topics that i’ve seen recently, but doesn’t matter, it was what it was 🙂

It’s surely more smart put the entire code in the first post for the reasons you listed.

I always like to see the code in the first post as I don’t always have my platform open 24/7 and so seeing how the strategy is coded is a lot of hassle of opening the platform and importing the code and I am generally to busy to bother doing that. If the code is in the first post however then I am able to immediately check it out and see if it is of interest or if I have anything to comment that might assist.

Small alteration to your exit conditions:

IF OnMarket AND (BarIndex – TradeIndex) >=93 and close>positionprice THEN …

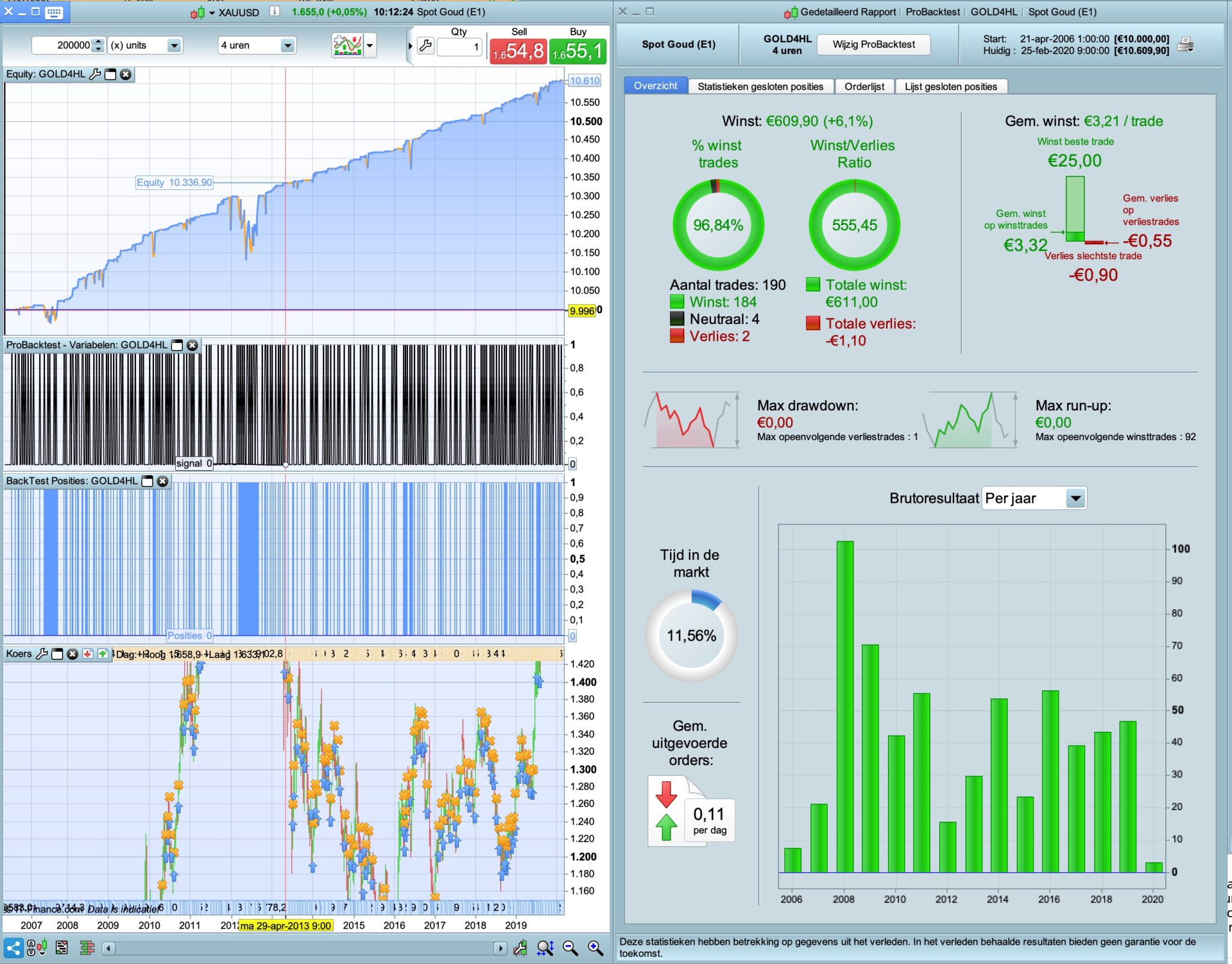

Makes a huge difference on 100k — gain/loss ratio of 370? worst trade -$4? seriously?

