Hi Guys. I have been following this post for quite some time- left it and came back. This weekend I read the whole post again and decided to begin some demo trades on the manual part.

I must say that since it’s a long development process with lots of try-outs, one easily gets lost if you weren’t really testing all the codes along with the developments, which I didn’t. Big applause for both Nikolas and CFTA. Great team work and effort to achieve what has been done. I apologies in advance if I forgot something in the long post, or obvious noob questions that may come.

Two things I’d like to achieve.

Code and Entry. With the entry part I’d like to make the screener or indicator, also to better to understand the setup- filtering out all the information here and on forexfactory. Boiling it down to a few simple lines.

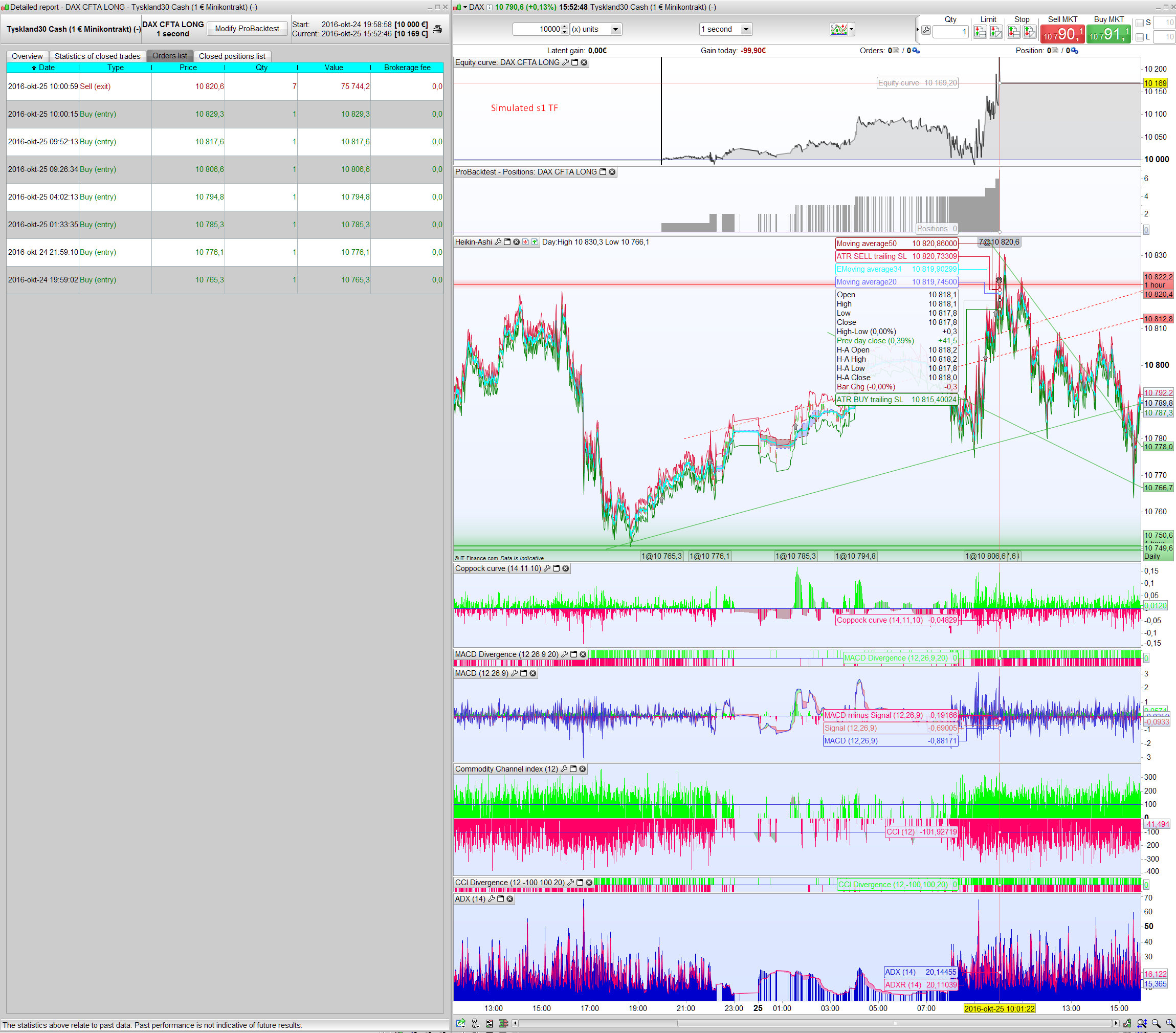

I made 3 trades with the same code. There are still findings that I think needs to be addressed or at least explained.

