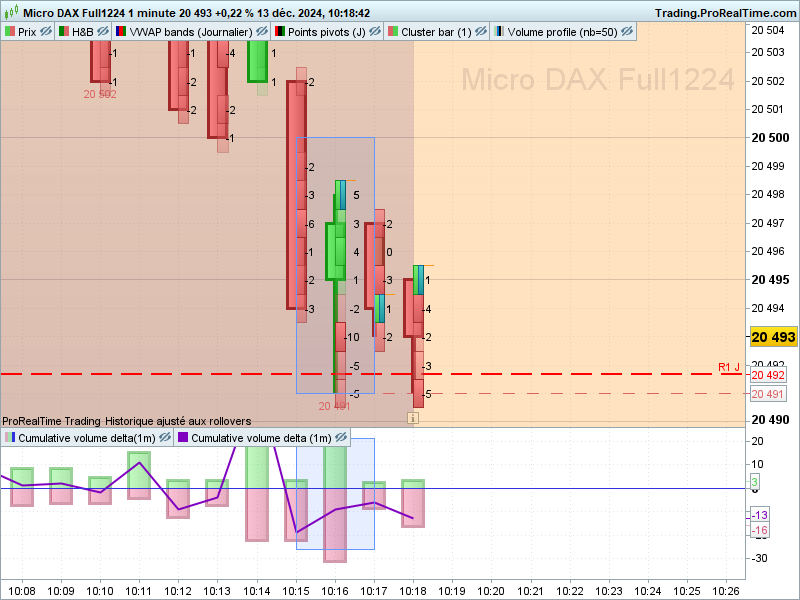

J’ai trouvé ce code sur trading view mais il faudrait que ce soit validé avec prorealtime…

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at

https://mozilla.org/MPL/2.0/

// © nico-von

//@version=5

indicator(“OrderFlow Absorption Indicator”, shorttitle = “Absorption”, overlay = true,

max_labels_count = 500, max_boxes_count = 500)

//<constants>

const int UP_DIRECTION = 1

const int NT_DIRECTION = 0

const int DOWN_DIRECTION = -1

const string PHDT_TT = “Plot historical absorption occurrences. Using historical data alone cannot accurately replicate real-time absorption, so detections may differ.”

const string HDT_TT = “Timeframe for calculating historical absorption: A smaller timeframe results in more accurate detections but in a slower indicator, potentially hindering real-time absorption detection.”

const string TL_TT = “Limit detections to consider only traded volume that is greater than or equal the selected volume filter value within the chosen time limit, in seconds. Real-time only.”

const string VLMT_TT = “Traded volume greater than or equal this value will be marked as absorbed. The larger value, the fewer detections.”

const string VLMT_AUTO_TT = “Automatically set the minimum size according to the standard deviation of traded volume for the last selected minutes.”

const string HIST_GP = “Historical/ Backfill Settings”

const string MINS_ERROR = “SD Interval must be greater than 0”

const string DATA_GP = “Tick Settings”

const string AB_GP = “Time Limit Settings”

const string AVLMT_GP = “Volume Filter Settings”

const string OTHER_GP = “Other Settings”

const string CHAR_TO_USE = “×”

const string CHAR_TO_USE_POINTER = “■”

const string STYLE_GROUP = “Style Settings”

const string IN_DELTA = “Delta Colour Settings”

const int DEF_SD_MULT = 10

//<input>

bool useLtfInput = input.bool(false, “Plot Historical Absorption”, tooltip = PHDT_TT,

confirm = true, group = HIST_GP, display = display.none)

string ltfInput = input.timeframe(“1”, “Historical Data Timeframe”, tooltip = HDT_TT,

confirm = true, group = HIST_GP, display = display.none)

float tickSizeInput = input.float(5, “Desired Tick Size”, confirm = true, group = DATA_GP)

bool enableTimeLimitInput = input.bool(false, “Enable time limit (realtime only)”, confirm = true,

tooltip = TL_TT, group = AB_GP, display = display.none)

float timeLimitInput = input.float(0.5, “Time limit (seconds)”, confirm = true, group = AB_GP,

display = display.none)

float volumeLimitInput = input.float(5, “Volume Filter”, tooltip = VLMT_TT, confirm = true,

group = AVLMT_GP, display = display.none)

bool autoVolumeLimitInput = input.bool(true, “Use Auto Mode”, tooltip = VLMT_AUTO_TT, confirm = true,

group = AVLMT_GP, display = display.none)

int autoVolMinsInput = input.int(30, “SD Interval (minutes)”, confirm = true, group = AVLMT_GP,

display = display.none)

int autoSdMultInput = input.int(DEF_SD_MULT, “SD Multiplier”, confirm = true, group = AVLMT_GP,

display = display.none)

bool deltaModeInput = input.bool(true, “Enable Delta Mode”, confirm = true, group = OTHER_GP,

display = display.none)

color neutralColourInput = input.color(color.yellow, “Regular”, group = STYLE_GROUP,

display = display.none)

color askColourInput = input.color(color.red, “Ask Delta”, group = STYLE_GROUP, inline = IN_DELTA,

display = display.none)

color bidColourInput = input.color(color.green, “Bid Delta”, group = STYLE_GROUP, inline = IN_DELTA,

display = display.none)