Probably worth re-optimizing the bar number.

Makes a huge difference on 100k — gain/loss ratio of 370? worst trade -$4? seriously?

Yes but one day you will open a trade at the top of the market and then the market will take a dive and you will go into massive account killing drawdown! Just because it does not happen in your backtest does not mean it can’t happen. Perhaps a robustness test would show this as perhaps the big DD trades are just not happening because of the start date and time meaning that you just so happened to be on the market and so missed those bad trades.

Yes, the tone of voice was meant to imply that this may well be too good to be troo and needs more testing … it’s effectively only closing if in profit. But may be worth considering …

Paul

PaulParticipant

Master

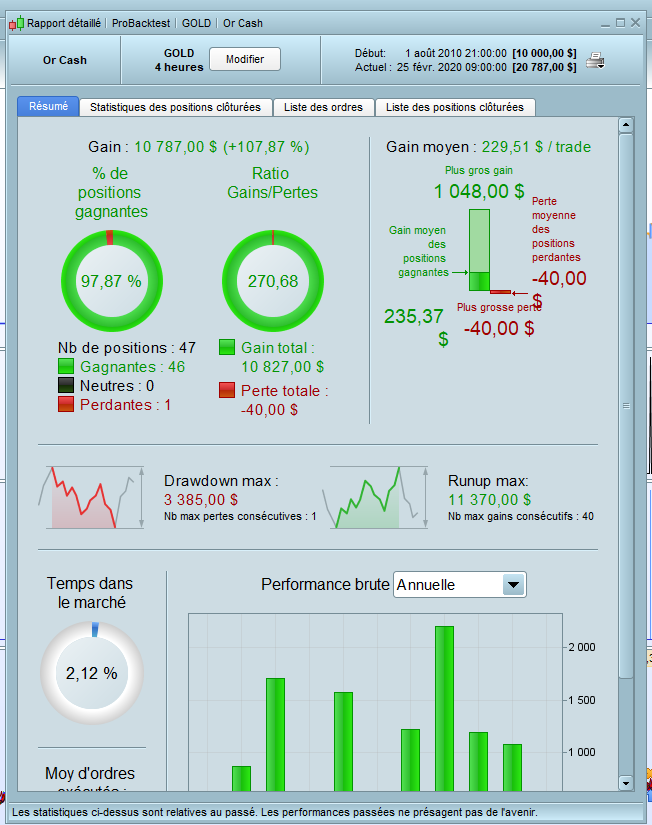

added re-entry to see what it does, kind of a robustness-test

defparam cumulateorders = false

once reentry =1 // close & re-entry on signal in same direction

condbuy=average[20] CROSSES OVER average[55]

if condbuy then

signal=1

else

signal=0

endif

graph signal

ctime=1

// Long

if ctime then

If condbuy THEN

if not onmarket then

buy 1 contract at market

endif

if reentry then

if longonmarket then

sell at market

endif

endif

endif

if reentry then

if condbuy[1] then

if longonmarket[1] then

buy 1 contract at market

endif

endif

endif

endif

// Stop and target

SET STOP pLOSS 0

SET TARGET pPROFIT 25

IF OnMarket AND close>positionprice and (BarIndex - TradeIndex) >=1 THEN

SELL AT MARKET

ENDIF

StartBreakeven = 0 // How much pips/points in gain to activate the Breakeven function?

PointsToKeep = 20 // How much pips/points to keep in profit above of below our entry price when the Breakeven is activated (beware of spread)

// Reset the BreakevenLevel when no trade are on market

IF NOT ONMARKET THEN

BreakevenLevel=0

ENDIF

// Test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

// Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

SELL AT BreakevenLevel STOP

ENDIF

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

EXITSHORT AT BreakevenLevel STOP

ENDIF

the breakeven though should be the other way around with it’s value’s

when reaching a gain, then move breakevenlevel to 0, however it’s a nice equitycurve this way.

Probably worth re-optimizing the bar number.

This is a terrible idea. Optimising on any time based idea is always going to be a great way to curve fit. As soon as I see numbers like 93 it instantly gets me worried that it is totally curve fitted.