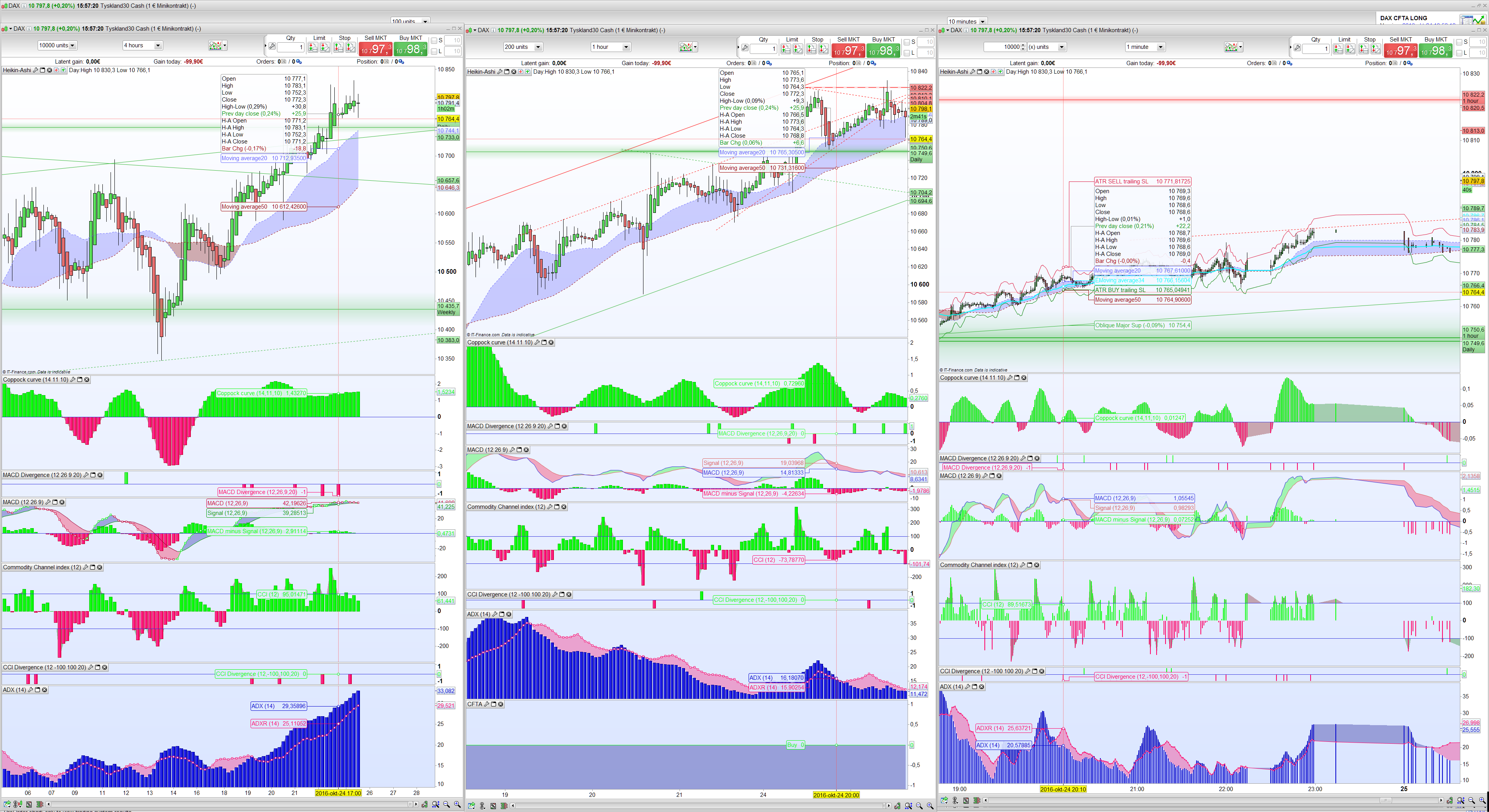

The first DAX trade. The other has similar errors. The third is running as designed.

As you can see on the screen dumps I have a TF 4H, 1H and 1min. The code is executed on a 1 sec TF.

Entry at 24 Oct 20:10 It looks like there was a retracement before going long again. I see this on the 1H TF. It was not matching the setup according to CFTA but I thought there was more in the DAX to trade it. It would also leave me with a test trade.

