Sometimes while trying to code strategies in today’s environment it is interesting to consider the bigger picture when trying to understand the relevance of our back test data.

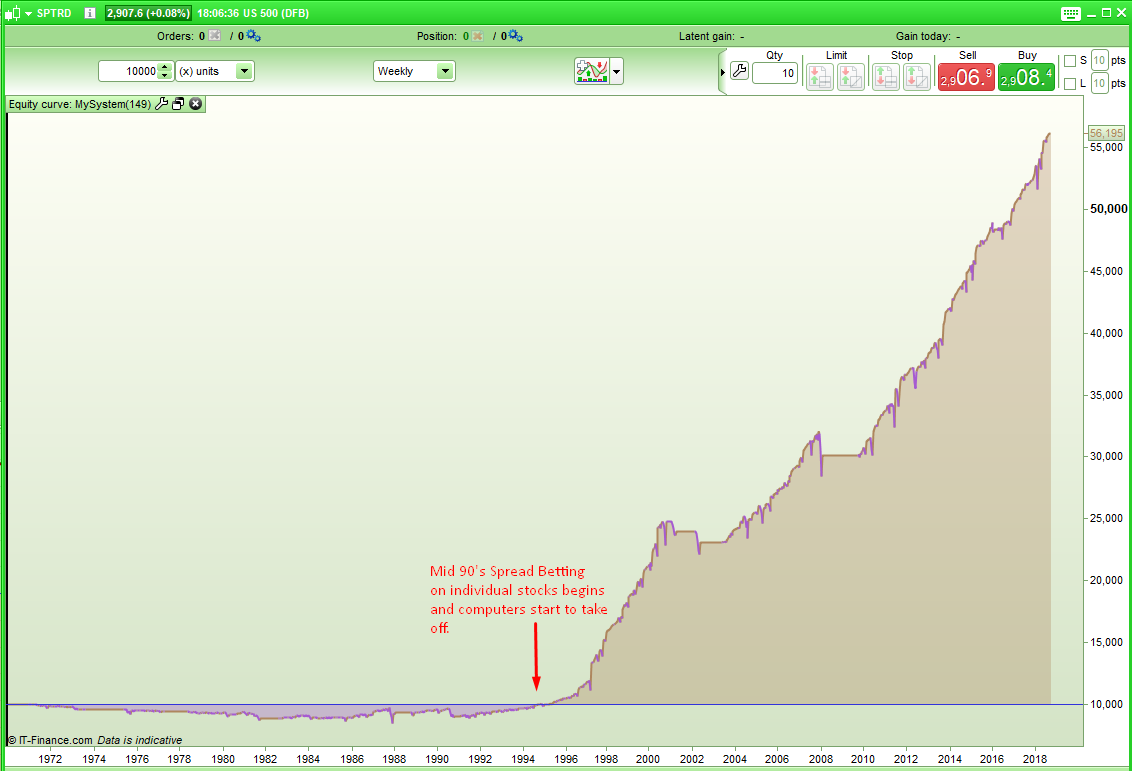

Here is the results of a simple SP500 weekly strategy and the point where data becomes relevant is not hard to spot.

Not much point in testing on any data before spread betting and computers hit the markets!

What I would be interested to know is how spreads have changed over the years. My feeling is that on indices the spreads will most likely have been a percentage of price and increased during volatile times but we have no way of using these varying spreads in our back tests which makes the back test results pretty meaningless. Which I guess is why lengthy forward testing is so important.

The effect of changes on the markets such as the invention of computers or the addition of new trading methods such as spread betting has got me wondering whether the new ESMA rules on margin will have any effect. If the cost of placing a trade increases then surely every non professional European trader’s risk changes and so their trading style or position size or quantity of trades has to change. I wonder if this will filter through to the markets in any way or whether us small fish have so little impact that the change in our trading will not touch the markets at all.

I also wonder whether as computer technology advances to new levels will this make the markets more stable or more volatile?

When you look at this image of the SP500 it would seem that as technology has rapidly progressed and the quantity of people reliant on the markets has increased we have a market that is more controlled with less downside.

To help us continually offer you the best experience on ProRealCode, we use cookies. By clicking on "Continue" you are agreeing to our use of them. You can also check our "privacy policy" page for more information.Continue

.

.