//<interface>

type absorptionObj

varip float movePrice

varip float nextPriceInQueue

varip int moveDirection

varip float volumeAbsorbed

varip float volumeAccumulator

varip bool absorbed

varip float absorbingPrice

varip bool isBuy

varip int startingTime

varip int nextTimeInQueue

type absorptionDisplayObj

varip float sellVolAbsorbed

varip float buyVolAbsorbed

varip float deltaValue

varip bool isrealtime

varip float volumeLimit

//<function>

calculateTick(float price, float tickSize) =>

float multiplier = math.round(price / tickSize)

multiplier * tickSize

convertSecstoMs(float seconds) =>

math.round(seconds * 1000)

checkAbsorption(int currDirection, int moveDirection, bool metTimeLimit = true) =>

absorbed = (currDirection != moveDirection) and metTimeLimit

absorbed

getDirection(float movePrice, float nextPrice, int upDirection, int ntDirection, int downDirection) =>

if movePrice == nextPrice

ntDirection

else if movePrice > nextPrice

downDirection

else if movePrice < nextPrice

upDirection

getVolumeChange(float newVolume, float prevVolume) =>

newVolume – prevVolume

checkPriceChange(float currPrice, float newPrice) =>

currPrice != newPrice

updateAbsorptionObj(absorptionObj object, float priceTick, float volumeChange,

float volumeLimit, int timeNow = na, int timeLimit = na) =>

bool priceChanged = checkPriceChange(object.movePrice, priceTick)

int currDirection = getDirection(object.movePrice, priceTick, UP_DIRECTION, NT_DIRECTION, DOWN_DIRECTION)

object.absorbingPrice := na

object.absorbed := false

if na(object.movePrice)

object.movePrice := priceTick

if na(object.startingTime) and not na(timeNow)

object.startingTime := timeNow

if priceChanged and object.moveDirection == NT_DIRECTION

object.moveDirection := currDirection

object.nextPriceInQueue := priceTick

object.nextTimeInQueue := timeNow

if priceChanged and object.moveDirection != NT_DIRECTION

bool metTimeLimit = true

if not na(timeLimit) and not na(timeNow)

int expectedTime = object.startingTime + timeLimit

metTimeLimit := timeNow <= expectedTime

bool absorbed = checkAbsorption(currDirection, object.moveDirection, metTimeLimit)

object.absorbingPrice := object.movePrice

object.absorbed := absorbed and (object.volumeAccumulator >= volumeLimit)

object.volumeAbsorbed := object.absorbed ? object.volumeAccumulator : 0

object.isBuy := object.moveDirection == DOWN_DIRECTION

object.startingTime := object.nextTimeInQueue

object.nextTimeInQueue := timeNow

object.movePrice := object.nextPriceInQueue

object.nextPriceInQueue := priceTick

object.moveDirection := currDirection

object.volumeAccumulator := volumeChange

else if not priceChanged

object.volumeAccumulator += volumeChange

object.isBuy := na

// return

object

includeToAbsorbingMap(map<float, absorptionDisplayObj> absorbingPrices,

absorptionObj mainObject, bool isDelta, float volumeLimit, bool isRealTime = false) =>

if mainObject.absorbed

absorptionDisplayObj absorptionDisplay = absorbingPrices.keys().includes(mainObject.absorbingPrice) ?

absorbingPrices.get(mainObject.absorbingPrice) :

absorptionDisplayObj.new(0, 0)

if mainObject.isBuy

absorptionDisplay.buyVolAbsorbed += mainObject.volumeAbsorbed

else

absorptionDisplay.sellVolAbsorbed += mainObject.volumeAbsorbed

absorptionDisplay.deltaValue := absorptionDisplay.buyVolAbsorbed – absorptionDisplay.sellVolAbsorbed

absorptionDisplay.volumeLimit := volumeLimit

absorptionDisplay.isrealtime := isRealTime

if isDelta and math.abs(absorptionDisplay.deltaValue) < absorptionDisplay.volumeLimit

absorbingPrices.remove(mainObject.absorbingPrice)

else

absorbingPrices.put(mainObject.absorbingPrice, absorptionDisplay)

absorbingPrices

getHistoricalData() =>

[calculateTick(close, tickSizeInput), volume]

getAutoVolumeLimit(int len) =>

ta.stdev(volume, len)

//<calculation>

var simple string ltfDisabler = timeframe.from_seconds(timeframe.in_seconds(timeframe.period) * 2)

float closeTick = calculateTick(close, tickSizeInput)

var int timeLimit = enableTimeLimitInput ? convertSecstoMs(timeLimitInput) : na

varip absorptionObj mainObject = absorptionObj.new(na, na, NT_DIRECTION, 0, 0, na, na, na)

varip float prevVolume = volume

varip bool isBarConfirmed = false

varip map<float, absorptionDisplayObj> absorbingPrices = map.new<float, absorptionDisplayObj>()

// reset

if isBarConfirmed and barstate.isnew

isBarConfirmed := false

absorbingPrices := map.new<float, absorptionDisplayObj>()

float volumeChange = getVolumeChange(volume, prevVolume)

// historical

[priceTick, volChangeLTF] = request.security_lower_tf(syminfo.tickerid, useLtfInput ? ltfInput : ltfDisabler,

getHistoricalData(), true, ignore_invalid_timeframe = true)

// volume limit (filter)

if autoVolMinsInput <= 0

log.error(MINS_ERROR)

autoVolumeLimitVal = request.security(syminfo.tickerid, “1”, getAutoVolumeLimit(autoVolMinsInput)

, ignore_invalid_symbol = true, calc_bars_count = autoVolMinsInput)

float volumeLimit = if autoVolumeLimitInput and not na(autoVolumeLimitVal)

autoVolumeLimitVal * autoSdMultInput

else

volumeLimitInput

priceTick := barstate.ishistory ? priceTick : na

if not na(priceTick)

for i = 0 to priceTick.size() – 1

if priceTick.size() == 0

break

mainObject := updateAbsorptionObj(mainObject, priceTick.get(i), volChangeLTF.get(i), volumeLimit)

absorbingPrices := includeToAbsorbingMap(absorbingPrices, mainObject, deltaModeInput, volumeLimit)

// live

if barstate.isrealtime

mainObject := updateAbsorptionObj(mainObject, closeTick, volumeChange, volumeLimit, timenow, timeLimit)

absorbingPrices := includeToAbsorbingMap(absorbingPrices, mainObject, deltaModeInput, volumeLimit, true)

// prep values for next bar

prevVolume := volume

if barstate.isconfirmed

prevVolume := 0

isBarConfirmed := true

// <display>

for key in absorbingPrices.keys()

chart.point xy = chart.point.new(time, na, key)

absorptionDisplayObj absorptionDisplay = absorbingPrices.get(key)

string labelText = deltaModeInput ?

str.format(“{0} {1}”, CHAR_TO_USE_POINTER, absorptionDisplay.deltaValue) :

str.format(“{0} ▲ {1} {2} ▼ {3}”, CHAR_TO_USE_POINTER,

str.tostring(absorptionDisplay.buyVolAbsorbed, “#.###”),

CHAR_TO_USE, str.tostring(absorptionDisplay.sellVolAbsorbed, “#.###”))

color textColour = deltaModeInput ?

absorptionDisplay.deltaValue >= 0 ? bidColourInput : askColourInput :

neutralColourInput

string tooltip = str.format(“{0} \nVol Absorbed by Bids: {1} \nVol Absorbed by Asks: {2} \nVol Filter Value: {3} \nRealtime Data: {4}”,

key, absorptionDisplay.buyVolAbsorbed, absorptionDisplay.sellVolAbsorbed,

absorptionDisplay.volumeLimit, absorptionDisplay.isrealtime ? “Yes” : “No”)

label.new(xy, labelText, xloc = xloc.bar_time, yloc = yloc.price, color = color.new(color.white, 100),

style = label.style_label_left, textcolor = textColour, tooltip = tooltip)

// recommendations table

string recommendedTickSize = str.format(“Recommended Tick Size: {0}”,

str.tostring(request.security(syminfo.tickerid, “1”, ta.atr(14)), “#.###”))

string recommendedFilterArg = not na(autoVolumeLimitVal) ?

str.tostring(autoVolumeLimitVal * DEF_SD_MULT, “#.###”) : “Cannot be determined.”

string recommendedFilterSize = str.format(“Recommended Volume Filter: {0}”, recommendedFilterArg)

table recommendationTable = table.new(position.top_right, 1, 2, bgcolor = color.new(color.black,50))

recommendationTable.cell(0, 0, recommendedTickSize, text_color = color.white, text_halign = text.align_left)

recommendationTable.cell(0, 1, recommendedFilterSize, text_color = color.white, text_halign = text.align_left)