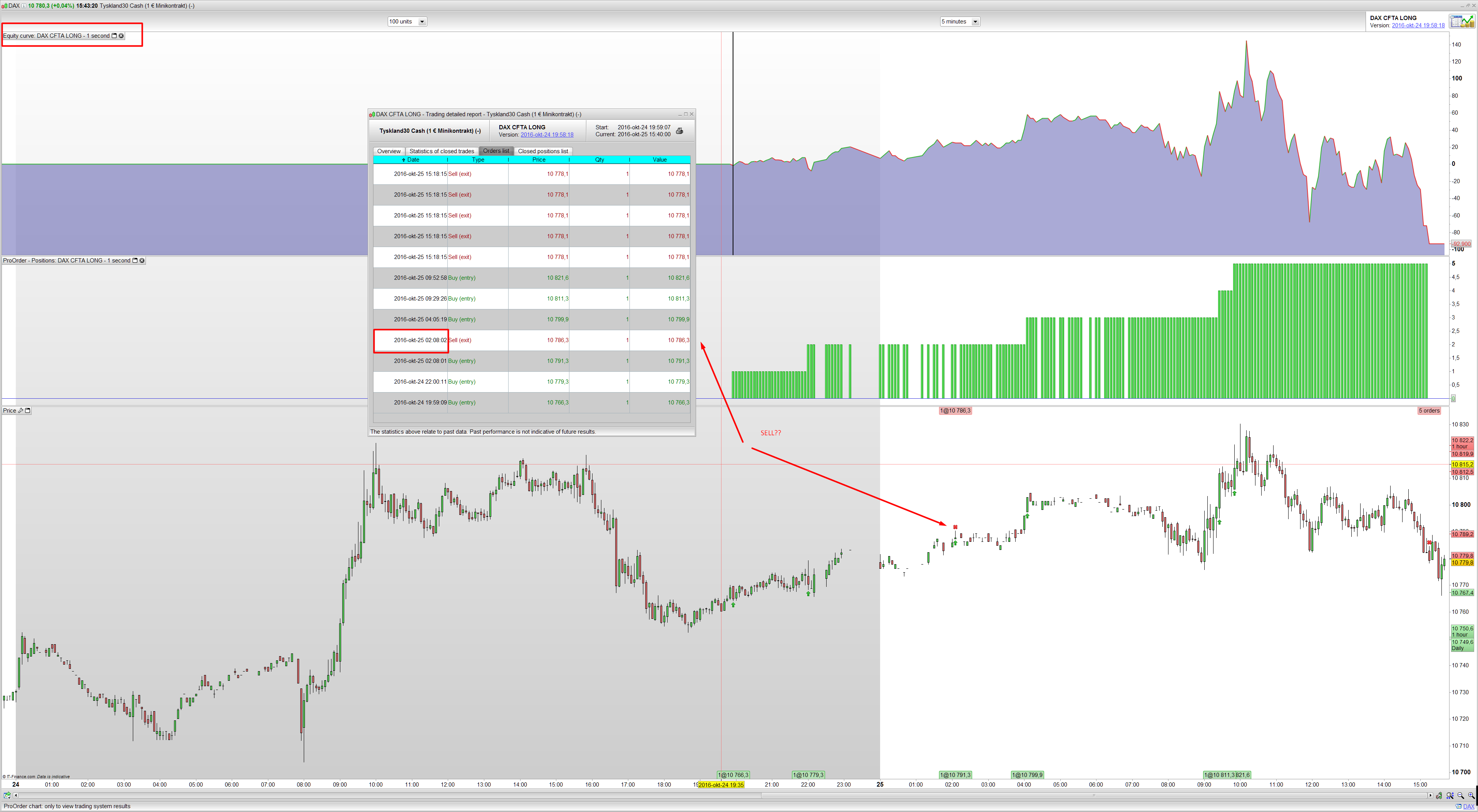

Anyway If I simulate or back tested this It would leave me with a profit- however the real trade did leave me with a 1% loss.

I decided to go with 1% risk and RR=2 which should leave me with 200eur if won or -100eur if loosing.

Simulated trades on 1s TF wins with 169 EUR and 1m TF wins with 116 EUR, but the demo proorder looses with 100 EUR.

Shouldn’t it still loose in the simulation because of the rr=2?

Also around 02:08 it closes 1 position of the 3 in the trade?

Why this behaviour?

I tried to read the forexfactory link but I didn’t think the description of how to enter the trade was clear to me. Perhaps because I’m not familiar with MT4 and some of the indicators there and also that I’m still generally new to trading. So this is what I came up with from this post. I tried to setup the indicators from one of CFTA’s screen dumps.

