Okay so I wrote this strategy today after studying some Ichimoku Trading Stategies.

It is mainly based around Ichimoku breakout strategy but also includes checks for Directional Movement and Divergence.

I wrote it for my local market (South Africa 40 Cash) on the 1Hr Timeframe on which it performs okay, which is no mean feat.

But to be completely honest i am disappointed with Ichimoku as an automated strategy in general.

But enough mumbling. Here is the code, maybe someone will find it useful.

//Stategy: IchimokuDM

//Market: South Africa 40 Cash (ZAR2 Micro)

//Timeframe: 1Hr

//Spread: 15

//Timezone: UTC +2

Defparam Cumulateorders = False

Defparam Flatbefore = 090000

Defparam Flatafter = 170000

If hour < 9 or hour > 17 then //Works in conjunction with Flat Before/After time

possize = 0

If longonmarket then

SELL AT MARKET

ElsIf shortonmarket then

EXITSHORT AT MARKET

EndIf

Else

possize = 2 //Minimum position size

EndIf

P = 11 //Standard Period

R = P*2 //Standard Period x 2

I = P*3 //Standard Period x 3

TS = (highest[P](high)+lowest[P](low))/2 //Tenkan-Sen

KS = (highest[I](high)+lowest[I](low))/2 //Kijun-Sen

CS = close[I] //Chikou-Span

SA = (TS+KS)/2 //Senkou-Span A

SB = (highest[I](high)+lowest[I](low))/2 //Senkou-Span B

DP = DIplus[R](close) //DI+

DN = DIminus[R](close) //DI-

AX = ADX[R] //ADX

ATR = AverageTrueRange[P](close)

If RSI[R](close) > RSI[R](close[I]) Then

If close < CS Then

BDIV = 1 //Buy Divergence Present

SDIV = 0

EndIf

EndIf

If RSI[R](close) < RSI[R](close[I]) Then

If close > CS Then

BDIV = 0 //Sell Divergence Present

SDIV = 1

EndIf

EndIf

If countofposition = 0 and BDIV = 1 and AX > 17 and DP > 20 and DP > DN and close > SA and close > SB and TS > KS and close > CS and Close > SA[I] and Close > SB[I] Then

Buy possize*3 contracts at close + ATR stop

EndIf

If countofposition = 0 and SDIV = 1 and AX > 17 and DN > 20 and DP < DN and close < SA and close < SB and TS < KS and close < CS and Close < SA[I] and Close < SB[I] Then

Sellshort possize*3 contracts at close - ATR stop

EndIf

If Longonmarket then

If close < TS Then

Sell possize contracts at Market //Exit third of position at close below Tenkan-Sen Line

ElsIf close < TS and close < KS Then

Sell possize contracts at Market //Exit third of position at close below Kijun-Sen Line

ElsIf close < TS and close < KS and close < SA or close < SB Then

Sell at market //Exit full position at close below Senkou-Span

EndIf

ElsIf Shortonmarket then

If close > TS Then

Exitshort possize contracts at Market //Exit third of position at close below Tenkan-Sen Line

ElsIf close > TS and close > KS Then

Exitshort possize contracts at Market //Exit third of position at close above Kijun-Sen Line

ElsIf close > TS and close > KS and close > SA or close > SB Then

Exitshort at market //Exit full position at close above Senkou-Span

EndIf

EndIf

Set Stop pLOSS ATR*4

Set Target pPROFIT ATR*5

Thanks for this automatic trading strategy code. It seems to work fine on backtests, though I moved your post to the forum instead of the library, because ProOrder don’t support yet partial closure of positions and that’s what your strategy does between lines 58 to 74. I hope this will be available one day, but actually this strategy could only work in paper trading / backtest, not in real trading environment under ProOrder..Sorry for that 😐

Hi Nicolas

Yes it is unfortunate about ProOrder not supporting close of partial positions, however replacing lines 58 to 74 with the below code yields a very similar result to above without having to use partial position closing. So what about we modify the code and move it to the library in order for a bigger audience to benefit?

If Longonmarket then

If close < TS Then //If close below Tenkan-Sen Line

If close < close[1] Then

Sell at Market //Close position at next lower close

EndIf

EndIf

ElsIf Shortonmarket then

If close > TS Then //If close below Tenkan-Sen Line

If close > close[1] Then

Exitshort at Market //Close position at next higher close

EndIf

EndIf

EndIf

Great! I do not have much time now, but I’ll have a look tomorrow. Thanks juanj! 😉

So here is the modified code with your last addition:

//Stategy: IchimokuDM

//Market: South Africa 40 Cash (ZAR2 Micro)

//Timeframe: 1Hr

//Spread: 15

//Timezone: UTC +2

Defparam Cumulateorders = False

Defparam Flatbefore = 073000

Defparam Flatafter = 163000

If hour < 9 or hour > 17 then //Works in conjunction with Flat Before/After time

possize = 0

If longonmarket then

SELL AT MARKET

ElsIf shortonmarket then

EXITSHORT AT MARKET

EndIf

Else

possize = 2 //Minimum position size

EndIf

P = 11 //Standard Period

R = P*2 //Standard Period x 2

I = P*3 //Standard Period x 3

TS = (highest[P](high)+lowest[P](low))/2 //Tenkan-Sen

KS = (highest[I](high)+lowest[I](low))/2 //Kijun-Sen

CS = close[I] //Chikou-Span

SA = (TS+KS)/2 //Senkou-Span A

SB = (highest[I](high)+lowest[I](low))/2 //Senkou-Span B

DP = DIplus[R](close) //DI+

DN = DIminus[R](close) //DI-

AX = ADX[R] //ADX

ATR = AverageTrueRange[P](close)

If RSI[R](close) > RSI[R](close[I]) Then

If close < CS Then

BDIV = 1 //Buy Divergence Present

SDIV = 0

EndIf

EndIf

If RSI[R](close) < RSI[R](close[I]) Then

If close > CS Then

BDIV = 0 //Sell Divergence Present

SDIV = 1

EndIf

EndIf

If countofposition = 0 and BDIV = 1 and AX > 17 and DP > 20 and DP > DN and close > SA and close > SB and TS > KS and close > CS and Close > SA[I] and Close > SB[I] Then

Buy possize*3 contracts at close + ATR stop

EndIf

If countofposition = 0 and SDIV = 1 and AX > 17 and DN > 20 and DP < DN and close < SA and close < SB and TS < KS and close < CS and Close < SA[I] and Close < SB[I] Then

Sellshort possize*3 contracts at close - ATR stop

EndIf

If Longonmarket then

If close < TS Then //If close below Tenkan-Sen Line

If close < close[1] Then

Sell at Market //Close position at next lower close

EndIf

EndIf

ElsIf Shortonmarket then

If close > TS Then //If close below Tenkan-Sen Line

If close > close[1] Then

Exitshort at Market //Close position at next higher close

EndIf

EndIf

EndIf

Set Stop pLOSS ATR*4

Set Target pPROFIT ATR*5

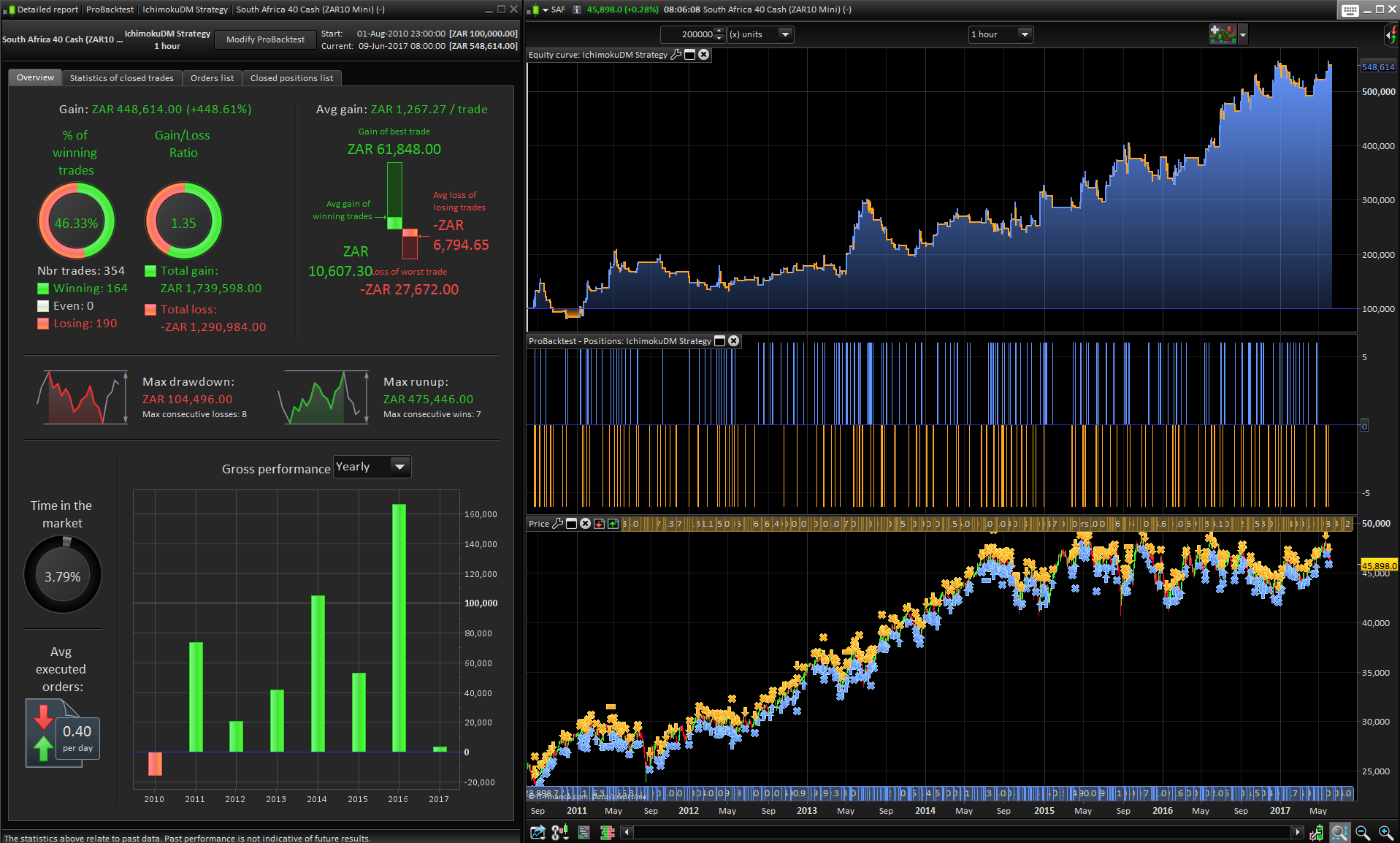

I changed the time schedule between 07.30-16.30 for the intraday 8 points spread. Results attached, please confirm before I add it into the library! thanks.

Hi Nicholas, the results seem valid. I don’t have the amount of data points you have so mine will look slightly different. Pleased to see it still performs on par in the period outside of my optimization time frame. This actually serves as validation of the strategy.

Maz

MazParticipant

Veteran

Nice idea, will take a look and post any updates.

Yea, bit of a pain with the lack of partial closures, bi-directional trading and stuff- but as quick proof of concept it’s useful.

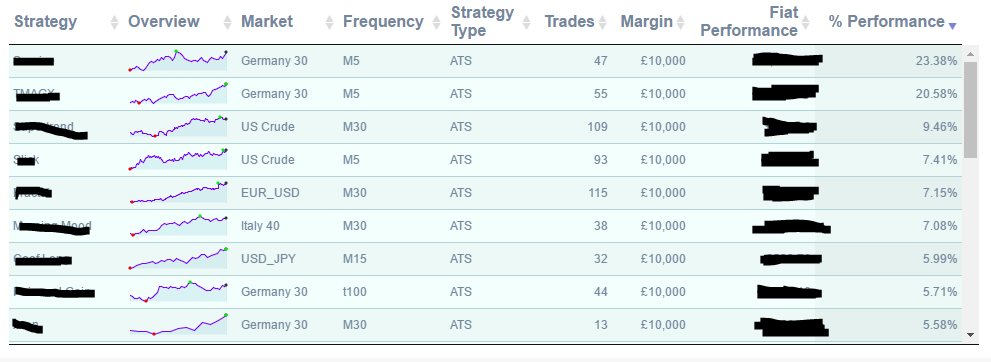

Just for future reference guys, if you are dependent on abilities such as to execute partial closures and wish to run with such features, I could actually make that happen for you using our own tools. Wouldn’t normally disclose the screen shots attached but I think there’s some good ideas and thinking out here that is out-growing PRT. (attached is monitoring views from our system)

Best,

M

@Maz, regarding your screenshots, what are we looking at???