As soon as I see numbers like 93 it instantly gets me worried that it is totally curve fitted.

But surely there must always be some optimal number, no? where optimal does not necessarily mean highest profit, could be lowest drawdown or %win or whatever helps you sleep at night.

I don’t think there’s a good ‘theoretical’ reason for it not to be 93 or 71 or 57, esp in a 10 year backtest with WF and all the rest. Or is there?

defparam cumulateorders = false

once reentry =0// close & re-entry on signal in same direction

condbuy=average[20] CROSSES OVER average[55] and (average[55]-average[55](close[1]))/pointsize> 0.1

if condbuy then

signal=1

else

signal=0

endif

graph signal

ctime=1

// Long

if ctime then

If condbuy THEN

if not onmarket then

buy 1 contract at market

endif

if reentry then

if longonmarket then

sell at market

endif

endif

endif

if reentry then

if condbuy[1] then

if longonmarket[1] then

buy 1 contract at market

endif

endif

endif

endif

// Stop and target

SET STOP pLOSS 0

SET TARGET pPROFIT 25

IF OnMarket AND close>positionprice and (BarIndex - TradeIndex) >=1 THEN

SELL AT MARKET

ENDIF

StartBreakeven =0// How much pips/points in gain to activate the Breakeven function?

PointsToKeep = 20 // How much pips/points to keep in profit above of below our entry price when the Breakeven is activated (beware of spread)

// Reset the BreakevenLevel when no trade are on market

IF NOT ONMARKET THEN

BreakevenLevel=0

ENDIF

// Test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

// Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

SELL AT BreakevenLevel STOP

ENDIF

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//Calculate the BreakevenLevel

BreakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//Place the new stop orders on market at BreakevenLevel

IF BreakevenLevel>0 THEN

EXITSHORT AT BreakevenLevel STOP

ENDIF

Hello,

Or add a filter

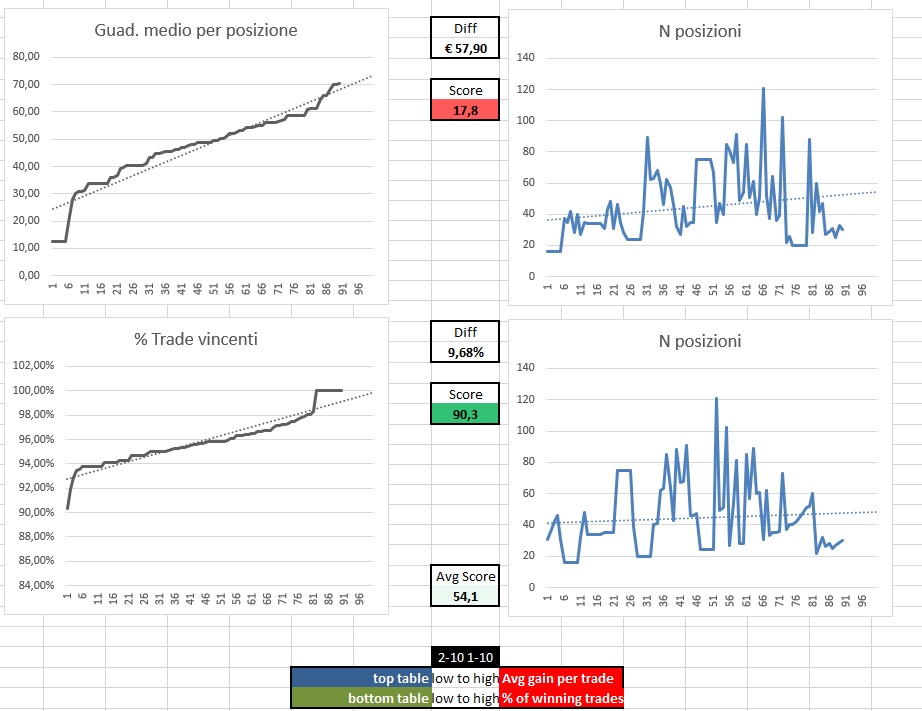

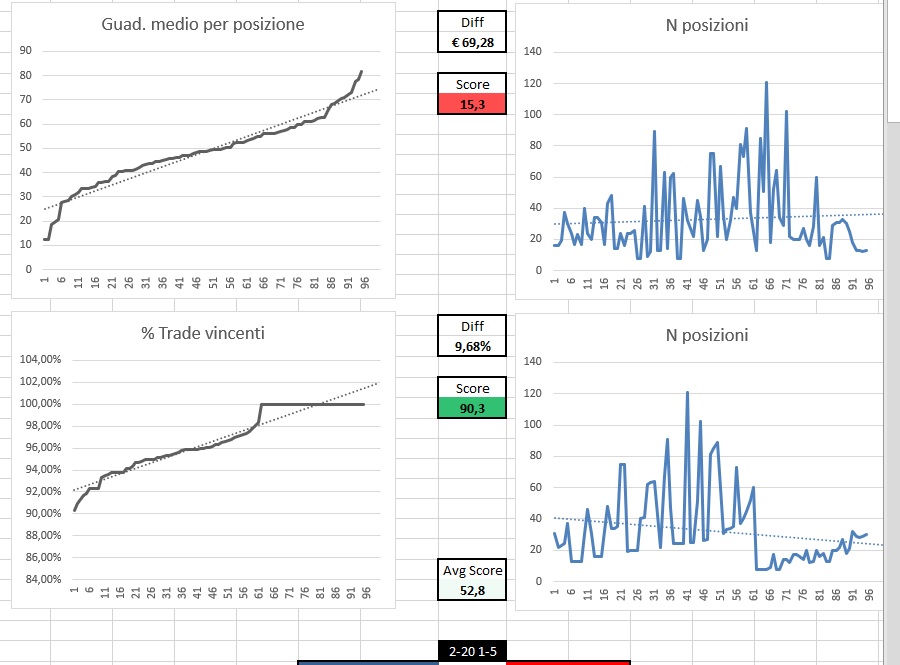

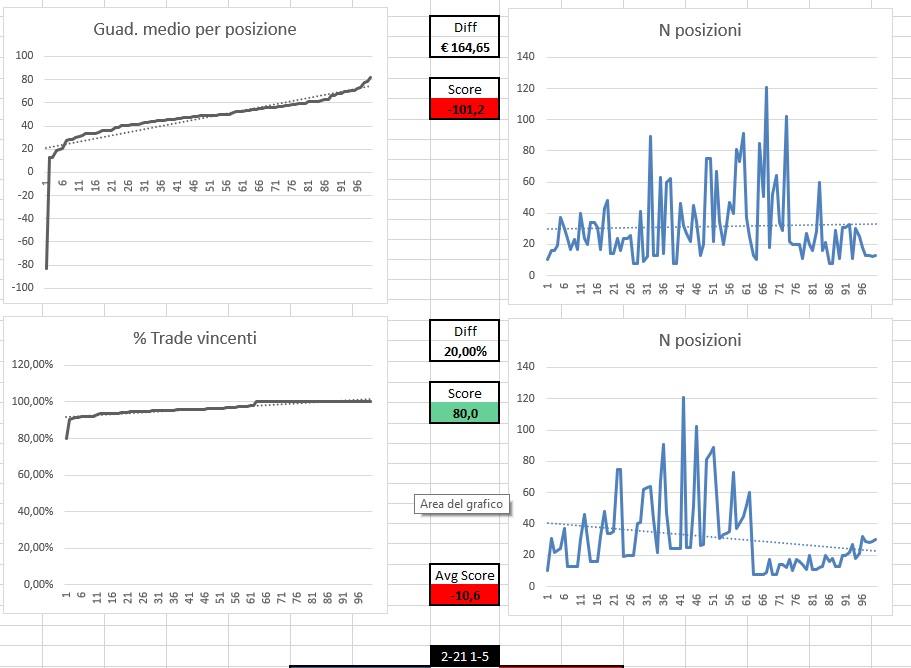

Robustness test results, nothing to do here 🙁

Thanks to @paul for the excel file

But surely there must always be some optimal number, no?

Yes – but that optimal number is your curve fit. You have looked at history and said ‘that number of bars before exiting has worked the best in the past’ but that does not mean that it will work tomorrow or ever be the best number to use ever again. Now if you had say a range of numbers from 83 to 103 that all worked pretty similarly and all returned nice equity curves then picking 93 slap bang in the middle of that range might put you in with a fighting chance that it will continue to work even if 93 was not the best result or best equity curve.