Long entry

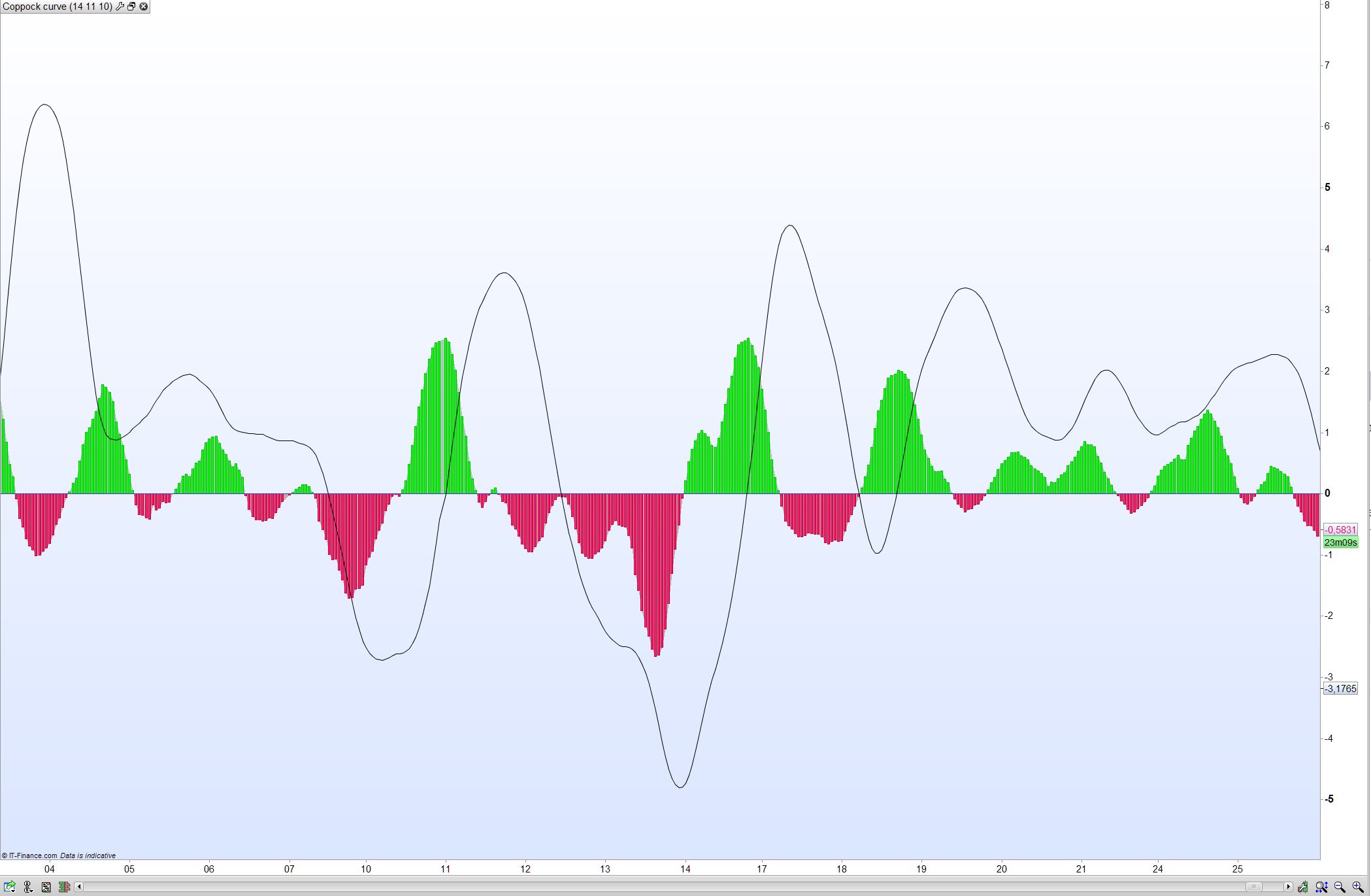

- Coppock rising curve under the 0 line- red in my scrn dump. Best from the lowest peak

- MACD minus signal like wise- however I discovered that when MACD and signal lines crosses, it’s also a strong indication for entry (manually sampled)

- CCI needs to cross over the 0 line.

- ADX needs to be above 25 to signal a strong trend.

- Heikin-Ashi needs to be green candle

But I cannot determine if this need to be true to both 4H and 1H TF before trying to pick the entry on a 15 or 1 min TF? Can you point me in the right direction? Also any advise in my perseption here would be welcome 🙂

Cheers Kasper

Here’s the code I used.

//-------------------------------------------------------------------------

// Main code : DAX CFTA LONG

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Main code : LONG GRID BB Exit

//-------------------------------------------------------------------------

defparam preloadbars = 100

once RRreached = 0

//parameters

accountbalance = 10000 //account balance in money at strategy start

riskpercent = 1 //whole account risk in percent%

gridstep = 10 //grid step in point

amount = 1 //lot amount to open each trade

rr = 2 //risk reward ratio (set to 0 disable this function)

//first trade whatever condition

if NOT ONMARKET AND close>close[1] AND STRATEGYPROFIT=0 then

BUY amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep*pipsize then

BUY amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

//floatingprofit = ((close-positionprice)*pointvalue)*countofposition

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize //actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*2

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

SELL AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif